The growth of independent platform providers Netwealth, Praemium, and Hub24 has accelerated in the last 12 months.

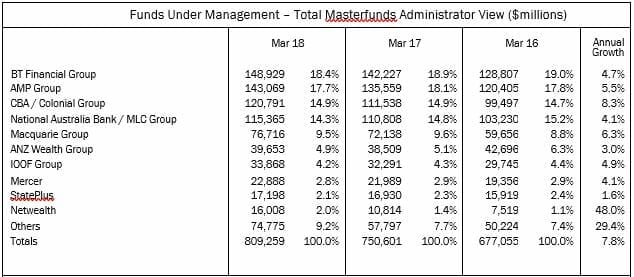

Netwealth, the 10th largest provider of platform solutions, is the leader of the second tier of service providers challenging the large incumbents, posting 48 per cent growth in 2018, new data shows.

CBA posted the best growth rate of the incumbent providers, with 8.3 per cent.

BT Financial Group remains the nation’s largest ‘Masterfund’ provider, researcher Strategic Insight reports. BT has $150 billion in funds under advice across its BT Wrap, Panorama and Asgard platforms.

AMP Group, with North and MyNorth platforms, sits second, with $143 billion under administration, while CBA and NAB hold $121 billion and $115 billion, respectively, across their platforms. Thereafter, the list of platform providers drops off to the second tier.

The $74.8 billion linked to the ‘others’ group, which sits outside the top 10 providers, is primarily attributable to independent managed account platform provider Hub24, which has increased its funds under administration by 58.4 per cent, and Praemium, which increased FUA 39.2 per cent in the 12 months to March, Strategic Insight senior manager Daniel Morris says.

The increasing success of Netwealth, Hub24 and Praemium is largely predicated on their managed account platform offering. The independent players have made a well-documented push into the advised client space in the last few years.

Strategic Insight’s Morris notes that while the growth rates are impressive, it is much easier to record such rates at smaller players than at incumbent institutional providers.

“Obviously, Netwealth are a smaller player with a single platform,” Morris says. “So, in percentage terms, their growth is very impressive, while a lot of the larger groups have older products flowing through their funds.”

He uses the case of AMP to illustrate the point.

“Platform such as AMP’s North are doing quite well, but other products might drag the group’s figures down.”

Still, the results show an industry being infiltrated by a new breed of providers that threaten to break up the institutional side’s 20-year dominance of platform administration services.

The previous year’s numbers confirm that the large players’ growth rates are slowing. Outside of Netwealth and the ‘others’, the average growth rate for the top 10 was 4.7 per cent in 2018, down considerably from 9.1 per cent in 2017.

Professional Planner will provide a full breakdown of the platform dynamic in our August magazine edition.

Leave a Comment

You must be logged in to post a comment.