In 12 years of measuring Australia’s retirement savings gap, Rice Warner has witnessed an alarming divergence between policy makers regarding a unified and measurable set of long-term objectives for superannuation. As the superannuation industry explores ways to solve the real savings gap, arguments for resolving the ‘policy gap’ have also intensified. Is it not time to finally agree measurable bi-partisan objectives against which Treasury can benchmark policy changes?

David Murray’s Financial System Inquiry (FSI) indicated that a lack of clarity exists when it comes to the objective of superannuation. It suggested the primary objective should be “to provide income in retirement to substitute or supplement the Age Pension.” It made a number of subsidiary objectives including to alleviate fiscal pressures on government from the retirement income system.

These comments are made against an historical backdrop of policy tinkering with superannuation, and a lack of political cohesion as to the ultimate purpose of the system. So, we have two gaps. The superannuation savings gap, which in partnership with the Financial Services Council – has been measured by Rice Warner since 2003.

The second gap is the policy distance between the major parties, wherein sensible reform is often put aside in favour of political expediency. A good example is the current government’s reluctance to address inequity in superannuation.

To highlight how the politics can impact the savings gap, the Superannuation Guarantee rate decision is a good example. We have seen the Savings Gap increasing over time, most recently to $768 billion at 30 June 2014 (up from $727 billion the previous year). The single government policy that had the biggest impact on this movement was the deferral of the increase in the Superannuation Guarantee from 9.5% to 12% by a further four years. This deferral added $118 billion to the gap.

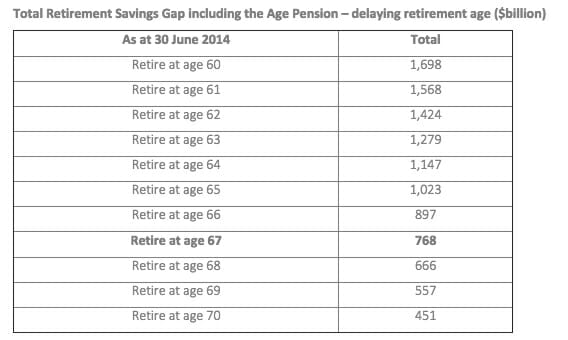

Similarly, the research shows the impact that deferring retirement will have on the size of the gap. Rice Warner applies a retirement age of 67 when measuring the gap. This is higher than the median retirement age for current retirees (about 62), but may be more realistic for younger workers given that workforce participation for older workers is trending upwards.

The table shows the impact of different retirement ages. If the current cohort of workers retired at age 62, the size of the gap would be $1,424 billion – almost double the gap at age 67. This implies a strong case to increase the Preservation Age in line with increases in the Age Pension eligibility age, along with further policies to support workforce participation for older employees.

Clearly, it serves the national interest for the majority of Australians to be self-sufficient in retirement. If there were bi-partisan agreement to achieve this, we could look to consensus on raising the Preservation Age and simultaneously seeking to promote work for older Australians.

We would all benefit from the outcomes of such an approach.

Source: Rice Warner

Leave a Comment

You must be logged in to post a comment.