Australians have spoken firmly against the idea of having their local supermarket as their superannuation provider. CoreData’s 2015 Member Engagement Report found more than three in four (76.3%) Australians would never consider Coles or Woolworths as their super fund, while one in seven (14.4%) would only consider them if they charged no fees.

Andrew Inwood, Principal at CoreData, says “With Coles and Woolworths increasingly involved in financial services, these findings tell us they would face a considerable challenge if they were to penetrate Australia’s $2 trillion superannuation sector.”

Higher overall satisfaction and advocacy

These findings have come amid the continuing improvement in satisfaction with super funds, with close to three in four (73.5%) respondents saying they are satisfied overall with their main fund, up from 65.6% in 2014. Reflecting this, more than half (55.6%) are likely to recommend their main fund to others, up from 48.4% in 2014.

Industry funds fundamentally trump retail funds in overall satisfaction (76.9% vs. 64.7%) and advocacy (64.5% vs. 41.9%).

These positive sentiments have meant Australians are now less likely to switch funds, with only 11.8% of respondents looking to change their fund, down from 15.0% in 2014.

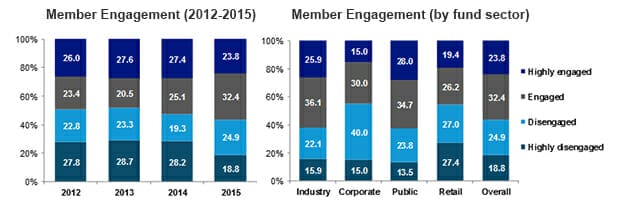

Member engagement also on the way up

In further good news to super funds, efforts to improve member engagement seem to have paid off with the proportion of members classified as engaged or highly engaged rising to 56.2% from 52.5% in 2014.

With their high levels of satisfaction and advocacy, industry fund members are the most engaged with their super fund (62.0%), up from 52.8% in 2014 and well ahead of those in retail funds (45.6%).

By fund, members of UniSuper are the most engaged (75.9%), while AMP members are the least engaged (36.8%).

However, despite the improvements this year, there remains a large proportion of super fund members classified as disengaged or highly disengaged (43.7%). This suggests the industry still has some way to go in lifting overall member engagement, particularly among Generation Y members, where the majority (52.6%) are disengaged to some extent.

Lower fees and improve returns to drive engagement

When asked what their main fund could do to engage them more, respondents most commonly cite lower fees and improve returns (54.2% and 53.6% respectively).

Furthermore, reducing the fees they currently pay remains an important consideration for super fund members, with seven in 10 (69.7%) respondents saying it is very or quite important. And while a quarter (26.9%) of those who find it important to reduce fees would not want to trade in anything for reduced fees, it is compelling that nearly seven in 10 (69.1%) would trade off their fund’s public profile by reducing spending on marketing/advertising, up from 44.4% in 2014.

“Previous CoreData research found advertising is not an appealing marketing and communication channel to members and the industry in general suffers from a lack of brand distinctiveness, despite the money being spent on high profile advertisements and sponsorships. Big spending on these advertisements and sponsorships are not necessarily translating to greater member engagement”, says Inwood.

Inwood adds, “Super funds need to change their mindset and go beyond advertising and instead focus on utility. This is emerging as an effective tool to establish a distinctive brand identity that appeals to the increasing number of engaged and discerning super consumers who are making an active choice with regards to their super.”

Sizeable intra-fund advice opportunity with Gen Ys

One way in which super funds can tackle the disengagement problem among Generation Y members is through intra-fund advice. Overall, less than one in three (31.7%) members have used their fund’s financial planning services, with Generation Y members the least likely to have taken up intra-fund advice (6.4%). However, more than a third (35.5%) of Generation Y members who have not used their fund’s advice services intend to use them if available.

Given the sizeable latent demand for intra-fund advice, funds need to consider offering intra-fund advice and better communicate their advice offer and value proposition in order to build a relationship with members and increase their engagement level, particularly among their youngest members.

Source: CoreData

Leave a Comment

You must be logged in to post a comment.