APRA’s annual release of fund-level superannuation statistics provides a good opportunity to reflect on the state of Australia’s superannuation industry. There are some fascinating trends, some of which seem set to persist.

Cleaning the data

From the APRA data we did the following:

- Aggregated multiple providers under the same parent company (e.g. Insignia Financial)

- Accounted for announced merger intentions

- Estimated assets for CSC based on assets managed rather than defined benefit liabilities

The landscape

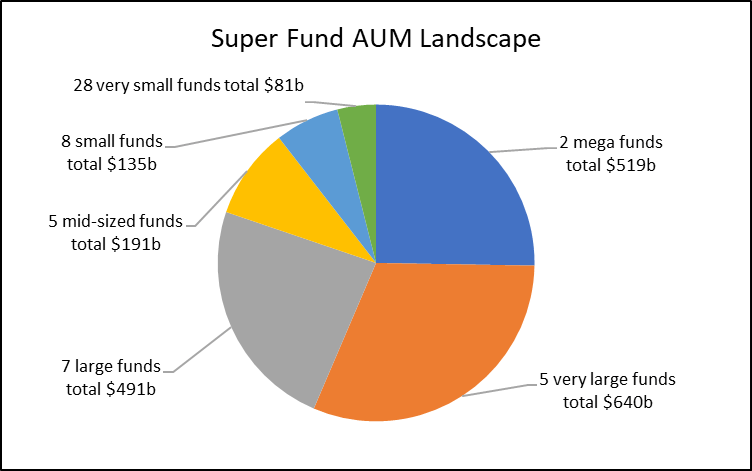

Most super assets (excluding SMSFs of course) are managed by a reasonably small number of funds, as highlighted in the chart below.

Aggregating the numbers in the chart there emerges fourteen funds in the “big fund club” (the “Big 14”), who manage just over 80 per cent of industry assets. We created our own definitions to divide the Big 14 into three sub-categories (all approximations): mega (>$250 billion), very large (>$100 billion), and large funds (>$50 billion).

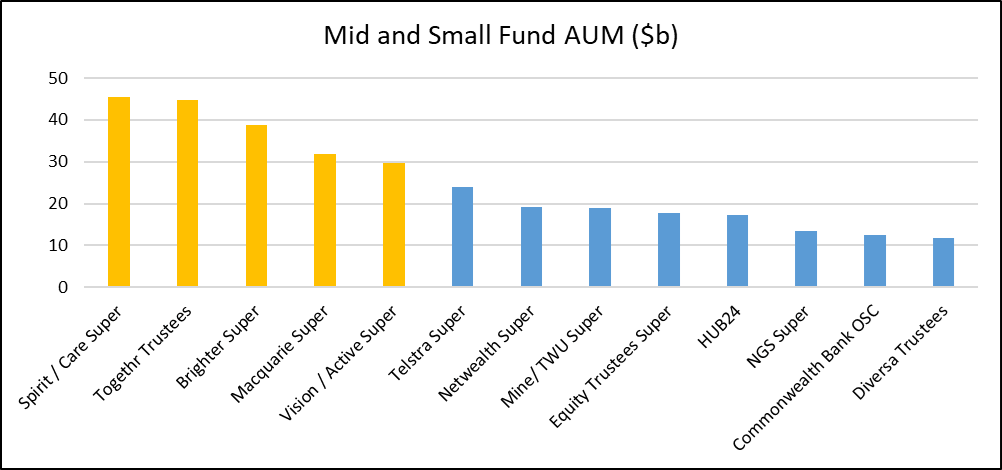

The remaining 20 per cent of industry assets are managed by (again, our definitions) medium (>$30 billion), small (>$10 billion) and very small funds (<$10 billion). We omit to include very small funds in the chart below.

Changing landscape in 2022

There are three important highlights of 2022. The first was the clear emergence of a mega fund category, where AustralianSuper (which continues to benefit from huge net inflows) was joined by Australian Retirement Trust (the merger between Sunsuper and QSuper). The second was Mercer Super joining the big fund club through its acquisition of some of BT’s super operations. The third is reduced numbers of very small funds, due to mergers.

What to expect in 2023 and beyond

Beyond the shrinking number of very small funds, the fact that there were only two significant changes to the super fund landscape suggests that, especially with respect to the big fund club, things move slowly.

Could we see the emergence of another mega fund? This would require a merger between two very large funds or possibly a very large fund and a large fund. However, the realistic number of candidate mergers is small once you account for fund types (it is difficult for a profit-for-member fund with a relatively small range of products to merge with a platform-based for-profit fund). Further, many of the Big 14 funds are digesting substantial merger activity and may be hesitant to take on the size of merger required to create a third mega fund.

Could we see a new entry into the big fund club? This would require mergers amongst mid-sized funds or, in some cases, a mid-sized and a small fund. However, the same problems arise once more: there are few natural mergers due to fund structures, and a number of mid and small-sized funds are bedding down their own mergers.

An interesting question is the pathway for small funds to exceed the $30b threshold cited by APRA. For most members of this category substantial growth would be required, making a merger, possibly multiple mergers, the most realistic pathway.

Overall, we expect the shape of the industry to evolve slowly. System flows and performance will have impact, but step-change comes through merger activity. But this is an industry which can surprise. Not many people predicted the merger between QSuper and Sunsuper, or tipped Mercer Super to be the fund to pick up some of BT’s super assets.

Leave a Comment

You must be logged in to post a comment.