Behavioural economics has exposed the hidden logic driving people’s decisions about money but it often takes a good financial planner to help clients make the ‘irrational’ rational.

The problem has nothing to do with how smart we are and everything to do with the way our brains work.

We now know (thanks to the work of psychologists Daniel Kahneman and Amos Tversky) that people attach values to gains and losses rather than to wealth, and the ‘decision weights’ they assign to potential outcomes differ from the probability of those outcomes occurring.

For example, a rational person would place a 2 per cent decision weight on a gamble with a 2 per cent chance of occurring. However, in reality, most people overweight the possibility and apply a decision weight of 8.1 per cent.

Similarly, a rational person would place a 98 per cent decision weight on a near-certain gamble with a 98 per cent chance of occurring. But the majority of real people underweight the possibility and apply a decision weight of about 87.1 per cent.

This imbalance means people become disproportionately excited or fearful about improbable or likely events occurring – and make poor decisions as a result. This is the possibility and certainty effect in action.

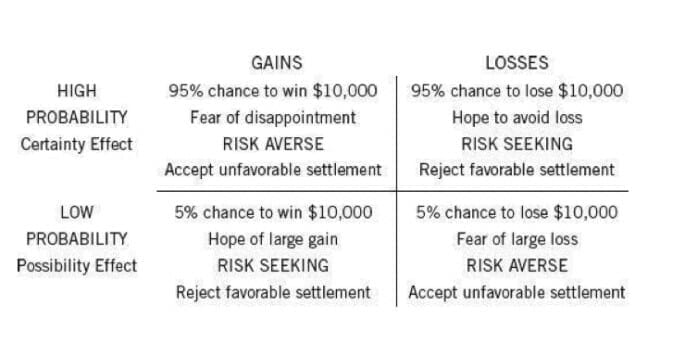

Unpacking the fourfold pattern

The fourfold pattern groups common decisions into quadrants based on their perceived likelihood and outcome, as shown here:

The top-left corner shows that people are risk averse when there is a high probability of achieving a substantial gain. They’ll often accept less to make a sure thing absolutely certain.

On the other hand, the top-right cell shows that people can become highly risk seeking when faced with the prospect of large losses. Why? People experience a diminishing sensitivity to near-certain events and so the sure loss has a bigger emotional impact than the possibility of an even larger loss. The result: we throw even more money into a failed investment hoping it will come good.

The bottom-left corner shows the possibility effect and explains why people are so willing to gamble on low-probability events with big payoffs, such as lotteries.

The bottom-right cell shows that people are willing to pay more to avoid the improbable chance of a large loss. This is one reason insurance is a profitable business.

The challenge of identifying and changing behaviour

Before behaviour can be changed, it must be identified, and that’s not easy given many clients are often oblivious to their own destructive tendencies. These behavioural biases occur at an emotional level but even highly self-aware clients are unlikely to reveal their worst traits immediately.

Planners need independent data about their clients’ behaviour to identify the individual traps each client regularly falls into.

Digital tools and applications are an important tool to strengthen consumers’ ability to manage their personal finances, according to an international report from the OECD International Network on Financial Education.

“Digital tools can complement and leverage traditional financial education approaches and mechanisms,” the report states. “They may be particularly useful to provide vulnerable and hard-to-reach groups with actionable and digestible guidance to help them navigate ever more complex digital finance products and tough financial times.”

Behavioural economics has taught us that all clients and investors – not just those who are vulnerable – are susceptible to self-sabotaging behavioural biases.

For example, poor market timing decisions cost US mutual fund investors an annualised 37 basis points over the 10-year period ending 2016, Morningstar reports. No one sets out to ‘buy high and sell low’ yet, under pressure, this is exactly what many investors do. Chasing returns is one of the most avoidable, but common, responses people are susceptible to when emotion overrides reason.

Understanding and curbing these types of behavioural biases is one of the most important goals for any financial planner interested in creating a platform for clients to achieve their personal goals.

Over the long term, clients can also self-monitor their behaviour using technology and independent financial information as a reliable checkpoint. Half-yearly (or potentially more frequent) check-ins with their adviser can provide a tune-up and boost motivation.

We can turn the predictably irrational into the rational with insights that reveal how our individual behaviour follows patterns that are more common than we might expect.

Leave a Comment

You must be logged in to post a comment.