No one knows to what extent new education standards will transform the advice industry, but it’s fair to say that transformation is coming.

Institutions are walking away from wealth management – either spinning off or divesting from their advice operations – because they can’t seem to make the economics of it all work anymore. ANZ Bank sold its aligned dealer groups to IOOF, Commonwealth Bank is spinning off its wealth management arm and National Australia Bank is evaluating options for its dealer group brands, which include Godfrey Pembroke, Apogee, Garvan, and Meritum.

The banks appear to be prepared to hold onto the component of their distribution strategies they have the most control over: high-net-worth private advice practices and salaried advisers who want to build a career under a bank brand.

Owning licensees, where compliance and education standards are monitored and adhered to at arm’s length, seems too much for most institutions, following the Hayne royal commission. The wealth management game now seems less about building scale and extending tentacles of distribution and more about mitigating risk and keeping ahead of new standards, which are yet to be set in stone but are certainly rattling in the pipeline.

At least a quarter of the roughly 25,000 individuals who call themselves financial advisers will probably call it quits and leave the industry within the next five years, UBS Equities analyst Kieren Chidgey reckons. These advisers are unlikely to be replaced by new ones entering the industry, Chidgey states in a recent research report on the Australian wealth management industry titled School or Beach?

Compare that with the turnover the advice industry now knows as normal. In the 12 months to the end of April this year, 344 advisers left the industry – a net loss of 1.4 per cent. Close to 11 per cent of advisers exited the industry during that time and the gain from new advisers joining was 9.5 per cent, the UBS research shows. Australia’s adviser exodus will continue to gain momentum and the biggest catalyst most in the industry are pointing to is the new education standards mapped out under the Financial Adviser Standards and Ethics Authority (FASEA) framework.

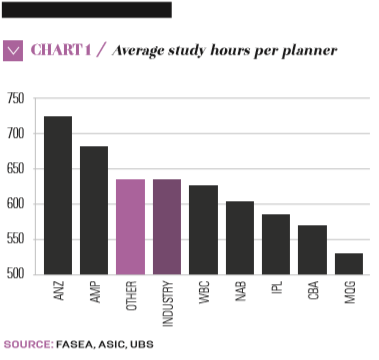

Chidgey has added up all the hours of education existing advisers will need to complete between now and the start of 2024, when the transition to new rules ends, and has determined that the average existing practitioner will need to undertake 642 hours, with 52 per cent of advisers facing 960 hours – the maximum.

“Given an average adviser age of [about] 55 years, we believe at least 25 per cent of advisers could call it quits over the next five years, with risks of greater attrition should grandfathered commissions be abolished,” Chidgey concluded.

ANZ’s aligned dealer groups – which have already been sold to listed wealth manager, IOOF – and AMP’s are composed of the groups of advisers most affected by the new standards, the UBS research shows. CBA and Macquarie Group’s advisers have the least ground to cover among the country’s largest wealth management institutions when it comes to meeting new education standards.

Advice businesses outside of the large financial institutions will also have work to do. UBS estimates the average amount of study those existing advisers will need to meet the new requirements is the same as for those at the major institutions – 642 hours.

“Arguably, this could be a bigger impost for IFAs [independent financial advisers], as major financial institutions shoulder some of the burden,” Chidgey stated.

The UBS analysis shows a stark reality for both owners of advice businesses and advisers themselves, who might be contemplating the opportunity cost of remaining compliant compared with choosing another career or, as may be the case for many, pulling up stumps and entering retirement.

Today, 47 per cent of advisers do not hold a bachelor’s degree, even though the FASEA framework will require a relevant, bachelor-level degree from an approved list after January 2019.

There is some question over whether the term “relevant” will remain in the final framework. Meanwhile, the Financial Planning Association is suggesting a streamlining of accepted degrees in its latest submission, raising the bar even higher than the current FASEA proposals.

In addition to the 47 per cent of advisers who do not hold a bachelor’s degree, another 5 per cent have undergraduate or postgraduate degrees in unrelated disciplines, meaning at least this number will need to undertake financial planning equivalency studies.

Education v experience

Possibly the most interesting finding to come out of the UBS research and the industry submissions to FASEA during the consultation period, which closed at the end of June, was the consideration given to education over experience.

There were a number of submissions that argued the FASEA proposals did not attribute any value to experience, a point policymakers are sure to hear. The Association of Financial Advisers argued in its submission that 10 years of experience as a responsible manager of an Australian Financial Services licence should be worth at least four subjects of a graduate certificate for advisers without a degree who have a diploma of financial planning.

The AFA’s submission went on to argue that financial advisers who are 55 years old at the end of 2023 and have 15 years of experience should be entitled to stay in the industry with just four units of the graduate certificate under their belts.

AFA grew out of the era when life insurance agents were a much larger part of the wealth management industry so its roughly 4500 members are probably at the more experienced end of the spectrum.

The research shows a clear correlation: the longer advisers have been in the industry, the more additional study they will probably require under FASEA’s new standards. UBS estimated that, among advisers with at least 25 years of experience, more than 70 per cent will need to undertake the full 960-hour graduate diploma additional education course.

Advisers who have been around the longest and who want to continue to give advice after 2023 will, therefore, be lobbying FASEA to supplement educational points with hard-earned experience.

But it’s likely the transition to new education standards will make wealth management firms, particularly the institutionally owned ones, rate experience as more of a liability than an asset.

Because the average financial adviser is in their mid-50s, the impost of enhanced educational requirements could lead to accelerated retirements over the next five years.

That’s why analysts in the segment and wealth managers themselves are looking at their advice businesses in terms of their advisers’ experience and the educational requirements and making a call to walk away now.

Leave a Comment

You must be logged in to post a comment.