The mass affluent market is a segment that financial planners have struggled to win and profitably service, but with technology and a fresh approach to advice, there is a way forward, to build a successful business servicing this diverse, aspirational mob.

First, the industry must end its obsession with investable assets and start focusing on a person’s investable cash flow; which arguably provides a better indication of their potential to be an engaged, long-term client.

This is a significant mind-shift because historically advisers were remunerated by the product and therefore focused on selling product.

That mindset has limited many to only a small percentage of the potential advice market.

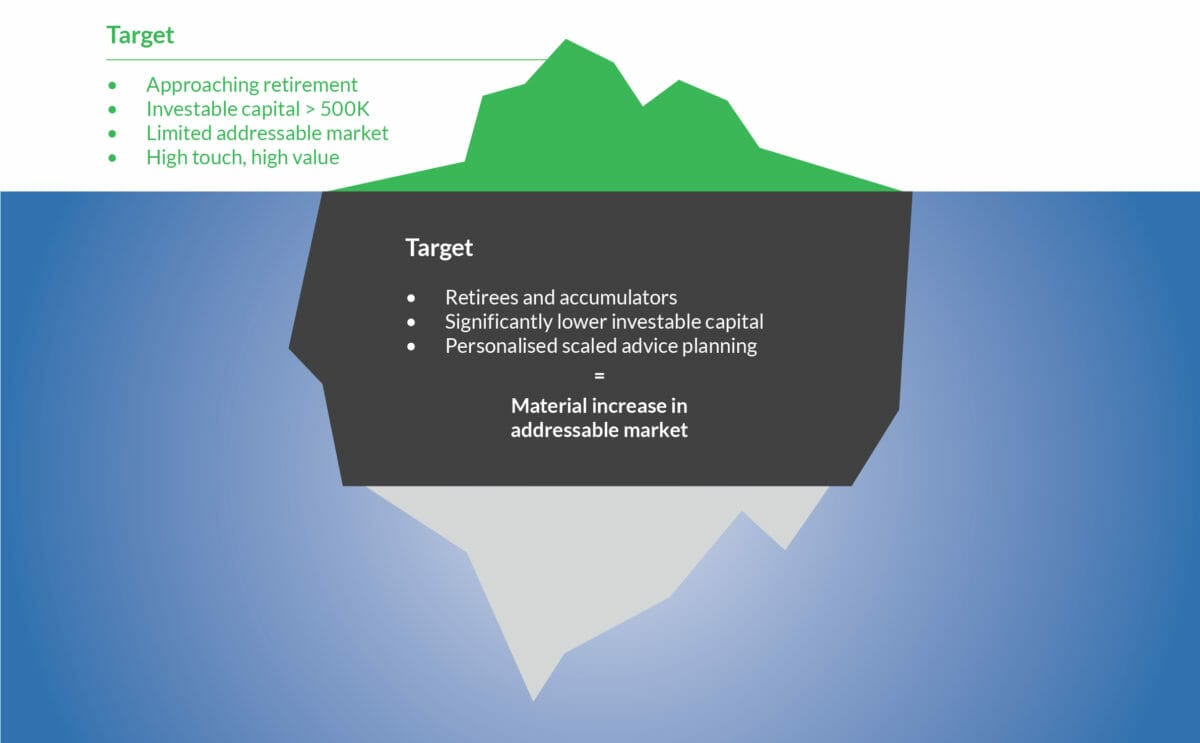

If the market for advice was depicted as an iceberg, the visible tip of the “adviceberg” would be the 20 per cent of Australians who currently seek professional advice, mainly wealthy retirees and pre-retirees. The large submerged population would be the mostly ignored – but potentially lucrative – mass market, including retirees and accumulators with lower investable assets, millennial entrepreneurs, single women, up-and-comers, and those on track to inherit eye-watering wealth.

The industry must accelerate its shift from product-based investment advice to goals-based advice, and consider a client’s investable cashflow in addition to their current and future investable assets, in order to capture opportunities in the adviceberg.

An advice proposition that’s exclusively focused on investing or life insurance won’t always cut it.

Technology makes everything possible

Adopting the right technology and embracing automation is the other key to success. It’s impossible to build and implement an efficient, scalable and economically-viable advice proposition for a broad disparate group without it.

Advisory firms can use technology to do the bulk of pre-sales and qualifying. They can automate tasks like gathering client information, sending out generic company information, responding to simple questions and prompting people to make an appointment.

Automation ensures that no-one slips through the cracks. It eliminates human error, takes over repetitive, low-value work and reduces the amount of time spent on people who aren’t serious about engaging an adviser or aren’t ready to make a decision.

Systems can be set up to ask clients to complete online questionnaires, chase responses and collect data like financial account balance and transaction details.

Advisers are increasingly integrating personal financial management (PFM) technology into their practices, to gather and consolidate account balance and transaction data from multiple sources, including bank and superannuation accounts, to gain a complete picture of a person’s financial position and lifestyle.

With technology, advisers can analyse a person’s spending and saving, debt and cashflow management, banking structures, super contributions and investments to determine their level of money management maturity and identify potential problem areas.

That insight can form the foundation of a highly customised financial plan that demonstrates a keen understanding of the client’s situation and specifies the value that an adviser can deliver, the level of service required and an estimated fee.

A customised plan can be put together relatively quickly so the conversation can progress smoothly.

OK Computer

Parts of the ongoing advice process can also be automated, such as monitoring a client’s financial position and portfolio, and tracking their progress towards their goals.

While many people have similar goals like buying a home, sending their kids to private school and affording a comfortable retirement, they’ll all require a different strategy to achieve them, based on personal factors such as their cashflow, ability to save and invest, risk tolerance, and timeframe.

Historically, the advice industry has taken a product-focused, cookie cutter approach to servicing the mass affluent with little success.

Advisers have to find a way to economically deliver customised, personal advice to Australians beneath the tip of the adviceberg if they hope to replenish their ageing clientbases.

Fortunately, contrary to popular belief, many mass affluent individuals understand the importance of saving and investing, and the value of professional advice. Many also have reasonable money management skills, but they need someone to coach and mentor them. That way they can discover their true goals and objectives, adopt healthy financial behaviour, make smart financial decisions, grow and protect their wealth, and ultimately migrate to the tip.

Advisers who want to reach new markets and grow their business need the right technology solutions to develop and provide a sustainable, profitable advice proposition.

Leave a Comment

You must be logged in to post a comment.