Future financial advisers will only need to complete four core financial advice subjects and four “financial concept” subjects as part of a Bachelor’s degree or higher qualifications to fulfil the education standard as the government commences the long-awaited consultation on the reform.

Announced on Tuesday morning, Minister for Financial Services Daniel Mulino said the reforms will complement the consultation on managed investment scheme reform released last month and broader work on consumer protection in the superannuation sector which will begin soon.

“When consumers aren’t able to access quality, trusted financial advice, they are more susceptible to predatory forms of lead generation and high‑pressure sales tactics,” Mulino said in a media statement.

The proposed education standard changes will require prospective advisers to hold a bachelor’s degree or higher, as well as meeting minimum study requirements in relevant areas such as finance, economics or accounting, along with completing the four mandatory financial advice subjects.

Ministerial approval will be required for the accreditation of the financial advice subjects, and the minister may have the power to delegate this role to Treasury.

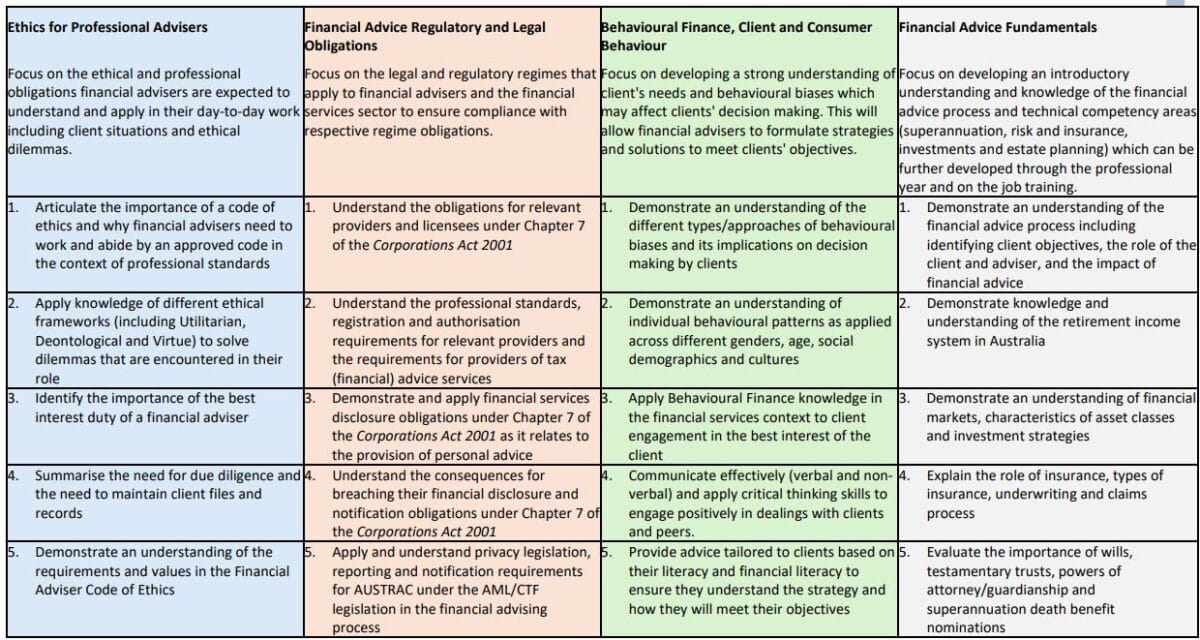

The four proposed prescribed financial subjects will be ethics for professional advisers, financial advice regulatory and legal obligations, behavioural finance and client relationships, and financial advice fundamentals.

Ethics for professional advisers will focus on the financial adviser code of ethics, as well as how to fulfil Best interest Duty and record keeping obligations.

Financial advice regulatory and legal obligations will be centred around disclosure obligations such as Financial Services Guides and Statements of Advice.

Behavioural finance and client relationships would cover streamlined learning outcomes related to behavioural biases, behavioural finance and communication skills.

Financial advice fundamentals is a new subject that will focus on developing a baseline level of knowledge of the financial advice process and existing technical competency in areas such as superannuation, investments and insurance.

Part of the education pathway

The degree changes will still work in conjunction with the professional year, financial adviser exam and continuing professional development requirements to support a substantive barrier to entry for the profession and ongoing training requirements.

The consultation document said licensees will continue to have “flexibility” to determine any level of additional training required for their advisers to ensure they have the demonstrated competency to provide advice, particularly for specialist areas like tax (financial) advice which would require the completion of a taxation and commercial law courses.

The reform was announced last year at the Professional Planner Advice Policy Summit by former Minister for Financial Services Stephen Jones due to continually diminishing adviser numbers in the aftermath of the Hayne royal commission and introduction of professional standards.

Welcomed reform

The reforms had been heavily advocated by the Joint Associations Working Group, which includes the Financial Advice Association Australia, Financial Services Council, Stockbrokers and Investment Advisers Association and SMSF Association.

WT Financial Group managing director Keith Cullen, who had long campaigned for reforms to the education standard, said the old relevant degree was unnecessarily restrictive and was limiting the pipeline of capable new advisers.

“These reforms are enormously important for the future of the advice profession and, more importantly, for Australian consumers who need access to quality financial advice,” Cullen said.

“Opening sensible education pathways, while maintaining strong professional standards, is exactly what both consumers and the profession need. With greater confidence to invest in growing the profession, and alongside technological advancements that are increasing adviser capacity, these reforms will help expand access to advice and begin to rebalance the supply and demand equation to the clear benefit of Australian consumers.”

Cullen said that without fixing the adviser pipeline every other reform is “largely window dressing”.

“Opening sensible education pathways is the single most important reform for advice accessibility,” Cullen said.

“These reforms finally allow the profession to rebuild adviser numbers and expand access to advice.”

FAAA chief executive Sarah Abood said the association is reviewing the proposal to ensure it achieves the goal of offering more flexible degree pathways for new entrants, while maintaining high standards for financial advice education.

“Importantly, existing courses will continue to be relevant, and current students can be confident that these degrees will qualify them to enter the profession in the future,” Abood said.

FSC chief executive Blake Briggs said reforming the education framework is an important step toward addressing the sharp decline in adviser numbers and improving access to trusted financial advice.

“Current education standards are unnecessarily restrictive, creating barriers for both aspiring advisers and existing professionals trying to meet the requirements,” Briggs said.

SMSF Association CEO Peter Burgess said new entrants and universities offering financial planning courses are declining and it was essential to fix the “one-size-fits-all” pathway.

“However, while greater flexibility is welcome, it will be important to mitigate the risk of variation in the quality of qualifications and licensee requirements,” Burgess said.

SIAA chief executive Maria Lykouras said it is critical that candidates with highly suitable degrees in finance, commerce, business and economics from Australia’s top universities have their degrees recognised.

“It is also vitally important that different financial concepts covered by a broad range of subjects from different disciplines such as economics, accounting, investments, finance and commercial law are recognised and counted towards the education requirement,” Lykouras said.

Proposed curriculum for new advice subjects

Source: Treasury. Click to enlarge.

Source: Treasury. Click to enlarge.

Once again, there is deafening silence on the REAL ISSUE and the REAL SOLUTION to the Life / Disability disaster that was brought on by inept representation for the Life Insurance sector by ALL BODIES, which based on the upcoming “solution,” is NO SOLUTION.

I am continually amazed at how no-one in Authority can see the complete stuff up from day one over a decade ago, which still continues today.

Let us quickly look at how all the “improvements” have panned out.

As of today, there has been over 12 thousand Advisers exited the Industry, many of whom wrote Life Insurance New Business and to my limited knowledge, NOT ONE new, “risk only” Adviser has entered the Industry due to the complete insanity of an Education pathway that throws up barriers to entry, by incorporating Education modules that 90% of, have zero to do with the work a risk only Adviser will perform.

It is all well for highly paid people in Government, Education lobbyists, Industry representatives and an army of Lawyers / Compliance entities to bring to life unworkable Regulations that has been proven to be a total blocker for potential new Risk Advisers and with NIL new people coming into the Life Insurance sector via the University pathway and virtually nil true New Business being written, at what point will Australia wake up?