For those chasing the yield offered by the Financials sector, excluding REITs or property trusts, it’s been a challenging few months. But if you saw some of the challenges coming down the pike for the high-yield segment, as I did, it paid to be a bit more agile in your approach.

The twin spearhead aimed at this sector comprises the increasing appeal of fixed income as bond rates rise on the back of the Federal Reserve rate hikes and the bloodbath that the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry has become. Scalps large and small have been taken. It seems that broking analysts have now downgraded their expectations of earnings for this sector.

As most people who regularly read my columns know, I use the broker earnings and dividends forecasts of the top 200 companies listed on the ASX – collected by Thomson Reuters – to back out rolling 12-month forecasts of capital gains and total returns (including dividends but not franking credits) for each of the main 11 sectors of the ASX 200.

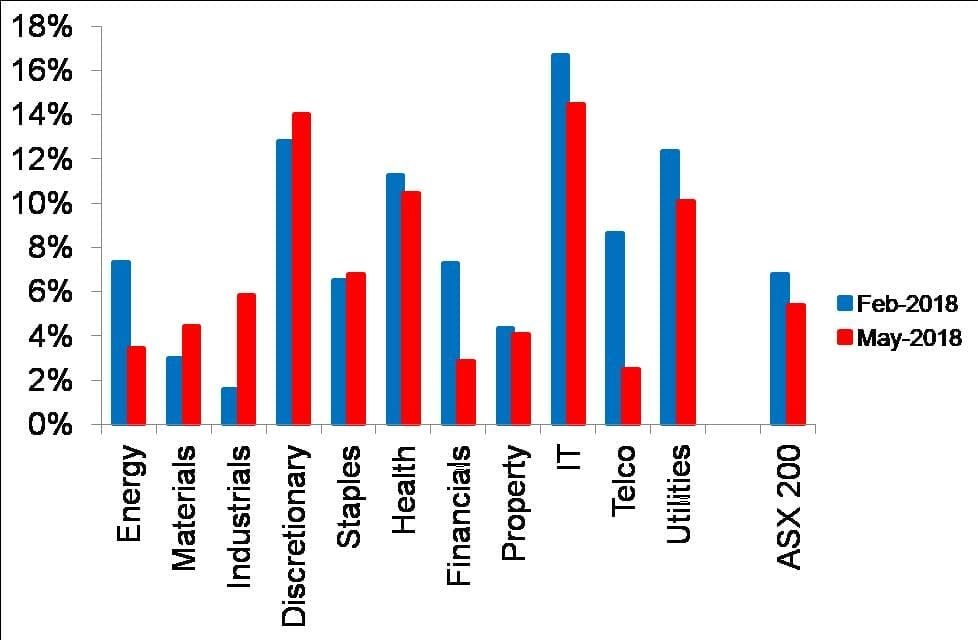

The most recent sector forecasts (from May 25, 2018) of capital gains are shown in Chart 1, alongside the forecasts made three months before, at the end of February. Forecasts for Materials, Industrials and Consumer Discretionary have strengthened over this period. Those for the four high-yield sectors (Financials, Property, Telcos and Utilities) have fallen. Given the relative size of Financials in the ASX 200, the fall from 7.3 per cent to 2.9 per cent in capital gains is material. The ASX 200 forecast slipped from 6.8 per cent to 5.4 per cent in spite of the strengthening of some sectors.

Chart 1: Rolling 12-month forecasts of sector capital gains on the ASX 200

Source: Thomson Reuters Datastream & Woodhall Investment Research

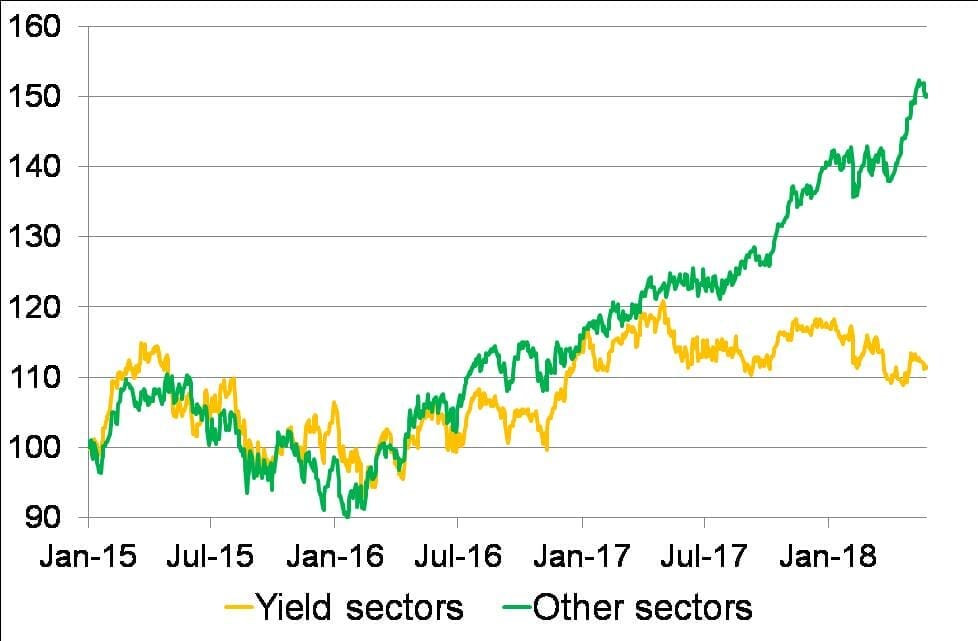

The expected dividend of 7.1 per cent on Financials (which is largely fully franked, taking the grossed-up yield to about 8.5 per cent) still warrants some attention; however, the historical total returns in Chart 2 tell a more sobering story. I constructed daily market capitalisation-weighted accumulation (dividends reinvested) indices for two aggregated sectors. One index, ‘yield sectors’, represents the four high-yield sectors identified above. The ‘other sectors’ index represents the other seven sectors. This chart is consistent with the annual figures I reported for the same aggregated sectors in April.

It can be noted from Chart 2 that the high-yield sectors have largely gone sideways since the beginning of 2017. That means capital losses have completely offset the dividend payments. On the other hand, the ‘other sectors’ have charged ahead. Any fund managers that noted this dichotomy in total returns should have found it easy to outperform the ASX 200 by tilting their allocations away from high yield if their mandates allowed it.

In our own model portfolios, we switched from a 100 per cent allocation to a high-yield model portfolio (tilted strongly, but not exclusively, to those sectors) from inception (February 2014) to a 50/50 blend of high-yield and a straight conviction model portfolio on February 1, 2017. We were less than certain at the time that it was the end of the high-yield play. We dropped the weight of high-yield in the blended portfolio from 50 per cent to 25 per cent on December 1, 2017. We dropped the high-yield portfolio allocation to 0 per cent of the blend from February 1, 2018.

Chart 2: Aggregated sectors’ accumulation indices for the ASX 200

Source: Thomson Reuters Datastream & Woodhall Investment Research

As a result of those changes, my blended portfolio has managed strong outperformance since inception. But the important point here is not whether I achieved these outcomes but what investors should be looking out for.

Most investment styles will have good and bad periods of performance; therefore, investors should expect most funds to take the rough with the smooth or switch his or her allocation as I did. I believe the criticism of active versus passive funds management comes from many funds not having the mandate to tilt their funds as much as is necessary.

And while passive funds might at times beat a given active manager, the passive funds and index exchange-traded funds will probably underperform cash more than an agile manager!

Dr Ron Bewley is a principal of Woodhall Investment Research and is a regular columnist for Professional Planner.

Leave a Comment

You must be logged in to post a comment.