In this article, we put accumulation aside and focus on the super fund landscape in retirement. While Commonwealth Superannuation Corporation is Australia’s largest pension fund, retail funds operating advice platform businesses have the largest proportion of their members in retirement. This creates an interesting dynamic around who will be the leaders in the retirement segment.

Applying APRA’s data and understanding flow

Our analysis involves taking APRA’s annual fund-level superannuation data for FY23, as described in previous articles on size, flow, and the super fund landscape, and cleaning it up. We use information about assets and accounts in the tax-free phase to identify members in retirement. This potentially understates the true number of retirees, some of whom may have not yet transitioned their assets across from accumulation to drawdown. We also analyse data on benefit payments to members, which helps to corroborate our findings based on tax-free phase account data.

Our research requires some unique treatment of CSC, the long-standing provider of pensions for employees of the Commonwealth Government including through its defined benefit funds. There is a regulatory requirement to report defined benefit liabilities as assets, rendering the asset data incomparable. We thus exclude CSC from any retirement asset-based analysis.

Retirement accounts, assets and benefit payments

The top 50 APRA-regulated funds by net assets collectively had 1.45 million pension accounts summing to $386 billion (excluding CSC) at June 2023. These pension accounts constitute just 6.6 per cent of total accounts by number but 17.7 per cent by value. This reflects retirement accounts being of a much larger size, with pension accounts averaging around $308,000 versus $88,000 for accumulation accounts across the top 50 funds.

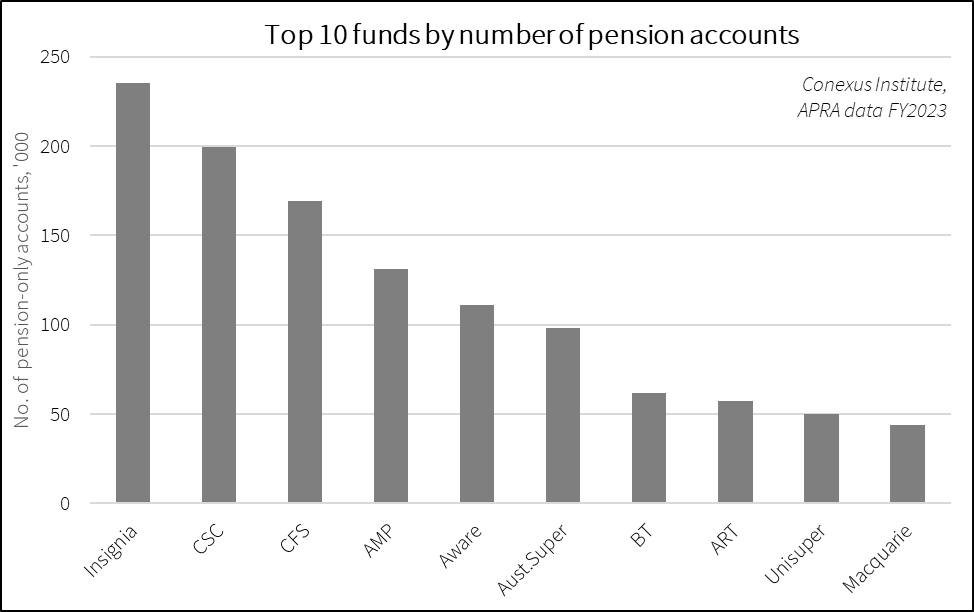

The chart below shows the top 10 funds by number of retirement accounts. This group collectively amounts to 80 per cent of the pension accounts of the top 50 funds. The most notable change compared with last year is the rise of Insignia to the position of largest provider of retirement accounts. This moves them ahead of CSC, with CFS ranked third.

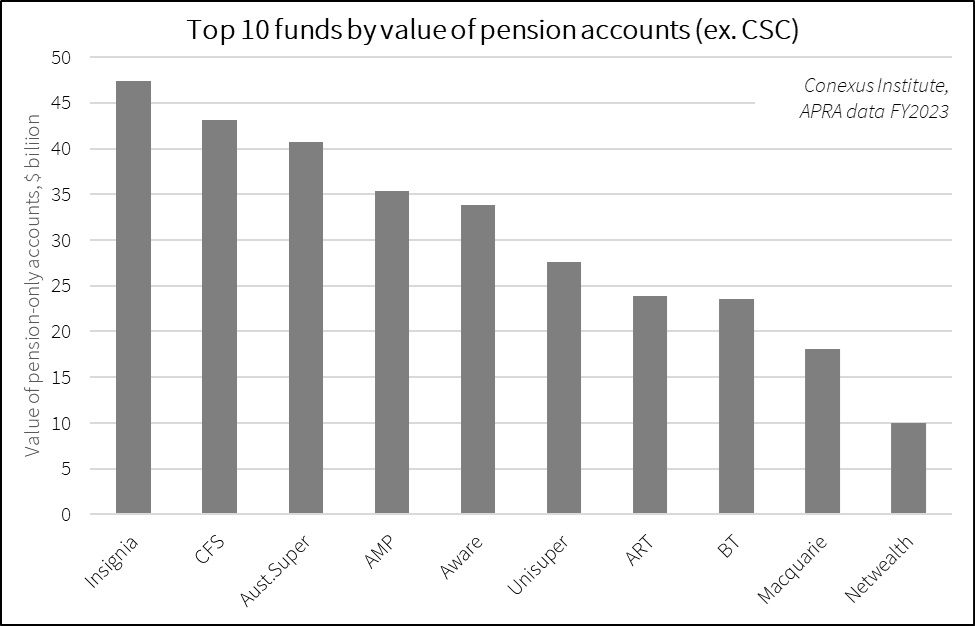

The chart below lists the top 10 funds by value of pension accounts (excluding CSC). While the deck chairs shuffle around relative to number of pension accounts, the names are the same except for the addition of Netwealth. Six funds have retirement assets between $25 billion and $50 billion. If these retirement assets were treated as separate funds, each would be sizable and in the ballpark of APRA’s indicated $30 billion – $50 billion scale figures.

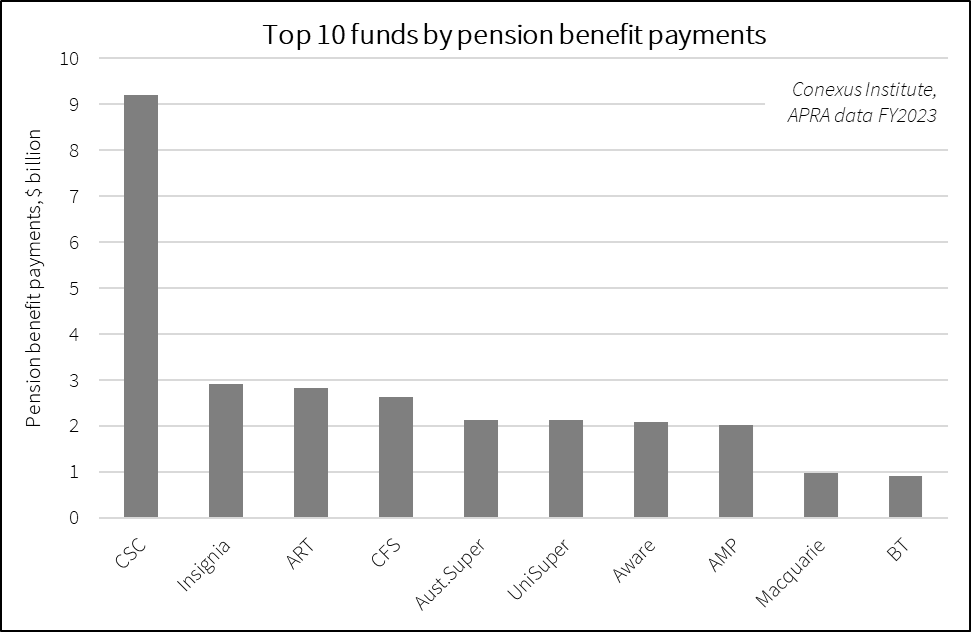

Over $34.2 billion in pension payments were made by the top 50 APRA-regulated funds during FY23. The top 10 funds accounted for 81 per cent of these payments, which are plotted in the chart below. The position of CSC as Australia’s largest pension fund is evident, with this fund alone accounting for 27 per cent of the benefit payments made by the top 50 funds by assets.

Retirement and fund operating models

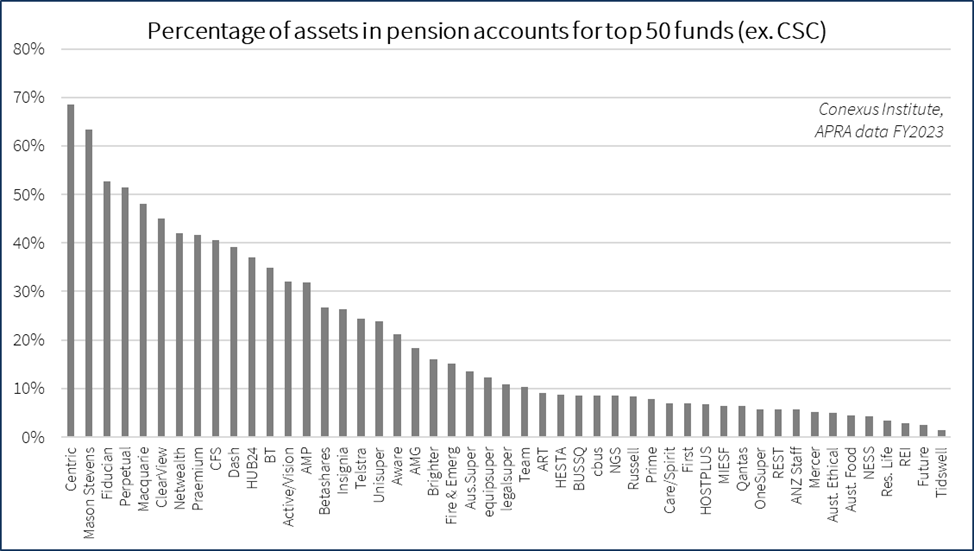

The dispersion across funds in exposure to retirement based on percentage of assets in pension accounts is stark, spanning from 1.4 per cent for Tidswell to 68.6 per cent for Centric (again CSC is excluded). This is illustrated in the chart below. However, the median is only 11.5 per cent (and 3.6 per cent by account numbers). We can see that many funds have quite low exposure to retirement in their membership mix.

This observation has consequences for meeting obligations under the Retirement Income Covenant, which requires fund trustees to develop retirement income strategies. The business case for developing retirement income strategies may be challenging for many APRA-regulated funds – at least until the superannuation system matures further.

The business case aspect is critical, and invariably involves a degree of cross-subsidisation where fees charged to accumulation members support development of retirement offerings. Funds with a smaller proportion of pension assets will have weaker business incentives to direct substantial resources towards developing retirement income strategies, and may find the cross-subsidisation challenge more confronting.

Following this logic, funds with a high proportion of pension assets may be better placed to establish a leadership position in the retirement market. This would particularly be the case for larger funds that can bring substantial resources to bear in developing retirement income strategies.

David Bell is executive director and Geoff Warren is research fellow at The Conexus Institute, a not-for-profit think-tank philanthropically funded by Conexus Financial, the publisher of Professional Planner.

David Bell is executive director and Geoff Warren is research fellow at The Conexus Institute, a not-for-profit think-tank philanthropically funded by Conexus Financial, the publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.