While it is natural to focus on assets under management (AUM) like we did here, net flows are just as, if not more, important. The net flows inform aspects like future scale, ability to invest in illiquid assets, and the extent to which a fund needs to source assets.

We took APRA’s annual fund-level superannuation data and ‘cleaned it up’. We aggregate multiple providers under the same parent company (e.g. Insignia Financial), account for announced merger intentions (e.g. Spirit Super and Care Super), and exercise judgement on special situations (such as the Commonwealth Superannuation Corporation’s asset levels given its significant defined benefit operations). When analysing flows we remove the one-off impact of successor fund transfers and combine net flow positions of merging funds. Growth due to investment performance isn’t explored in this article given it is not based on member account activity.

Applying APRA’s data and understanding flows

We split the net flow picture into two categories: ‘natural flows’ and ‘competitive flows’. Natural flows aggregate contributions and benefit payments, which proxy for the natural industry growth rate. Competitive flows focus on net roll-in/roll-out activity and hence member switching, and are broadly a zero sum game. One exception is net switching activity between APRA-regulated funds and the SMSF sector. This was small in FY23 when a net $3.5 billion rolled out of APRA-regulated fund into SMSFs, representing only 0.15 per cent of total assets ($2.3 billion rolled out in FY22).

Natural flows

Net natural flows for the largest 50 APRA-regulated super funds were about $48 billion in FY23, an increase of about 4 per cent on FY22. At a system level the superannuation guarantee (SG) rate of 10.5 per cent (which has risen to 11 per cent in FY24) more than offsets the outflows resulting from pension accounts built up during periods where lower SG rates were in place. This represents about 2.1 per cent natural growth based on the estimated $2.24 trillion total assets in the APRA-regulated super funds sector.

While 39 (78 per cent) of our top 50 fund sample funds experienced positive natural flows, for many funds the natural flow was marginal. Only 11 funds (22 per cent of the 50) exceeded the 2.1 per cent average growth rate from natural flows. The percentage net natural flow position of each fund is determined by its member demographics, specifically the balance between accumulators and retirees.

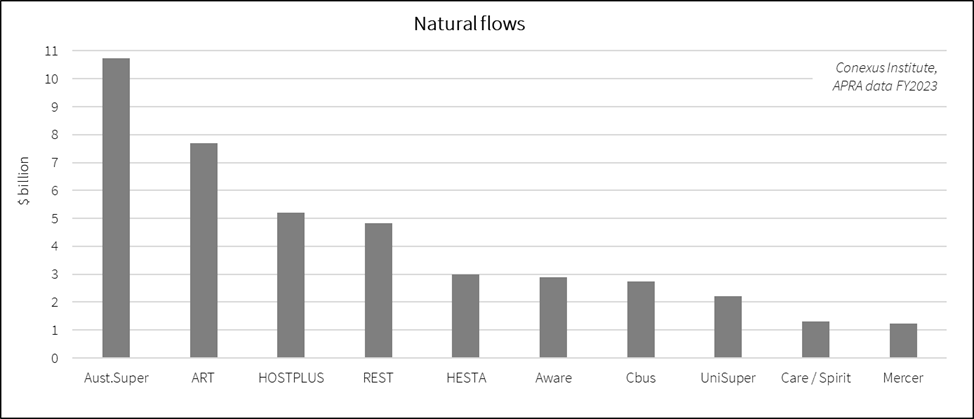

From a dollar perspective, natural flow is further linked to the size of the fund. The chart below shows the top 10 funds by natural flows in dollars, which together constituted nearly 90 per cent of total natural flows.

Source: APRA, Conexus Institute.

The concentration of natural flows into the large profit-for-member funds is evident in the chart. Indeed, the big eight profit-for-member funds took 80 per cent of the natural flows, with the two mega-funds of AustralianSuper and ART leading the pack. The limited presence of retail funds on this chart is explained by demographics – these funds have an older membership. The broad numbers shouldn’t change too much year-on-year as fund demographics tend to move slowly.

Competitive flows

The competitive flow landscape is far more complex with many factors at play across different market sub-segments. Some of these factors include:

- Impact of investment performance and resulting publicity – good and bad – arising in particular from the YFYS (Your Future, Your Super) performance test;

- Marketing, branding and member acquisition activities;

- Media coverage of developments such as greenwashing accusations, cybersecurity breaches and fund mergers or terminations;

- Fund switching as members change jobs, accounting for impact of fund stapling that operated for a full year in FY23; and

- Decisions made by financial advisers.

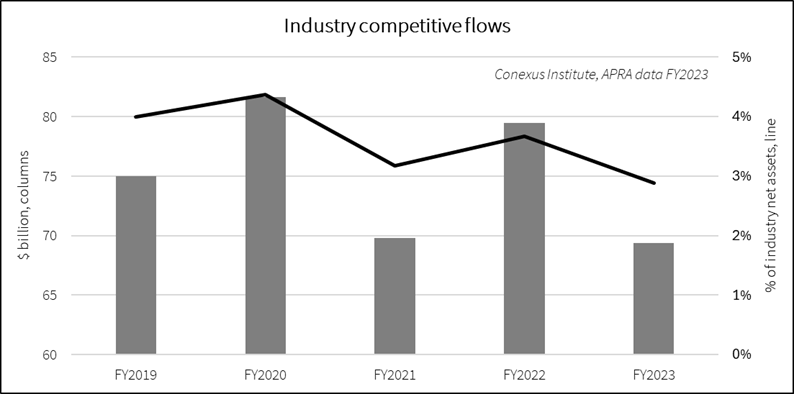

Our first observation from the data is that the amount of member switching activity has been on the decline, whether measured in dollars or percentage of industry size.

A challenge is posed by this chart for the value in spending on brand and marketing. If the size of the member switching pool is shrinking, spending more on brand and marketing (something we plan to investigate further) could yield less benefit for both funds and at the system-level for consumers.

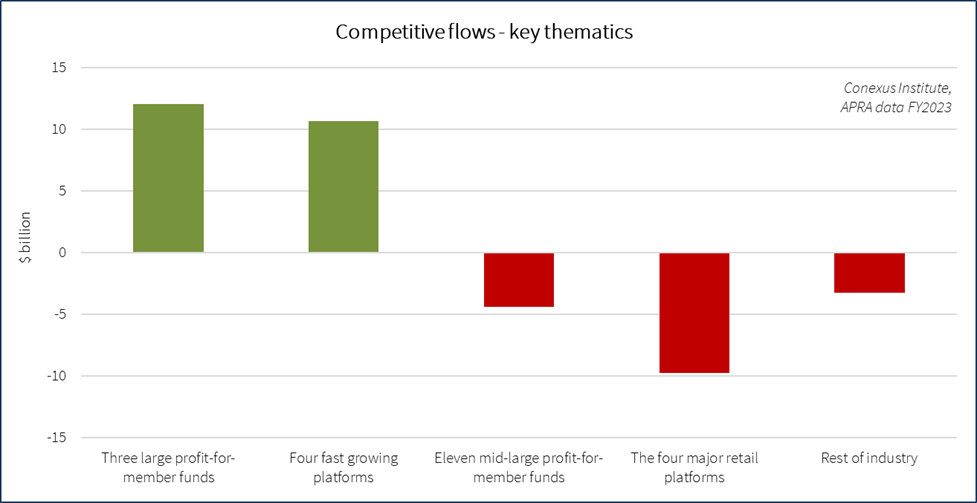

Before investigating individual fund outcomes, let’s explore some key thematics. The chart below dispels the simple anecdote that funds are flowing from retail funds to profit-for-member funds.

The sub-groups in the chart are comprised of (ordered from best to worst):

- Three large profit-for-member funds: AustralianSuper, UniSuper, and Hostplus;

- Four fast-growth platforms: HUB24, Macquarie Super, Netwealth, and Praemium;

- Eleven mid-large profit-for-member funds: Cbus, ART, Active/Vision, HESTA, NGS, Team Super, Brighter, Care/Spirit, equipsuper, Aware Super, and REST;

- Four major retail platforms: BT, CFS, AMP, and Insignia.

The chart above reveals that the ‘winners’ comprise idiosyncratic winners amongst the profit-for-member funds sector and success stories amongst small-to-mid-sized retail platforms. Meanwhile, many profit-for-member funds are losing when it comes to competitive flows.

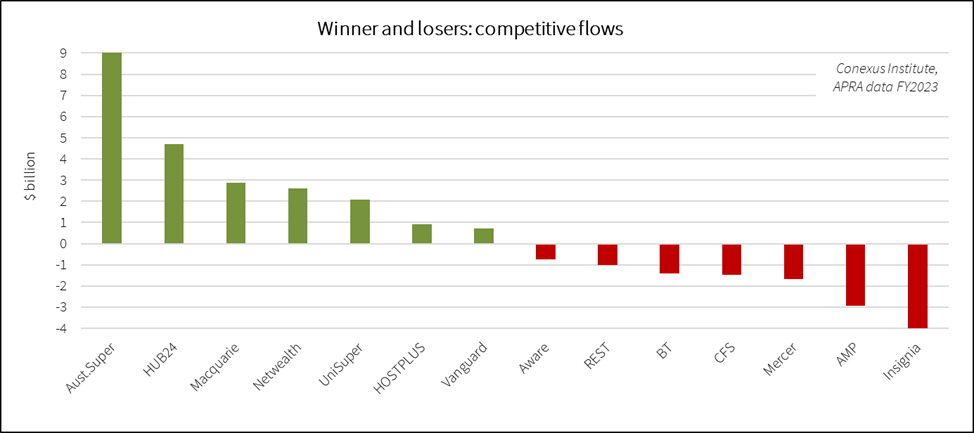

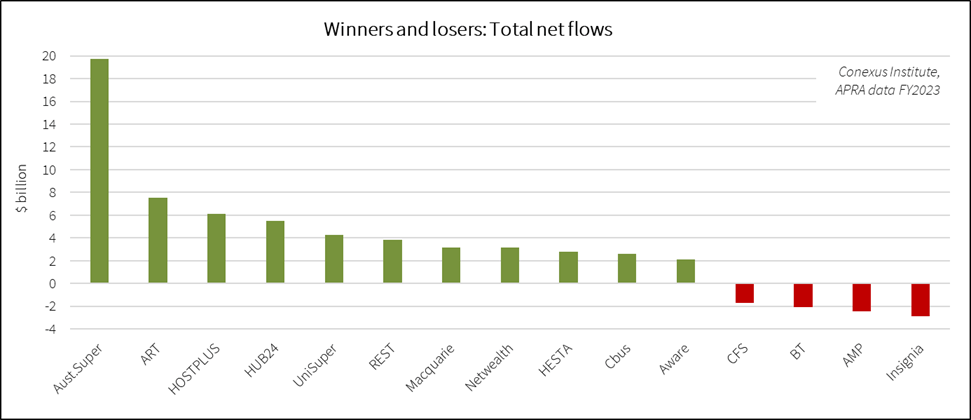

The individual winners and losers chart below adds further colour to some of the thematics. One additional highlight is the performance of Vanguard. Despite it not yet being part of the top 50 funds by asset, we include Vanguard on the chart where it comes in at number seven by dollar inflows.

The competitive flows landscape is less stable than that for natural flows. Analysing the data we found some significant year-on-year changes in competitive flow positions:

- AustralianSuper’s position in competitive flows, while still a strong leader, diminished significantly during FY23, falling from $15.4 billion to $9 billion. When we look deeper, this is largely due to roll-ins. Simply put, a lot less people switched to AustralianSuper in FY23.

- Large retail funds, while still losing in terms of competitive outflows, are seeing their losses abate. AMP (+$1.8 billion), BT (+$1.7 billion), and CFS (+$0.8 billion) all experienced significant year-on-year improvement.

- REST (+$0.6 billion) was another notable improver. Mercer’s position deteriorated (-$0.7 billion) as did ART’s (-$0.9 billion); although for both this may potentially relate to member activity during merger onboarding.

Net flows in FY23

Net flows are simply an aggregate of natural flows and competitive flows. Total reported industry net flows were $54 billion. Eleven funds received 115 per cent of the industry flows, which means the rest of the industry is in net outflow. AustralianSuper alone receiving 37 per cent of flows amounting to nearly $20 billion. Again, the theme emerges of concentration of inflows into the hands of a modest number of funds.

Meanwhile, outflows are concentrated in the four large retail groups. As well as losses through competitive flows, the relatively high portion of pension accounts adversely impacts their natural flows.

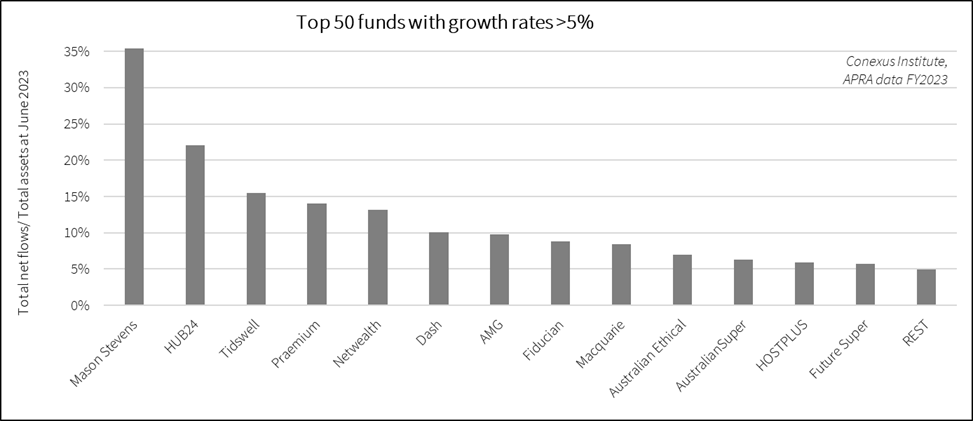

We finish by considering overall flow-related growth rates through dividing net flows by AUM. The chart below of funds growing at more than 5 per cent p.a. through flows provides a fascinating snapshot. The nine fastest growers have all focused their operational models on servicing the adviser community. Another theme relates to ESG and sustainability, with Australian Ethical and Future Super posting growth above 5 per cent.

Of the more established funds, AustralianSuper’s growth profile remains significant given its size, although substantially lower than FY22 (when it was close to 10 per cent). Appearances are also made by Hostplus and REST, which dominate the ‘first employment’ sectors of hospitality and retail.

David Bell is executive director and Geoff Warren is research fellow of The Conexus Institute, which is philanthropically funded by Conexus Financial, publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.