• Total loans outstanding grow to $3.7 billion

• Increased rate of early repayment by borrowers, up to 12.5% pa

Large banks including CBA, St George, BankWest and Macquarie Bank continue to support Australian retirees in accessing a valuable form of home equity release via reverse mortgages.

The use of property to be considered alongside other retirement sources is an area of emerging interest across broader financial services organisations including industry funds, retail wealth managers, banks and non-bank lenders and insurance companies according to Deloitte.

In its annual Reverse Mortgage Report, Deloitte estimates more than $500 billion of home equity is held by Australians aged over 65, with the total reverse mortgage loan book worth $3.66bn as at the end of 2014.

James Hickey, Deloitte Partner Financial Services and author of the Deloitte report said: “Although the Australian reverse mortgage loan book grew more than 3% to the current $3.66bn, it represents a small proportion of the potential funds available to be accessed by senior Australians.”

Hickey said: “Currently there are almost 40,000 reverse mortgages on issue in Australia with an average loan size of $92,000, up from $86,000 in 2013.

“The top three uses for the released equity remain debt consolidation, supporting an income stream and home improvements. However, this year there was renewed interest in how the product could be structured to support financing needs for Aged Care accommodation bonds.

“The changes to aged care accommodation payments that came into effect 1 July 2014 with the Living Longer, Living Better reforms, have generated additional interest in how reverse mortgages can play a far greater role in assisting senior Australians navigate one of the most stressful stages of retirement, that of financing the accommodation bond.

“For many retirees the equity in their home continues to represent two thirds or more of their entire wealth, well in excess of their superannuation balance. While many people may ordinarily access this housing equity by downsizing, there are many challenges to that approach.

“This includes having to sever the emotional ties to the family home, the availability and suitability of properties to downsize to, and the treatment of monies released in the assets test for social security purposes.

“A reverse mortgage offers the option for retirees to stay in their home and access equity in a manner which may have far less impact, if any, on their social security entitlements. This means that a reverse mortgage can be a very useful option for retirees to consider when looking for ways to supplement their superannuation retirement income,” Hickey said.

“Being aware of equity release options and how they work requires both support and education. We believe banks, insurers, qualified financial advisers and superannuation funds are best placed to embrace, understand and educate Australians on the options available with equity release products.

“These are the groups seeking to help their customers aged 65 plus to navigate their retirement with the dual challenges of longevity and income sustainability. Bringing what is often their most substantial asset, their home, into such discussions must be in the best interests of everyone,” Hickey said.

The 13th comprehensive annual study of the Australian reverse mortgage sector, commissioned by the Senior Australians Equity Release Association (SEQUAL), shows that at 31 December 2014, the reverse mortgage market in Australia consisted of 40,000 reverse mortgage facilities, with total outstanding funding of $3.66 billion.

| Dec 06 | Dec 07 | Dec 08 | Dec 09 | Dec 10 | Dec 11 | Dec 12 | Dec 13 | Dec 14 | |

| Outstanding market size | $1.51b | $2.02b | $2.48b | $2.71b | $3.01b | $3.32b | $3.56b | $3.56b | $3.66b |

| Number of loans | 27,898 | 33,741 | 37,530 | 38,788 | 41,640 | 42,410 | 42,455 | 41,435 | 39,867 |

| Average loan size | $54,233 | $60,000 | $66,150 | $69,896 | $72,474 | $78,249 | $83,840 | $85,881 | $91,740 |

| Settlements | $520m | $466m | $321m | $264m | $322m | $317m | $305m | $302m | $272m |

| Facility (settlements) | $714m | $627m | $426m | $367m | $449m | $426m | $385m | $404m | $307m |

| Additional drawdowns | N/A | $125m | $116m | $126m | $131m | $73m | $65m | $47m | $46m |

| Discharges | N/A | $203m | $253m | $309m | $354m | $338m | $350m | $504m | $555m |

“Some 3,400 new borrowers took out a reverse mortgage in 2014. The average size of a reverse mortgage loan is now nearly $92,000. In addition to new borrowers, 4,900 borrowers voluntarily repaid their reverse mortgage loan in 2014 (representing 12% of total borrowers). This shows that many borrowers are using the product to cover short terms needs and then repay the mortgage once they are ready to finally downsize their home,” Hickey said.

John Thomas, Chairman of SEQUAL, the peak industry body that governs equity release providers and determines consumer safeguards, said: “We are very pleased that large lenders such as the CBA, St George, BankWest and Macquarie Bank continue to support the sector. There are take-up opportunities for the product in every state in Australia.

“The annual Deloitte report shows that the majority of equity release customers are couples (47%), followed by single females (36%) with those aged between 70-79 predominating (49%). The average age of new borrowers is 75 years.”

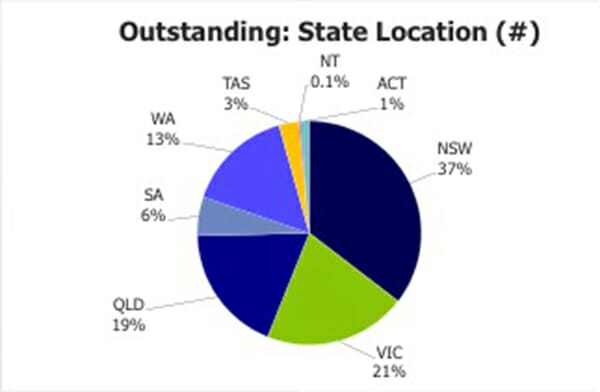

The state-based percentage of outstanding loans has remained fairly constant year on year:

• Around 71% of loans outstanding are in capital cities down six per cent from the previous year

• The larger regional areas in NSW and QLD lead growth of non-metro lending

• The recent settlements of 85% in capital cities is down three per cent over the previous year

• Houses made up 80% of settlements in 2014

• Lenders are now willing to accept units and other property types outside stand-alone dwellings in capital cities

Summary of key findings

The market by $ outstanding has grown 3% in the 12 months to December 2014

Some 3,400 new borrowers took out a reverse mortgage in 2014

The full discharge rate of 12.5% p.a. is mainly due to sale of property and voluntary repayment

Additional drawdowns are approximately 1.3% of outstanding loans

Lump sum are the most popular drawn down type

Brokers and planners settlements channel 31%, direct channel 69%

Proportions of outstanding loans by #: NSW 37% of market, VIC 21% & QLD 19%

Source: Deloitte/SEQUAL

Leave a Comment

You must be logged in to post a comment.