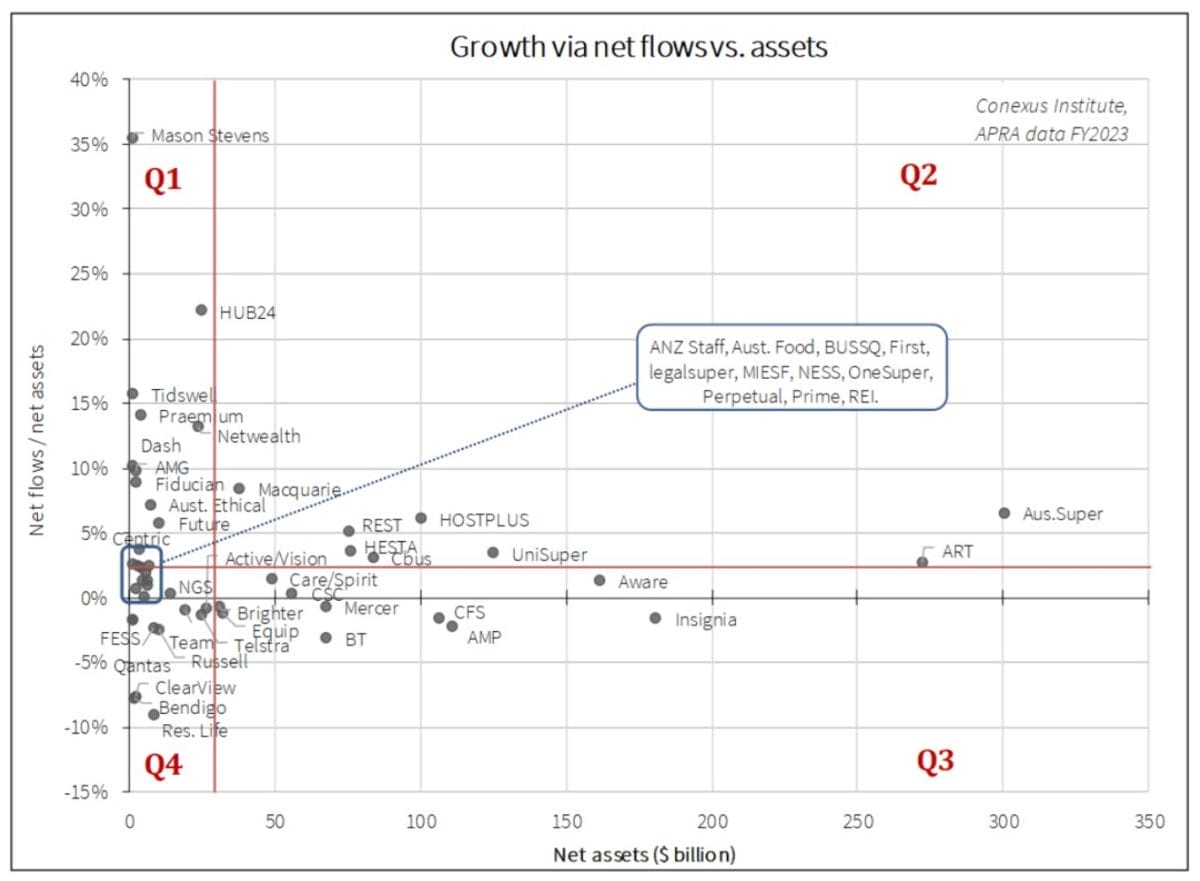

Combining size and flow rates creates a rich picture of the super fund landscape. In this article, we divide the universe of top 50 APRA-regulated funds by assets into four quadrants based on these two dimensions. The analysis reveals that some funds are in a strong position and their future is bright. For others, there is uncertainty and work ahead.

Exploring the super fund landscape

Our analysis involves taking APRA’s annual fund-level superannuation data, as described in previous articles on size and flow, and cleaning it up.

We then create a scatterplot for the top 50 funds that maps out growth rates arising from net flows (which exclude mergers and investment returns) against net assets under management. We then create four quadrants divided by two red lines.

The vertical line represents the $30 billion asset figure initially espoused by APRA for sufficient scale (although they later made mention of $50 billion as a marker). The horizontal line represents the aggregate 2.4 per cent growth rate via net flows experienced by the top 50 funds in FY2023.

Before we explore each quadrant, it is important to acknowledge that scale is a complex issue and the $30 billion marker is only notional. Indeed, research by The Conexus Institute (Do superannuation fund members benefit from large fund size?) argues that assets under management is not as important as implementing it successfully given a fund’s size, whatever it may be.

Quadrant one – Below scale but good growth

The table below lists the quadrant one funds with low scale but above-system flows. Apart from three more traditional industry funds with flows just above system rates (Prime, AMIST and NESS), the other funds display two themes.

First is a prevalence of funds that are successfully targeting the external financial adviser market, often supported by technologically advanced platform service offerings. HUB24 and Netwealth stand out as they could both reach the $30 billion scale mark quickly if they maintain their high growth rates. Many funds in this group also undertake other activities and have non-super product offerings that may assist with attaining scale for the overall business.

Second is that pure play sustainable investment offerings are capturing flows that are solidly above-system. This thematic is represented by Australian Ethical and Future Super.

| Fund | Net assets ($b) | Net flows/net assets |

| HUB24 | 24.8 | 22.2% |

| Netwealth | 23.8 | 13.2% |

| Future Super | 10.1 | 5.8% |

| Australian Ethical | 7.2 | 7.2% |

| Prime Super | 6.6 | 2.5% |

| Praemium | 3.8 | 14.1% |

| Centric | 3.5 | 3.7% |

| AMIST (Australian Food Super) | 2.9 | 2.5% |

| Fiducian | 2.3 | 8.9% |

| AMG Super | 2.1 | 9.9% |

| Tidswell | 1.4 | 15.8% |

| Dash | 1.1 | 10.2% |

| NESS Super | 1.1 | 2.7% |

| Mason Stevens | 0.9 | 35.5% |

Quadrant two – Good scale and good growth

Funds in quadrant two have a strong competitive position, benefitting from the combination of good scale and above-system growth through flows. AustralianSuper, Macquarie and to a lesser extent HOSTPLUS and REST are standouts for having strong flows along with sizeable assets.

It is a fascinating situation when the largest fund is also one of the fastest growers in this quadrant. AustralianSuper is benefitting from strong natural flows and a leading position in the marketplace for competitive flows, albeit moderating as explored in our flows article.

HOSTPLUS and REST appear to be benefiting from member demographics and access to first employment. Macquarie is similar to many of the funds in quadrant one which is performing strongly in the platform sector.

| Fund | Net assets ($b) | Net flows / net assets |

| AustralianSuper | 300.4 | 6.6% |

| Australian Retirement Trust | 272.1 | 2.8% |

| UniSuper | 124.7 | 3.4% |

| HOSTPLUS | 100.1 | 6.1% |

| Cbus | 83.7 | 3.1% |

| HESTA | 75.8 | 3.7% |

| REST | 75.3 | 5.1% |

| Macquarie | 37.7 | 8.5% |

Quadrant three – Good scale but sub-system growth

Within quadrant three, different stories emerge for large retail funds and large profit-for-member funds.

The four large retail funds (AMP, BT, CFS, and Insignia and Mercer) headlined competitive outflows as they face multiple sources of competition from both smaller fast growing retail platform groups and profit-for-member funds. This translates into negative (although not catastrophic) growth rates, thus leaving their scale largely intact. For these funds, the challenge is how to stem the outflows and develop a growth strategy.

In the profit-for-member segment, there is a cohort of above-scale funds that are experiencing below system growth, including the proposed Active/Vision Super, Aware Super, Brighter Super, Care/Spirit Super and CSC. In all these cases, growth through flows is quite close to zero (-1.2 per cent to +1.5 per cent range) and hence suggestive of a broadly stable competitive position rather than a major cause for concern.

| Fund | Net assets ($b) | Net flows / net assets |

| Insignia Financial | 180.6 | -1.6% |

| Aware Super | 161.4 | 1.3% |

| AMP | 111.0 | -2.2% |

| Colonial First State | 106.4 | -1.6% |

| BT Super | 67.4 | -3.1% |

| Mercer | 67.4 | -0.7% |

| Commonwealth Super Corp. | 56.0 | 0.4% |

| Care Super / Spirit Super | 48.9 | 1.5% |

| Equip Super | 32.0 | -1.2% |

| Brighter Super | 30.7 | -0.7% |

Quadrant four – Below scale and sub-system growth

Of the quadrant four funds, the biggest challenge in terms of sustainability might be faced by small funds below $10 billion (where APRA has expressed some concern) that are also suffering outflows. This sub-group includes Bendigo Super (being acquired by Betashares), Clearview, Qantas Super, MIESF and Resolution Life. Within this group, Qantas Super has announced its intention to seek merger partners.

For some funds in quadrant four, the scale issue is not too extreme. Although a merged Active Super/Vision Super and Telstra Super are both experiencing modest net outflows, they each have reasonable scale (both circa $25 billion).

The ability to draw on scale benefits through being part of a broader business also needs to be considered. Funds where superannuation is one component within a larger product or service offering include Betashares (once Bendigo Super acquisition is completed), OneSuper, Perpetual, Resolution Life and Russell Investments. Nevertheless, these groups might need to review what is required to ensure a sustainable superannuation offering.

Other quadrant four funds may be facing the question of whether they can succeed at current scale, given that any scale issues are unlikely to improve through business-as-usual given their net flow profiles. Funds listed in quadrant four with assets below $10 billion and growth through flows of 2 per cent or less include ANZ Staff Super, BUSSQ, legalsuper and REI Super.

| Fund | Net assets ($b) | Net flows / net assets |

| Active Super / Vision Super | 26.6 | -0.8% |

| Telstra Super | 24.9 | -1.2% |

| Team Super | 19.1 | -1.0% |

| NGS Super | 14.2 | 0.3% |

| Russell | 10.2 | -2.4% |

| Resolution Life | 8.7 | -9.1% |

| Qantas Super | 8.4 | -2.3% |

| BUSSQ | 6.1 | 1.3% |

| ANZ Staff Super | 5.9 | 1.0% |

| legalsuper | 5.5 | 2.0% |

| Perpetual Super | 5.0 | 0.0% |

| OneSuper | 4.6 | 1.4% |

| First Super | 4.0 | 2.4% |

| ClearView Retirement Plan | 2.1 | -7.6% |

| REI Super | 2.1 | 0.7% |

| Bendigo (to become BetaShares) | 1.5 | -7.8% |

| MIESF | 1.0 | -1.7% |

| Fire & Emergency Services Super | 0.9 | -1.6% |

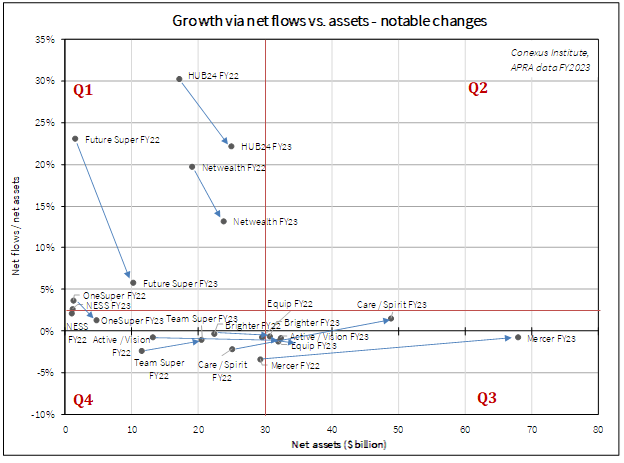

Shifting across quadrant boundaries

Of the 50 funds featured in the previous chart, only a handful were in different quadrants a year ago including Brighter, Equip, Mercer, NESS Super, OneSuper and a merged Care/Spirit Super. The chart below plots these “quadrant shifters” along with a selection of funds that saw substantial moves over FY23, or will do upon completion of mergers.

Of the funds shifting quadrants:

- The drop in OneSuper’s growth rate took it from quadrant one to quadrant four. Perhaps this was related to its integration of ING Super, which nearly quadrupled the size of the fund.

- NESS Super shifted in the opposite direction from quadrant four to quadrant one by managing to improve its growth rate enough to meet our threshold.

- Equip Super’s asset growth just shifted them across the asset threshold of quadrant four into quadrant three.

- Mercer’s merger with parts of BT’s super businesses were transformational, leaping from just inside quadrant four to well into quadrant three.

- Brighter shifted to quadrant three after completing acquisition of Suncorp’s super operations.

- Completion of Care Super and Spirit Super merger would also be transformational (as would Mine Super and TWU Super to form Team Super, although to a lesser extent).

Two broad themes emerge from these case studies. The first is how mergers can deliver an instant shift in scale and transform the business.

Second is that high growth rates generally subside over time, partly due to the denominator effect of a higher asset base, and potentially because competitors take notice and/or new innovations arrive.

Future Super is an interesting case study that combines both effects where multiple mergers (with Guild and Smart Future) added significant scale, but appear to have diluted its growth rate. Whether HUB24 and Netwealth can continue their growth rates going forward will be interesting to see.

David Bell is executive director and Geoff Warren is research fellow at The Conexus Institute, a not-for-profit think-tank philanthropically funded by Conexus Financial, the publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.