When APRA releases its fund-level superannuation statistics for APRA-regulated funds the race is on to analyse assets under management. This measure translates directly to scale and is the measure that garners most attention. However net inflow is just as, if not more, important. It informs future scale as well as the ability to invest in illiquid assets.

Applying APRA’s data and understanding inflow

We took the APRA dataset (for FY22) and did the following:

- Removed the one-off impact of successor fund transfers

- Aggregated multiple product offerings under the same parent company (e.g. Insignia Financial)

- Accounted for announced merger intentions (however we were unable to aggregate the impact of BT’s assets transition into Mercer Super)

We have broadly split the total inflow picture into two categories: ‘natural flows’ and ‘competitive flows’. Natural flows aggregate contributions and benefit payments, while competitive flows focus on net roll-in/roll-out activity.

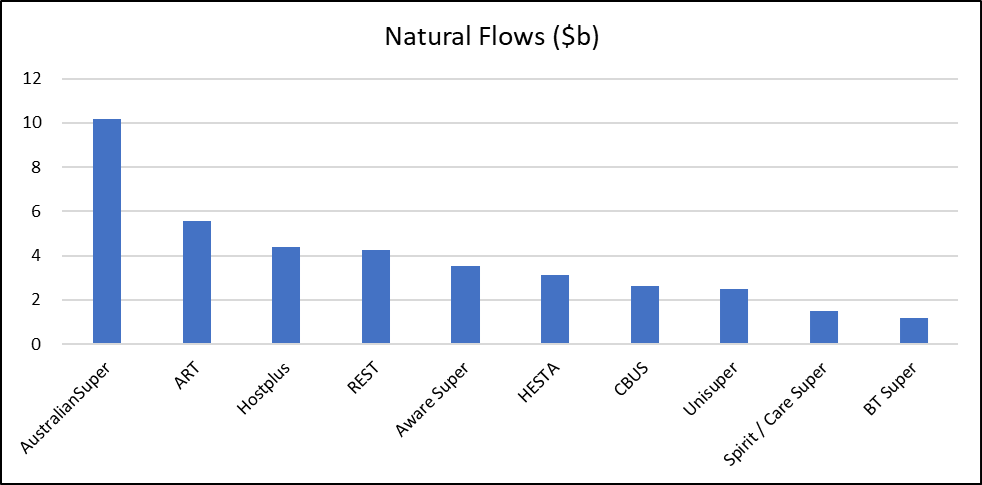

Natural flows

Net natural flows for the system (applied to large super funds, leaving SMSFs aside) were about $46 billion in 2022. In aggregate the SG rate of 10.5 per cent (scheduled to rise to 11 per cent at the end of this financial year) more than offsets the outflows resulting from pension accounts built up during periods where lower SG rates were in place. This represents about 2.2 per cent natural growth (investment performance is an additional source of industry growth), based on the estimated $2.05 trillion total assets in the APRA-regulated super funds sector.

While most funds (77 per cent) experienced positive natural flows, for many funds the natural flow was marginal. Ten funds received nearly 85 per cent of total natural flows.

There aren’t too many surprises in the above chart. Natural inflows, when measured in dollars, are influenced by fund size and the ratio of workers to retirees.

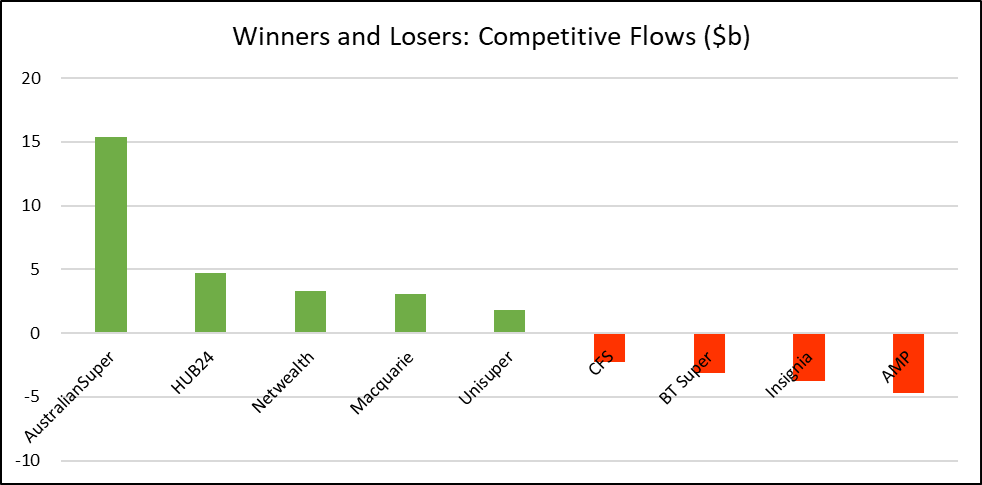

Competitive flows

The competitive flow landscape is far more complex and there are many factors at play given different market segments. Some examples of these factors, which are difficult to quantify, include:

- Potential switching as member’s change jobs. This is a natural headwind for funds with a high proportion of first job members. This dynamic may change in the presence of the Your Future, Your Super stapling reforms

- The impact of investment performance and resulting publicity, good and bad

- The marketing, branding and member acquisition activities of funds

- Flows between the institutional and SMSF sectors (last year net $2.3 billion rolled out of APRA-regulated funds into SMSFs)

- Decisions made by advisers relating to platform choice and adoption of not-for-profit funds.

The data suggests that the simple anecdote of funds flowing from for-profit retail funds into profit-for-member funds is outdated. There are strong winners in the for-profit space likely taking assets away from for-profit peers.

There is a huge amount of churn relating to competitive flows. Total one-sided flows (to avoid double-counting) were around $76 billion in FY22 (3.4 per cent of assets) but the net flow was only $6.5 billion. Only 30 per cent of funds experienced positive net competitive inflows, and there is a small set of clear winners and losers.

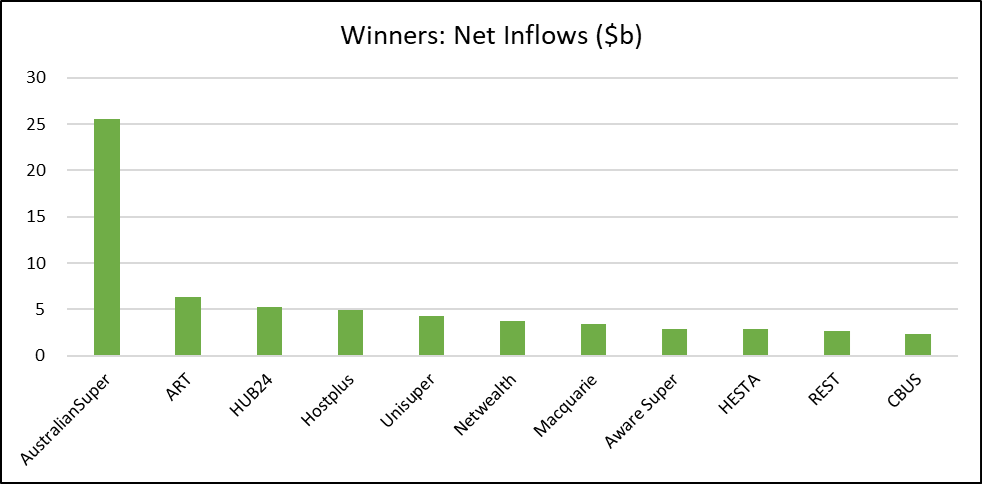

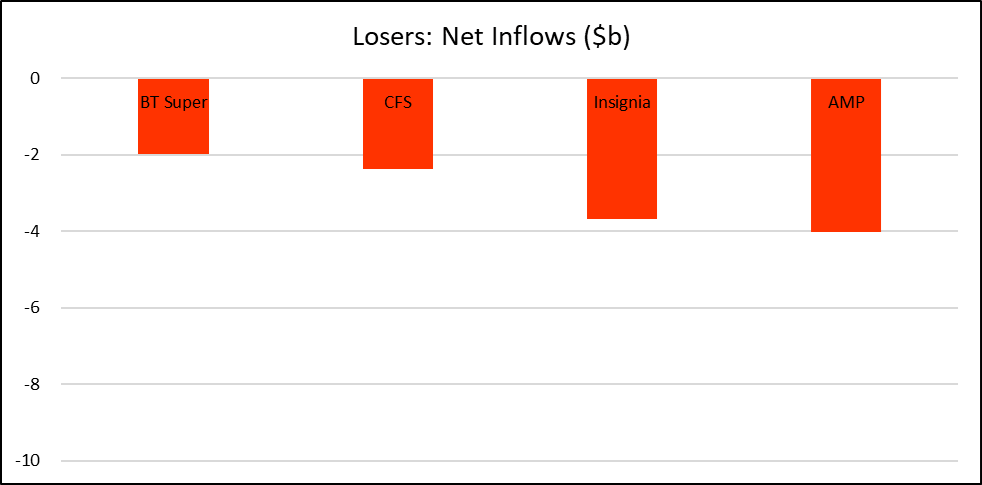

Net inflows in FY22

Net inflows are simply an aggregate of natural flows and competitive flows. Total net industry flows are $52 billion (slightly different to the $46 billion natural flow due to SMSF flows and reporting methodology). Eleven funds received 123 per cent of this flow, meaning that in aggregate the rest of the industry is in outflow. The AustralianSuper story is amazing: its net inflow is nearly the size of a medium fund (as defined in our industry size article). Outflow is concentrated between four large retail groups.

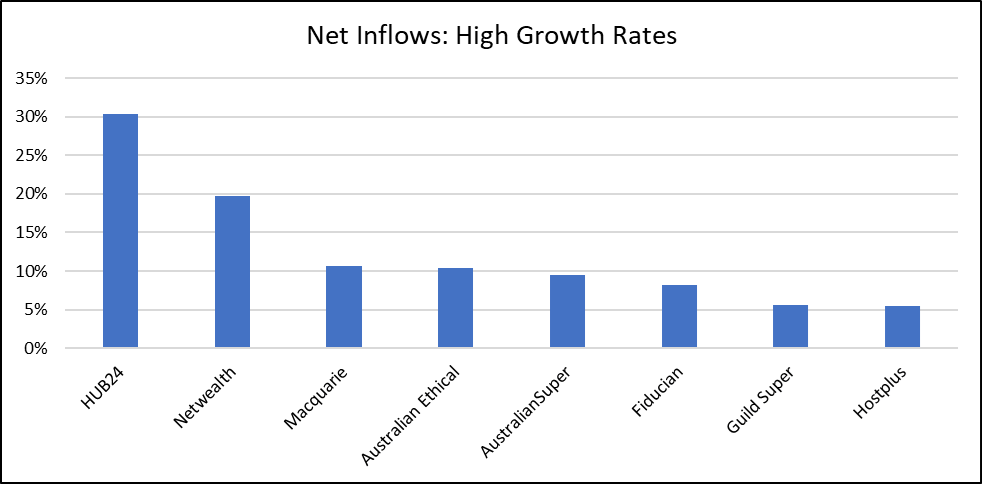

Finally it is important to consider growth rates, calculated through dividing net inflows by AUM. This provides a fascinating snapshot that the fastest growers are participating in a range of unique themes, be it advanced platform offerings for advisers/SMSF’s (HUB24, Netwealth, Macquarie, Fiducian), or a specific cohort (ESG and sustainability – Australian Ethical, females – Guild Super), or long-term brand and performance (AustralianSuper and Hostplus).

Leave a Comment

You must be logged in to post a comment.