The ageing of the population has long been touted as one of the key economic and social drivers affecting Australia over the long term. This demographic shift will be one of the major forces shaping the demand and delivery of financial advice.

Advice processes, strategies and education supporting the accumulation phase of superannuation have been well developed to support clients building their pre-retirement savings. However, by comparison, this support is lacking for servicing clients in the post-retirement phase. Clients in the post-retirement phase are likely to represent a growing portion of an adviser’s client base and their savings will become a greater portion of overall superannuation savings.

The trend

Australians are expected to live longer and continue to have one of the longest life expectancies in the world. According to UN data, Australia ranks equal first with Iceland in male life expectancy. For females, we rank only behind Japan, Spain, France and Italy.

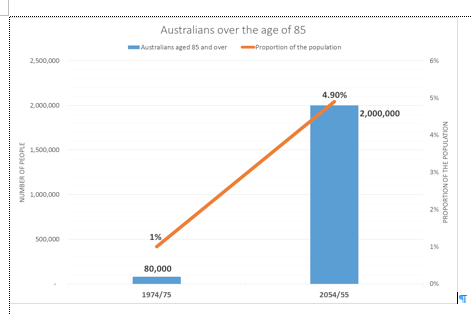

In 2054-55, there are projected to be 40,000 people over the age of 100. This is a stark increase from the 122 Australian centenarians in 1974-75. The number of people aged 85 and above is also predicted to jump over the next 40 years, as illustrated in the accompanying graph.

The number of Australians over the age of 85 is expected to reach close to 2 million people in the next 40 years. At this time, one in 20 people will be over age 85.

Importantly, the increase in life expectancy is matched by an increase in healthy life expectancy. Improvements in health mean that older Australians are likely to remain active for longer. “Active ageing” presents great opportunities for older Australians to have more active and engaged retirement years. This may enable them to stay in the workforce for longer and be more active in the community.

Advice implications

The way in which advisers help their clients plan for retirement is likely to change. There will also be more demand for ongoing and active advice during retirement. There is likely to be greater focus on managing the client’s longevity risks and the need for a sustained level of income (essential and discretionary income) to provide a more active lifestyle in retirement.

The portfolio construction approach and selection of investments may need to be reviewed and modified and better tailored to the specific client’s situation. More than ever before, tailored strategies that match the client’s specific situation are required for retirees and pre-retirees.

These trends also reflect the growing importance of aged care advice that offers a development opportunity for advisers and Australian financial services licensees (AFSLs).

Those aged over 85 have an immediate need for aged care advice, including advice to help them stay in their home. In many cases, it is their children (50-plus age group) who will be the “client” in demand of aged care advice on behalf of their parents. Advisers also need to consider the client’s aged care needs and account for the costs in providing acceptable aged care support in the “disability” years of their life.

Aged care services also enable advisers to retain funds under advice by building relationships with the children of clients.

The forces shaping the financial services industry are many, but the demographic trends will only accelerate the need to review and adapt advice models and processes.

Leave a Comment

You must be logged in to post a comment.