APRA’s annual release of fund-level superannuation statistics is the perfect time to reflect on the state of Australia’s superannuation industry. There are some fascinating trends, some of which seem set to persist.

The first thing we do is to take the APRA data and ‘clean it up’. We aggregate multiple providers under the same parent company (e.g. Insignia Financial), account for announced merger intentions (e.g. Spirit Super and Care Super), and exercise judgement on special situations (such as Commonwealth Superannuation Corporation’s asset levels given its significant defined benefit operations).

Working off net assets, we estimate industry size as captured by APRA-regulated funds to be about $2.2 trillion*. This is about 10 per cent larger than just under $2 trillion a year ago.

The 2Cs: consolidation and concentration

It was another year of fund mergers with a number completed, some progressing, and further mergers announced. There were also some small fund terminations. A partial offset to the consolidation activity is a sprinkling of new entrants with quite targeted offerings. An example is Vanguard, with a focus on a low-cost product targeted at financial advisers and directly to consumers.

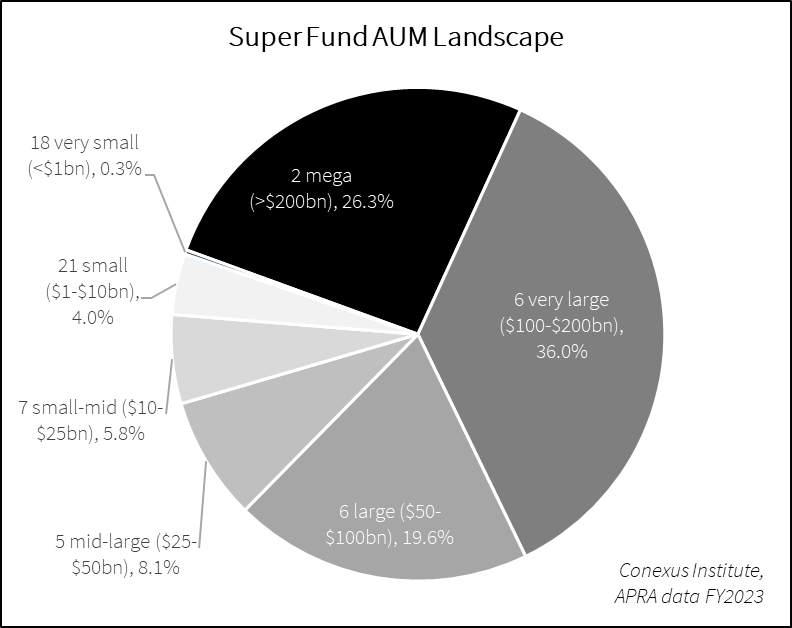

Consolidation combined with a small number of new entrants with negligible assets means that industry concentration is increasing. We define ‘big’ funds as including mega funds (>$250 billion net assets), very large funds (>$100 billion), and large funds (>$50 billion). This group continues to increase its market share at the expense of the medium and small fund segments. The overall landscape appears in the diagram below.

When we analyse year-on-year change, there has been a small increase in the footprint of big funds, from 81.5 per cent to 81.8 per cent. The real growth story is within the big fund segment. The eight big not-for-profit funds increased their market share of industry assets by nearly 2 per cent (from 52.9 per cent to 54.8 per cent).

New entrant to the ‘big fund club’

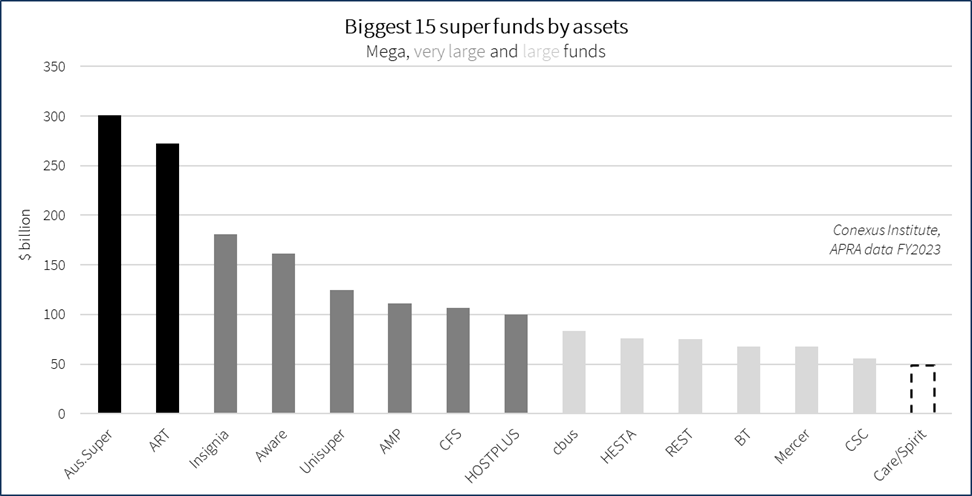

It looks likely that 2024 will see a new member of the “big fund club” with the merged Spirit Super/Care Super making the cut as member #15, allowing for some positive market performance. Last year we suggested that new members into this club seemed unlikely, partly because many candidate mid-size funds (like Spirit Super) were already bedding down mergers. The preparedness of Spirit Super to ‘go again’ speaks to the value placed on further scale amongst those trustee directors.

The 2023 financial year saw Hostplus join the group of very large funds, on the back of strong net inflows and its merger with Maritime Super.

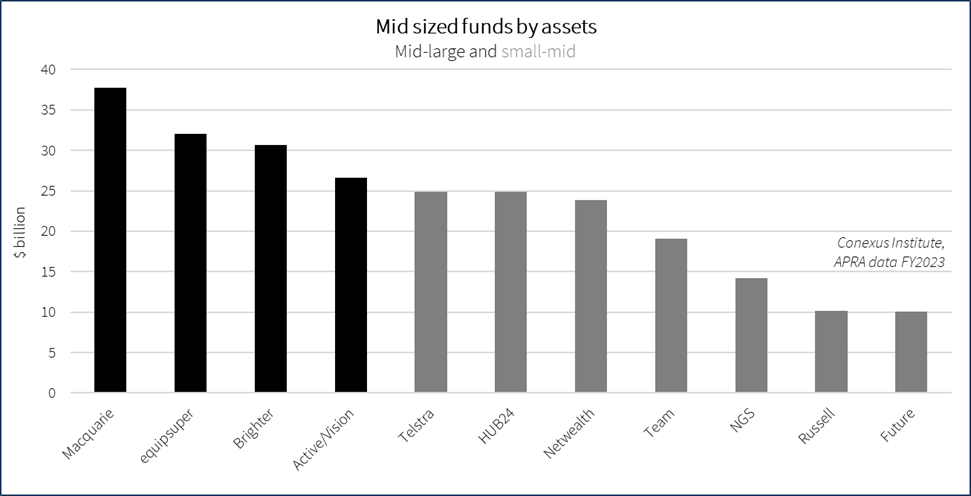

There are some interesting dynamics in the mid and small-sized fund sector. The footprint of this sector increased by about one percentage point to 13.9 per cent, with multiple drivers at play. There were mergers announced, including between Active Super and Vision Super, Mine Super and TWU Super to form Team Super, and Future Super staged multiple mergers with Smart Future Trust and Guild Retirement Fund. There were a few notable cases of growth being driven by strong net inflow, including Macquarie Super, HUB24 and Netwealth experiencing significant inflows via financial advisers.

To complete the picture, 21 very small funds manage between $1 billion and $10 billion, accounting for about 4 per cent of industry assets. This is down from 5.2 per cent last year. This fall occurs despite new entrants such as Vanguard.

Growth drivers distinguish fast growing funds

There were some amazing growth stories in FY23. Analysing these we found a disperse range of underlying growth stories.

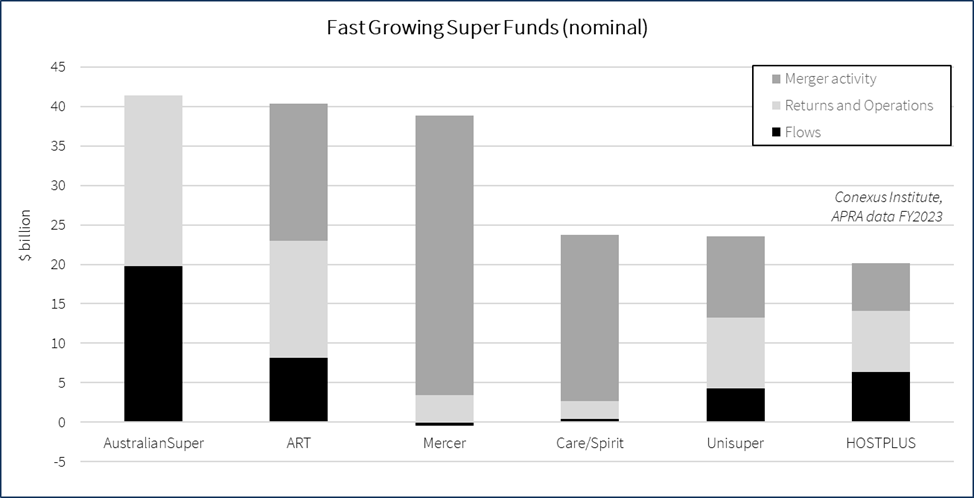

Through the lens of growth in dollars, AustralianSuper reigned again. But it was a closer race than one might have expected once mergers are accounted for.

The net assets of AustralianSuper grew by over $41 billion in FY23. ART grew by nearly the same amount at $40 billion, while Mercer was a close third with $38 billion.

However, the composition of growth amongst these funds reveals the dominant position of AustralianSuper in terms of competitive flows where members choose to switch from another fund.

AustralianSuper clearly grew the most in dollar terms without undertaking any merger activity, and the associated operational implementation cost and effort (though some funds like ART may argue they have established processes which minimise the operational impact). A merger transformed the size of Mercer and will do likewise for a merged Care Super/Spirit Super.

Mergers remain transformational

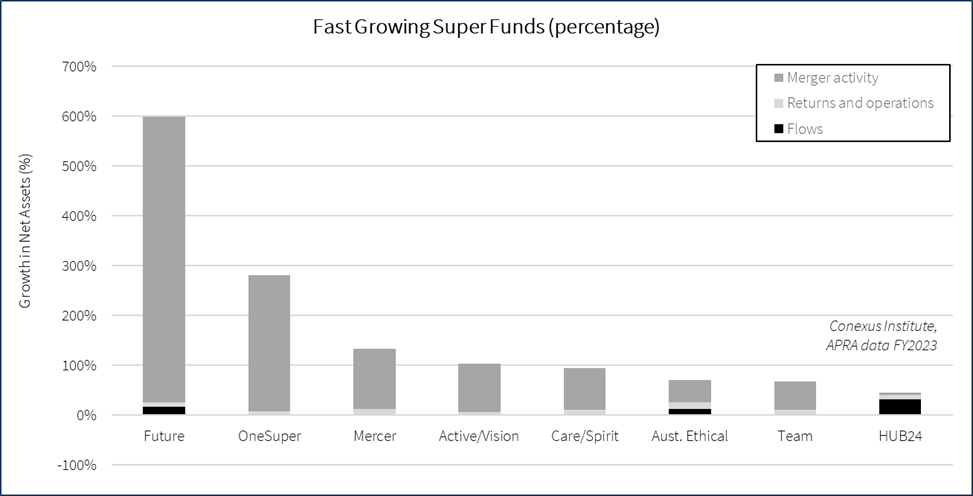

The percentage growth lens presents some amazing, and in some cases transformational, growth stories.

Future Super’s mergers with Smart Future and Guild increased assets by nearly 600 per cent in a move that transforms them from being a small fund with strong net inflows to being part of the small-mid fund segment.

OneSuper’s integration of ING Super substantially enhanced their scale, although they remain a small fund at $4.6 billion net assets under management.

The mergers of Mercer with BT Super (completed), Vision and Active (to be completed this year), Spirit Super with Care Super (to be completed), Australian Ethical with Christian Super (completed), and Team Super (Mine Super and TWU Super) all reflect the power of mergers to significantly increase scale.

HUB24 stands out on this chart as a high growth fund largely achieved through competitive growth. The chart reveals the next challenge for some of those merged entities: to establish a sustainable net inflow profile.

Changing landscape in 2023

Overall, not all that much changed in 2023 in terms of the broader landscape.

The big funds increased their market share at the margin, particularly the big not-for-profit funds, a merger between Spirit Super and Care Super will create a new member of the “big fund club”, while the small fund sector lost market share.

However, we have seen that there are fascinating dynamics at play at the individual fund level, particularly in the mid-sized segment.

What to expect in 2024 and beyond

Changes in the large fund landscape tend to be slow as the denominator effect of large existing asset size is influential. The emergence of another mega fund requires a merger between two very large funds or possibly a very large fund and a large fund. A new large fund requires the merger between two medium funds.

However, the realistic number of suitable merger candidates is small after accounting for fund types (difficulty of a profit-for-member fund with a relatively small range of products to merge with a platform-based for-profit fund), and the fact that many funds are digesting substantial merger activity and may be hesitant to take on further mergers.

Pressure remains on small funds, where factors such as APRA’s data and regulatory activities, the requirements of the Retirement Income Covenant and cybersecurity all weigh heavily. This is where further consolidation activity remains most likely as the incentives are strongest.

*This article was edited on 19 January 2024 to change billion to trillion, along with clarifying the Active Super/Vision Super merger is to be completed.

David Bell is executive director and Geoff Warren is research fellow of The Conexus Institute, which is philanthropically funded by Conexus Financial, publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.