The government will consider levying other subsectors to fund the excess Compensation Scheme of Last Resort remediation, despite pushback from the broader finance sector in a previous consultation last year.

The government announced on Friday afternoon it was seeking industry feedback on options to fund the CSLR special levy, just days after Minister for Financial Services Daniel Mulino hinted a broader funding model might be needed.

The CSLR announced last month that the advice sector would require a $67.3 million levy for FY26, which is above the $20 million subsector cap and triggered the need for the special levy.

The minister outlined four options: taking no action, spreading compensation over time, a special levy for the primary subsector (financial advice in this case), or spreading it out across different subsectors.

The latter option will be the most controversial. Feedback during an inquiry into the failed Dixon Advisory scheme last year saw pushback against expanding funding of excess CSLR costs to other subsectors from the Insurance Council of Australia (representing general insurers), Mortgage & Finance Association of Australia and the Australian Banking Association.

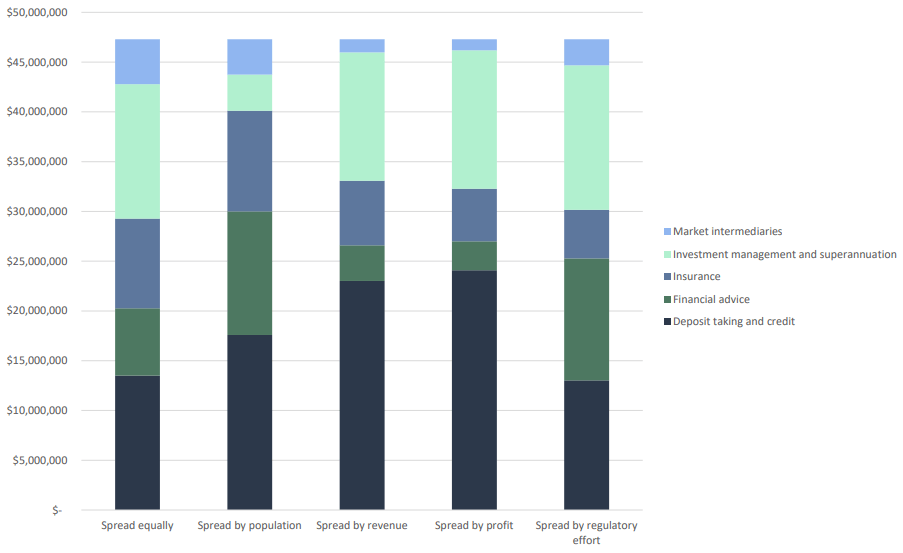

The consultation paper listed 21 potential retail-facing subsectors used in the ASIC Industry Funding Model and set out five sub-options: spreading the levy equally, by “population”, by revenue, by profit or by “regulatory effort”.

While not an option for the FY26 levy excess, the consultation paper does leave the door open to canvassing views on something similar to the pre-CSLR levy, which could also be made available in future levy periods, subject to legislative amendment.

The previous pre-CSLR levy saw the ten largest financial institutions pay $241 million, but that was a once-off which can’t be replicated under the current law.

The table below shows the various levies for each advice subsector. “Licensees that provide personal advice to retail clients on relevant financial products” covers advisers registered for advice on financial products such as super, investments, life insurance; “licensees that provide personal advice to retail clients on products that are not relevant financial products” covers general insurance, simple banking needs and credit.

Estimated graduated levy component for advice subsectors

| Spread equally | Spread by population | Spread by revenue | Spread by profits | Spread by regulatory effort | |

| Licensees that provide personal advice to retail clients on relevant financial products | $130 per adviser | $497 per adviser | $42 per adviser | $43 per adviser | $738 per adviser |

| Licensees that provide personal advice to retail clients on products that are not relevant financial products | $3,981 for an entity licensed for the full year | $2,897 for an entity licensed for the full year

|

$2,428 for an entity licensed for the full year | $1,196 for an entity licensed for the full year | -$60 for an entity licensed for the full year

|

| Licensees that provide general advice only | $2,268 flat levy

|

$2,928 flat levy | $1,290 flat levy | $1,295 flat levy | $721 flat levy |

| Source: Treasury consultation paper. | |||||

The paper notes spreading funding equally would be the simplest option and the 21 subsectors would pay $2.25 million each to cover the $47.25 million excess due in FY26. However, the paper notes this wouldn’t reflect the subsector’s capacity to pay and could introduce a significant risk of under-collection.

Allocating the levy by population would weight payment according to the number of entities within each subsector that are required to be AFCA members.

This method would mean subsectors with smaller populations of AFCA members would face lower levies, but the paper notes that a graduate levy component would operate to impose more levy on larger entities within subsectors and doesn’t reflect the financial position of each subsector.

Distribution of special levy spreading options by ASIC IFM sector

The key flaw with the first two options isn’t that they don’t factor in the financial sustainability of the subsectors, which is why spreading the levy by revenue or profit are other options.

The Australian Taxation Office provided estimated average revenues and profits for almost all entities within each of the retail facing subsectors, which Treasury has scaled this up by the number of entities in each subsector that are required to be AFCA members as of the end of FY24.

The consultation noted this option would be more reflective of the subsectors capacity to pay.

“Revenue and profitability go much more directly to the statutory considerations of financial sustainability,” the paper said.

“Revenue is, generally, a more objective criterion, less susceptible to variation on the basis of accounting treatment decisions than profits. Profits are, conceptually, more reflective of capacity to pay.”

The paper said the advantage of spreading funding by profits, rather than revenue, would be avoiding burdening high revenue, but low-margin businesses.

However, it also notes that using profit data based on a single year isn’t necessarily reflective of a business’s capacity to pay.

The final option would be to apportion the special levy on the basis on “regulatory effort” applied to each subsector as reflected in ASIC’s most recent IFM levy.

“This does not assign blame to any sub-sector for contributing to the specific losses that will be covered by a special levy, but it is in harmony with the principles underpinning the CSLR’s annual levy process where costs are apportioned according to the sub-sector driving those costs,” the paper said.

“If a special levy were applied broadly across retail-facing sub-sectors to reflect the broader benefit and impact of the CSLR on retail clients, apportioning based on regulatory effort may be an analogous approach.”

However, it noted this method doesn’t reflect a sub-sector’s capacity to pay, but that the financial sustainability could still be assessed on a subsector-by-subsector basis.

In the search for a sustainable way to fund the Compensation Scheme of Last Resort, it must be worth considering a model similar to other community-wide protections, such as the Emergency Services Levy. A small, broad-based levy applied at the product level across all managed investment schemes could provide a fair and resilient funding model. After all, the CSLR exists to protect investors, and spreading the cost across those who ultimately benefit aligns well with that purpose. This approach could provide long-term stability while maintaining fairness across the sector.