Several prominent investors and commentators have been warning that there are dark clouds on the horizon this year. There always are. It is worth remembering, however, that booms and bubbles tend to bust when every remaining bear has been converted and everyone is bullish, not when there is a large band of Cassandras warning of imminent doom.

For that reason, it could be 2019 before we see the impact of the excess – itself the result of unusually cheap money for an unusually long time.

As for 2018, here are four themes that should influence investments in the year ahead.

China

According to Angus Grigg, from the Australian Financial Review, China’s ruling party is anxious. At the core of this unease, Grigg states, is the transition from an economy supported by investment in fixed assets to one built on consumption. “Forty-one per cent of all China’s economic activity in 2017 was generated by building things, known as fixed-asset investment,” he wrote.

This number must come down below 30 per cent, but consumption won’t immediately replace the lost growth. In other words, Beijing needs to decide: continue to build, which would keep the economy humming at 6 per cent GDP growth, “or pull back and begin a long period of slower growth as the economy restructures”.

“The party flirted with the latter in 2014 and 2015, but ultimately did not want to see what an economy growing below 5 per cent might look like and so pushed the button on yet more stimulus,” Grigg wrote.

That stimulus is what drove mining and materials stocks in 2016.

“For economists like Jonathan Anderson, previously with the World Bank in Beijing and now an independent adviser, the 2016 credit stimulus, which soaked up much of the industrial over-capacity, was the final straw,” Grigg’s article states. “He went from China optimist to fully fledged bear as Beijing pumped credit into the system faster than during the 2008 global financial crisis.

In forecasting a fall in growth to between 2 per cent and 3 per cent, Anderson had said: “At the current pace, we would highlight 2019-20 as crunch years when China crosses the potential crisis threshold.”

Perhaps that is why Wesfarmers sold the Curragh metallurgical coal mine.

Junk bonds

Moody’s reports that a record $947 billion of US high-yield, or ‘junk’, debt, is scheduled to mature in the next four years. Clearly some issuers may struggle to refinance, especially if the appetite of lenders wanes.

And with record low spreads between junk yields and Treasuries, that could be a real possibility.

Of the $947 billion total, $400 billion is set to mature in 2020. This represents the highest amount of rated debt to mature in a single year in the history of credit markets, Moody’s reports. The telecommunications, technology and media sector carries the biggest debt burden.

Tech boom 2.0

Speaking of tech, in my 2010 book Value.able, I recalled a company that listed in the US in 1999, whose shares rocketed from 50 cents to more than $8.80, despite its prospectus stating that it “conducts no substantial business activity of any description, and has no plans of conducting any business activity of any description”.

Nothing so preposterous should occur, yet it happened again in 2017.

In December, shares in a New York-based company, Long Island Iced Tea, rose as much as 289 per cent after the unprofitable business rebranded itself Long Blockchain.

“It’s the latest in a near-daily phenomenon sweeping the stock market, [in which] obscure microcap companies reorient to focus on some aspect of the mania sparked by bitcoin’s almost 1500 percent rally this year,” Bloomberg states.

Long Blockchain, states that it will “now seek to partner with or invest in companies that develop the decentralised ledgers known as blockchain, the technology that underpins bitcoin”.

Sounds a lot like, ‘no substantial business activity of any description’.

The inexorable rise in the share prices of tech companies has resulted in, for example, the combined market value of Tesla, Uber and Twitter rising to US$140 billion ($176 billion), despite a combined profit for the three companies of zero.

And keep in mind the European court determined in late December that Uber is not a tech company but a taxi firm. This will have serious implications for gig-economy players such as Airbnb, which enjoy astronomical market valuations.

Think of the decision as a nail in the coffin for the tech boom. If a tech company’s profits are limited to the economics of a transport company, the valuations cannot be as high and private equity funders will not remain as enthusiastic. The decision could result in a deflation of the bubble.

And there is no question that a bubble exists.

An increasingly concentrated bet on technology is demonstrated by the fact that fully a third of the S&P 500’s year-to-date gains are attributed to just five tech companies – Apple, Microsoft, Google parent Alphabet, Facebook and Amazon. Furthermore, almost half of all the companies listed in The Nasdaq 100 Index (45 companies) are trading on a forward price-earnings ratio of more than 200 times, including Tableau, Wix, Amazon, Yelp and Shopify.

Lest you think Australia is immune, keep in mind companies listed on the ASX such as Updater and GetSwift are trading on market capitalisations of $600 million to $750 million with little or no revenue. During 2017, GetSwift generated revenues of just $336,356, up on the previous year’s $107,554.

Earlier this year, lauded value investor Howard Marks perhaps best articulated the love affair with everything technology-related when he described investors’ amore thus: “Old-timers fare worst in a boom, with the gains going disproportionately to those who are untrammelled by knowledge of the past and thus able to buy into an entirely new future.”

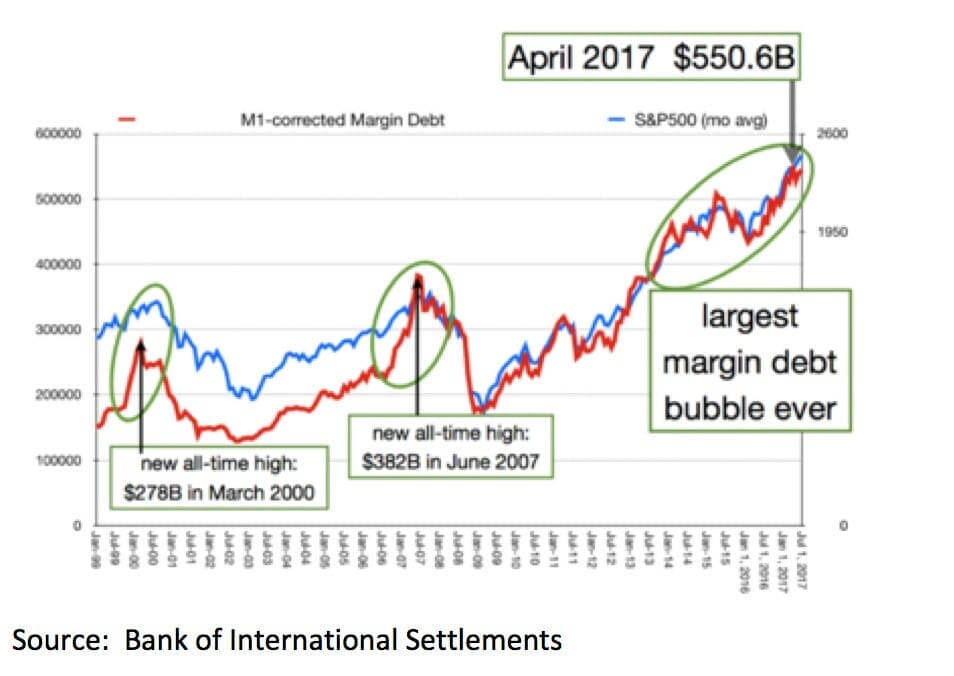

There is little question that the themes of disruption, creative destruction, and particularly automation, have captured the imagination of investors, who have also now borrowed record amounts to buy stocks through margin loans (Fig.1)

Figure 1. Margin loans taken out on US stocks now exceed tech 2000 and pre-GFC booms.

Our concern is that valuations for disruptors factor in a future that will not be disrupted (the European decision against Uber shows the folly in this).

To suggest that the growth of these companies’ earnings will continue unchallenged by competition, economic setback or legislative response is to believe in a future when history demonstrates it is unlikely.

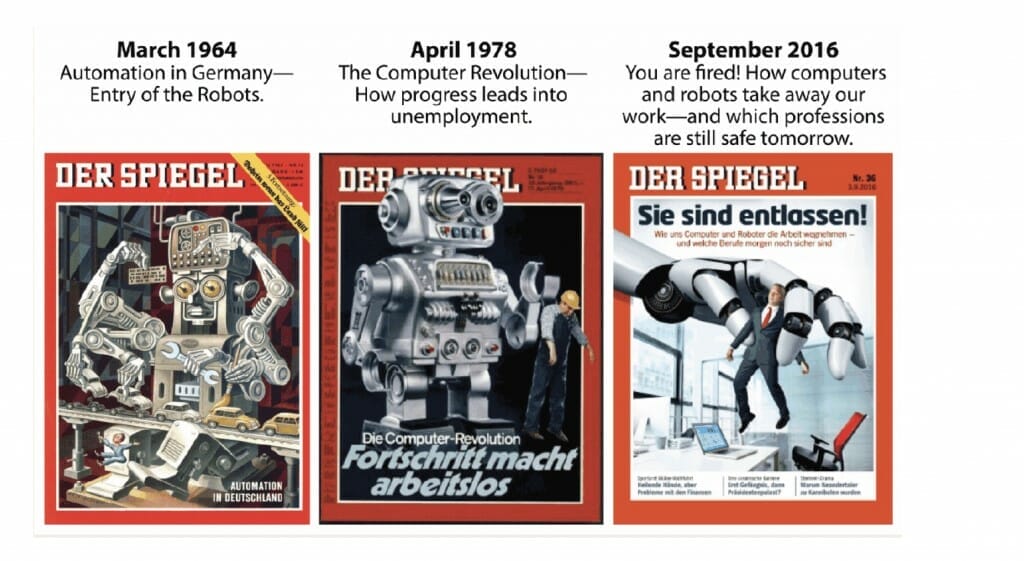

Have a look at the various issues of German news magazine Der Spiegel in Fig.2. It becomes immediately obvious that the current emotion about automation is not new, reinforcing our observation that ‘disruption’ is just a fancy new word for change, which is constant.

Figure 2. Der Spiegel covers 1964-2016

We have seen this elsewhere, too. In Omaha, Nebraska, in the US, farm land prices soared amid thematic enthusiasm for the westernisation of Asian taste buds and the replacement of rice with red meat and wheat. But that enthusiasm had already emerged, in the 1960s, and farm prices subsequently plunged.

Enthusiasm abounds. When the chief executive of American Airlines, Doug Parker, announced on an earnings call with analysts, “I don’t think we’re ever going to lose money again”, I wondered whether bullish enthusiasm had crossed over into irrational exuberance.

When WeWork chief executive Adam Neumann told Forbes.com in October, “No one is investing in a co-working company worth $20 billion. That doesn’t exist…Our valuation and size today are much more based on our energy and spirituality than on a multiple of revenue,” I couldn’t help but think, here we go again.

With commentators calling “loss the new black”, citing the market capitalisations of Uber, Snapchat, WeWork and Amazon as evidence of a “new world order”, and as articles with titles such as “Buy Everything”, “RIP Bears” and “Congratulations Capitalism” become increasingly common, it’s worth asking whether sound reasoning has been usurped by unbridled optimism.

Investors have surprisingly short memories and there is no doubt that the fear of missing out – as reflected in the pursuit of companies with zero profit such as Tesla – is replacing the fear of loss. When that happens, be cautious.

Recently, in American Consequences, Dan Ferris wrote, “Investors have pushed [that] reality aside and fallen in love with companies that have a great story and a soaring share price…regardless of profitability. What they don’t realize is that equity only has value if a company earns a profit. That means there’s a much higher probability than investors currently acknowledge that unprofitable highfliers might be worth…zero.”

Construction

In Australia, potential declines in construction activity will be the indicator to watch in 2018. The construction industry is the third-largest employer, after retailing and healthcare, so any weakness in employment levels there could have serious consequences for the rest of the economy.

Record levels of residential building commencements have generated about 180,000-200,000 construction Jobs since 2011. One estimate has 2018 losing about 80,000 jobs as the sharp decline in applications and approvals leads to declining commencements.

While some suggest the boom in government-backed infrastructure construction could soak up the job losses, others believe there will be a meaningful net attrition.

With house prices already falling, auction clearance rates slowing and time on market for homes increasing, the additional supply of apartments emerging from the construction boom over the last couple of years is expected drive prices down further.

The impact on the sentiment of consumers, many of whom are heavily indebted (the household debt-to-income ratio is a staggering 194 per cent) is difficult to over-state.

There are indeed dark clouds forming. But there are also still too many bears. A year of volatility may therefore be in store for 2018. Investors should seek advice about whether selling into strength and adding to investments only upon weakness are wise strategies.

Montgomery Global Funds own shares in Apple, Microsoft, Facebook and Amazon.

Leave a Comment

You must be logged in to post a comment.