Who are Australia’s largest retirement funds? Here, we put accumulation aside and focus on retirees.

Applying APRA’s data and understanding inflow

Like other recent articles (scale, inflows, and super fund landscape) based off APRA’s annual fund-level data set (which relates to FY22), we aggregated offerings and accounted for announced mergers. We use information about assets and accounts in the tax-free phase as our measure of members in retirement. This potentially understates the true number of retirees, some of whom may not have transitioned their assets across from accumulation to drawdown. We also analyse data on benefit payments to members. This helps to corroborate our findings based on tax-free phase account data.

Retirement accounts, assets and benefit payments

Just 6.3 per cent of members (just under 1.4 million) are in the retirement phase but, illustrating the power of ongoing savings and compounding investment performance, this represents nearly half a trillion dollars, or 22.3 per cent of industry assets.

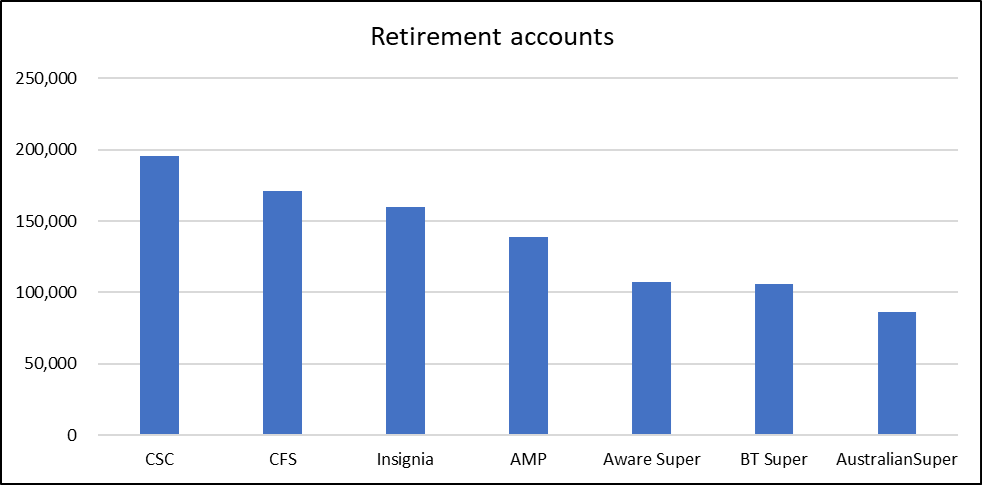

The seven largest funds, in terms of accounts, make up about 71 per cent of all industry retirement accounts.

Note that the BT Super data does not account for the transition of accounts across to Mercer Super.

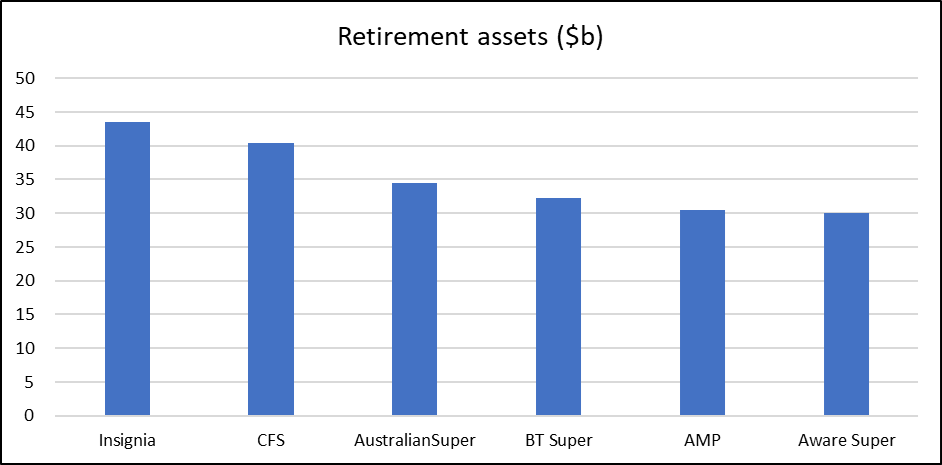

When it comes to assets in retirement accounts the deck chairs shuffle slightly. Unfortunately, the data does not allow us to accurately adjust Commonwealth Superannuation Corporation’s (CSC’s) assets (regulatory reporting requires them to report defined benefit liabilities as assets). Six funds have retirement assets in excess of $30 billion. Put another way, if these retirement assets were treated as separate funds, each ‘new’ fund would exceed APRA’s indicate sustainable scale figure.

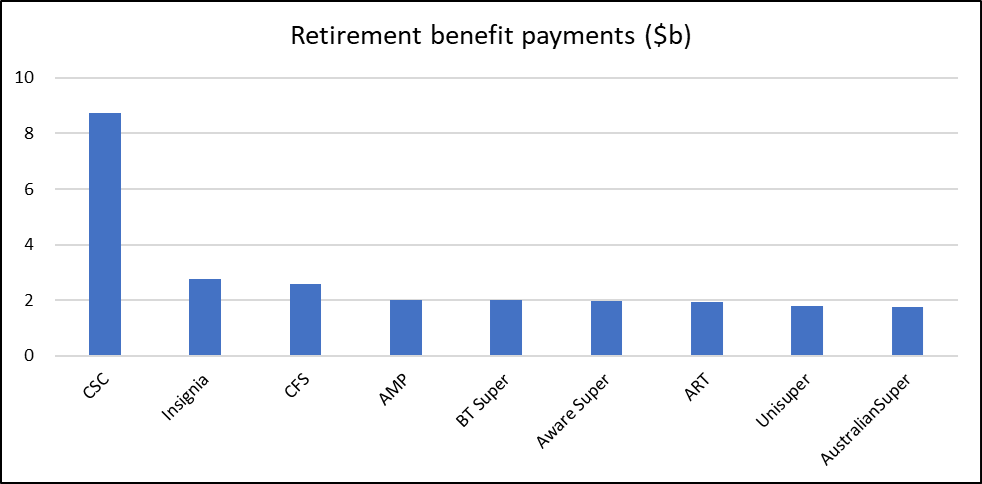

Last year over $33 billion in pension payments were paid out by APRA-regulated super funds. Nine funds account for nearly 80 per cent of these payments. Here the position of CSC as Australia’s largest pension fund, underpinned by the management of a sizable defined benefit book, becomes clearer.

Retirement and fund operating models

For some funds, pension-phase members make up a small component of their membership while, for other funds the share is large. This has consequences for the development of retirement income strategies.

The best retirement income strategies will consist of high-quality product-based solutions combined with a level of service which can result in an outcome tailored to the member’s circumstance.

The business case aspect is critical (as highlighted by former Unisuper CEO Kevin O’Sullivan) and invariably involves a degree of cross-subsidisation.

For those funds with a small proportion of pension assets the cross-subsidisation challenge is more confronting. Those funds with a high proportion of pension assets face an easier decision. Further, they have the opportunity to develop a leadership position should the retirement segment evolve into a competitive sector with a high levels of consumer choice.

There exists significant dispersion amongst funds based on pension proportions of membership.

Top ten super funds based on pension asset proportion (note this excludes CSC due to data constraints):

| Pension asset proportion | |

| Encircle Super | 64.2% |

| Perpetual | 51.4% |

| Fiducian | 51.1% |

| ClearView | 50.4% |

| Macquarie | 47.8% |

| Oasis | 45.3% |

| Netwealth | 41.1% |

| CFS | 40.8% |

| Praemium | 40.1% |

| HUB24 | 34.2% |

Some of the names in this list may be unexpected. All these groups are platforms and are generally used by financial advisers to provide tailored portfolio solutions for their clients. For these groups it is likely important that they continue to develop a high quality retirement offering with products, tools and functionality which are valuable to advisers. The leadership question mark is whether these platform-based services can directly attract members, particularly important given shrinking adviser numbers.

Bottom ten super funds based on pension asset proportion (note this excludes CSC due to data constraints):

| Pension asset proportion | |

| Qantas Super | 5.9% |

| Australian Ethical | 5.7% |

| ANZ Staff Super | 5.7% |

| AMIST | 4.7% |

| Smart Future | 3.9% |

| OneSuper | 3.5% |

| Rei Super | 2.7% |

| Future Super | 2.0% |

| Tidswell | 1.6% |

| Guild | 0.6% |

Most of these funds have a young demographic created through the nature of their workforce or their segment-based marketing strategies. For these funds the business case for significant investment into their retirement income strategies is more challenged.

Leave a Comment

You must be logged in to post a comment.