Historical perspective is one thing but how should clients feel about the market’s recent rise? Van Eyk’s Jonathan Ramsay believes being happy, worried or just a little depressed are all perfectly valid responses.

Financial planners are lectured often enough that: “past performance is not indicative of future performance”. Yet it still seems to be a truism that clients are more adventurous when share markets have just risen and this would seem to be the case now, notwithstanding very recent market setbacks.

Your clients are bombarded with information from the media about past performance, usually about investments that have just done very well or very badly, with the suggestion that the recent trend will continue. In this situation the path of least resistance is always going to be to pander to client fears when markets are down and creep out on the risk spectrum when things seem more settled.

Yet both behavioral and valuation theories of investing suggest that this is counter to best practice and will lead to underperformance much of the time. Of course, when markets trend, chasing past performance can work. The problem is that it doesn’t work at the extremes when the investor’s degree of confidence and valuations give opposite signals and the potential downside is greatest.

Getting clients to focus on the finer points of valuation or finance theory in an hour-long interview with their adviser may be challenging. So here’s a chart that might be useful in certain situations to shift their focus, particularly when you are required to ask clients to adopt a contrarian stance.

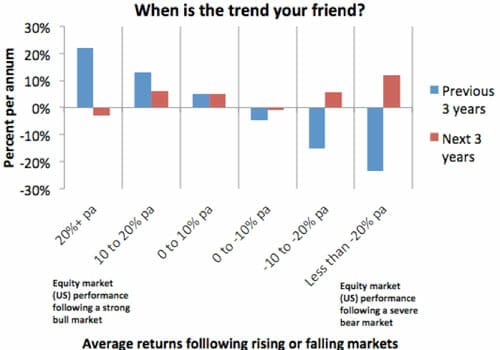

Consider the following analysis of returns over the last 80 years (US data is used as it gives us more data to look at). It shows average annualised equity market returns for 3-year periods after markets have risen or fallen by different amounts in the preceding 3 years.

We can see clearly that after periods when markets have risen strongly they have then tended to disappoint and when they have fallen they have often tended to rebound particularly strongly.

This is mostly due to the gravitational effect of valuations, which become stretched at peaks and improve when fear is in the air. However, this also hides long periods when market behavior can be very different and when contrarian strategies can prove costly.

So at what point are we now? The local share market was up by almost 25 per cent for the year to May 31 2013 and perhaps advisers should reflect on whether they are feeling more bullish for reasons any more fundamental than the fact that markets have risen and clients are giving them less grief. If there is no other reason then maybe that is a cue to go against the grain and start urging a degree of caution to clients.

This is especially pertinent in Australia where market rises were exclusively driven by improved sentiment (earnings actually fell over the period). If you are more bullish now than six or twelve months ago then by definition you must not only have a strong conviction that growth prospects have improved dramatically but have improved to a much greater extent than the broader market believes.

On the other hand, we have not seen the three years of 20 per cent + per annum price rises that have typically preceded a bursting share market bubble. Rather the 7-8 per cent per annum advance of the last three years probably sets us up for something more muted in the next three years.

Jonathan Ramsay is head of asset consulting and strategic research at van Eyk