MLC’s Gareth Abley argues that advisers must ensure clients take an objective and long-term perspective to share markets and manage the emotional flux caused by volatility and an excitable mainstream media.

Investors are at an interesting inflection point with regard to shares. While many are still pained by the losses of 2008, they’re also aware that term deposit rates are shrinking, bond yields are low, and shares can still deliver strong returns.

So it’s a good time to take a step back and reconsider the nature of share investing and the role shares should play in an investor’s portfolio.

This article offers no predictions. Instead, I examine the last 112 years of share market returns through the lenses of three different time periods. This can give investors an objective and long-term perspective to manage the emotional flux caused by capricious markets and excitable media.

Lens 1 – the very long run

Historically, investors have generally done well investing in shares over long periods. There are logical reasons why we can expect this to continue. Essentially, it’s a bet on 7 billion people waking up each day and finding ways to be more productive, and then finding new ways to spend their money.

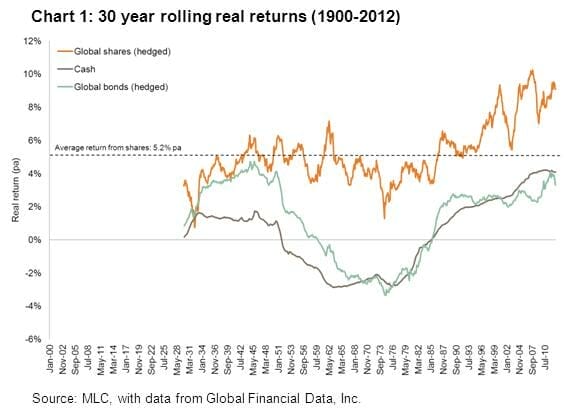

Chart 1 shows rolling 30 year real returns (above inflation) from global shares, bonds and cash since 1900. These returns have been generated through wars, pestilence, financial crises, bubbles and busts.

Over every 30-year period, investors have been rewarded with a positive real return from shares. For example, their spending power has grown faster than inflation. Shares have also consistently returned more than the other mainstream assets – bonds and cash – which have both failed to keep up with inflation for prolonged periods.

It’s also worth noting that while the average outcome has been very good, investors have had very different experiences even over 30 year periods (ranging from less than 1 per cent pa to just over 10 per cent pa).

Lens 2 – the short run

The reality is investors often react to short-term market volatility, of the type shown in Chart 2, because of the emotional and financial pain it causes.

This emotional pain matters in determining an allocation to shares, because it creates “switching risk” – the risk that investors react to short-term performance in ways that are wealth-destroying. We sell after shares have fallen, when the pain becomes too great, and we buy after shares have gone up, once the fear of missing out on profits exceeds the fear of losing money.

A key benefit to retail investors of financial advice, and of investing in a diversified portfolio of shares and other assets, is to avoid this type of self-harm.

The other reason short-term volatility can really matter is “sequencing risk”. This is the risk that the year of big negative returns happens when an investor’s superannuation pot is at its largest, close to retirement.

Both switching risk and sequencing risk suggest investors and their advisers need to factor in the reality of short-term volatility when determining an allocation to shares.

Lens 3 – 10 years

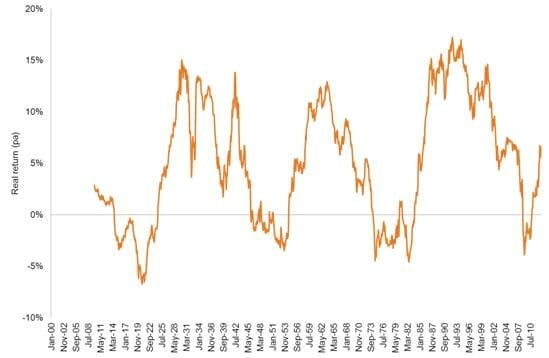

Ten years is arguably a more realistic ‘long-term period’ for investors and advisers to focus on than 30 years. Chart 3 shows real returns for global shares over rolling 10-year periods.

The chart shows that, more often than not, shares have generated very attractive returns over 10 year periods. Indeed, 26 per cent of 10-year periods saw real returns of more than 10 per cent pa.

But perhaps surprisingly, it also illustrates that in over 27 per cent of 10-year periods, shares delivered negative real returns.

What conclusions can we draw?

1. It makes sense for most long-term investors to have a meaningful allocation to shares

• Very likely to have a higher long-term real return than bonds and cash.

• Likely to outpace inflation and support future spending.

2. Share performance can be very volatile and painful to investors in the short term

• Can cause clients to switch at the wrong time.

• Fear of volatility may also lead investors to invest in more conservative asset classes over the long term, missing out on the potential for higher returns.

• If a bad year coincides with retirement, it is a big deal.

3. Shares can also deliver negative real returns over 10 year periods

• Investors shouldn’t have all their money in shares.

Gareth Abley is head of alternative strategies at MLC Investment Management

Leave a Comment

You must be logged in to post a comment.