What’s in a name? Not that much if it’s a balanced fund, it turns out.

Balanced funds make asset allocations predominantly based on actual dollar allocations, or capital, rather than on the underlying risk inherent in those assets. But they’re not balanced at all, given equities dominate these portfolios, both pushing it up and dragging it down with the whims of the market.

Risk-parity funds incorporate a portfolio management approach that focuses on the allocation of risk rather than capital, and so lower volatility bonds often play a larger role. But do they double-down on inflation risk by leveraging into long-duration bonds now that bond yields are at historic lows? What happens if we get an inflation scare such as in 1994?

This is the main criticism levelled at the risk-parity sector, which holds an estimated US$150 billion in assets. A closer look at the facts suggests this is an over-simplification.

Two of the basic premises of risk-parity funds are that the long-term reward for risk taken should be the same across all asset classes and that volatility (or risk) isn’t the same across all asset classes.

Historically, this means bonds have dominated some risk-parity portfolios in the same way that equities have dominated balanced funds. Leverage has been used to bring the absolute risk contribution from bonds up to be equal to that of equities – giving a more balanced risk outcome.

But since the election of big-spending, tax-cutting US President Trump late last year, inflation is back on the agenda. The assumption is that if inflation takes off, leveraged long-duration bonds – and risk-parity funds – will take a huge hit.

After decades of falling inflation, the threat of reflation may be the risk to which investors are most attuned.

Investors in risk-parity funds should certainly be asking how the risk of inflation is being managed, but assuming that some of the world’s largest risk parity investors are ignoring it is unfair. Given that two of the largest managers in the world are the quantitative heavyweights Bridgewater and AQR, assuming that they are blindly unaware of the risks of being highly leveraged into low-yielding bonds in an inflation driven sell-off seems unrealistic.

Of course, fund managers are not limited to investing in equities and bonds. They can increase their allocation to a wide range of other asset classes – such as commodities or currency – or take advantage of some arbitrage opportunities, depending on their view of current risk.

Why risk should be the focus for all managers

If investors knew future risk levels, investment returns and asset-class correlations, they could build a perfect portfolio. But only one of these components can be known with any degree of confidence: risk. It can be forecast relatively well, while forecasting long-term returns is more challenging and the likelihood of predicting asset-class correlations with any accuracy comes a distant last.

This is why all managers should be using some form of volatility forecasting.

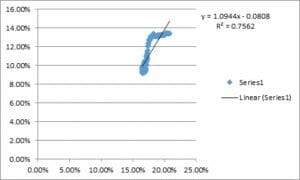

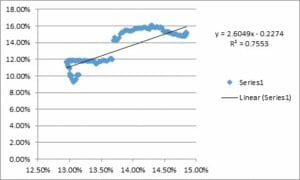

The evidence strongly suggests that historical volatility is a robust indicator of future long-term volatility (over 10 years). The following two diagrams show this in practice, demonstrating how historical Australian equity and US equity market volatility can be used to forecast future volatility.

Our model explains 75 per cent of the variability (as shown in the R-squared figure) between the linear forecast (black line) and realised annualised price movements over 10 years.

Australian Equity Market Volatility: Forecast v. Actual

Source: Bloomberg and Innova Asset Management. Indices used are price indices from 1960.

US Equity Market Volatility: Forecast v. Actual

Source: Bloomberg and Innova Asset Management. Indices used are price indices from 1960.

Volatility forecasting is one of the tools that allows us to manage risk effectively. Innova may not be a risk parity manager but we incorporate a “maximum risk contribution” measure, which defines the maximum volatility level that each asset class can contribute to the total portfolio.

Innova doesn’t have any allocation to long-duration sovereign bonds because of the risk if there’s any upside surprise to inflation. If Innova is able to model the ‘left-tail’ risk in sovereign bonds, and can build volatility forecasting models that explain 75 per cent of realised results, we would hope that other quantitative managers could do the same. Admittedly, we have partnered with one of the world’s largest risk-management firms, the Milliman Group, so we have a distinct advantage over most. However, it would be naïve indeed to assume no one else is aware of these risks and implementing strategies to mitigate them.

Risk comes in many forms and, unfortunately, it is often invisible until it’s too late. Chasing returns isn’t a smart strategy at the best of times and is an even worse idea in the current climate, even though market returns continue to be solid and volatility has been extraordinarily low, given high valuations and rising geopolitical risk. There is the heightened risk of the rise of naïve risk-parity solutions cropping up in-house, where money managers who don’t have the necessary risk-management techniques blindly apply leverage to low-volatility assets to make their overall portfolio volatility contributions equal. This approach could be disastrous.

Investors need to keep a sharp eye on volatility, the likelihood of losing money, and the average and maximum magnitude of potential losses, given that returns build a portfolio but unmanaged risk will almost certainly derail it.

Leave a Comment

You must be logged in to post a comment.