New advice fee consent rules come into effect on Thursday July 1, and a recent survey of financial advisers by CoreData suggests not everyone is necessarily well prepared for the changes.

The new rules require advisers to obtain written consent from clients before they can deduct fees from the client’s account, to set out the services and for the coming 12-month period as well as estimate the fee, and to review ongoing fee arrangements each year.

There are additional new rules relating to the deduction of advice fees from superannuation accounts; the trustee of the fund must (a) receive a copy of the client’s informed consent to paying the fees, and (b) confirm that the fee being charged is in-line with the agreed advice arrangement.

CoreData’s Adviser Pulse Check Survey, conducted in the second quarter of 2021, shows that irrespective of the number of clients a practice has, the most common method of deducting fees is a combination of payment from the client’s investments and direct payment by the client.

For firms with 100 to 200 clients, for example, two-thirds employ the mixed method, while just over two in 10 (22.2 per cent) only deduct their fees from the client’s investments, and less half that number (8.9 per cent) charge the client directly.

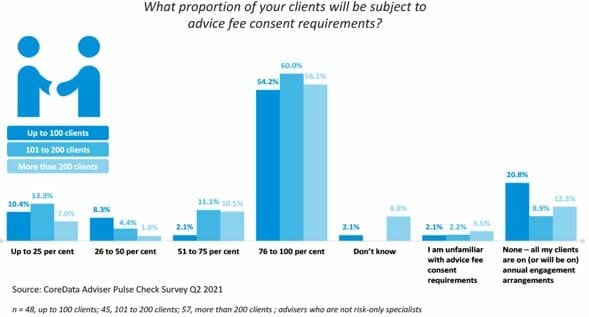

Well over half of all practices (57 per cent), irrespective of client numbers, expect at least three-quarters of clients to be subject to advice fee consent arrangements. A much smaller proportion (13.9 per cent) expect all clients to be on annual engagement arrangements. The frequency of the latter is greatest among smaller advice practices (up to 100 clients), where around one in five (20.8 per cent) think they’ll have all clients on annual engagements.

The process of receiving that consent is work in progress: around one in five (19.9 per cent) practices have already received consent from only half the number of clients they need to (including 13 per cent of practices that have received consent from less than a quarter of the clients they need to); one in six practices (16.6 per cent) have not received consent from any clients at all, but “plan to start”.

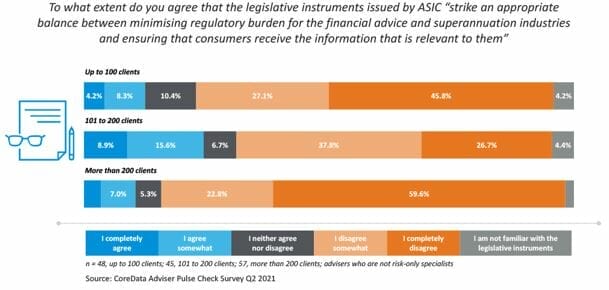

Advisers clearly are not happy with the legislative instruments issued by ASIC to enact the consent arrangements: about three-quarters (73.5 per cent) of advisers say they disagree somewhat or completely that the ASIC instruments “strike an appropriate balance between minimising regulatory burden for the financial advice and superannuation industries and ensuring that consumers receive the information that is relevant to them”.

Unsurprisingly, perhaps, it’s practices which have most clients and which have the greatest task ahead of them to obtain client consent that disagree most, with more than eight in 10 (82.4 per cent) dismissive of the regulator’s actions.

ASIC has also issued example ongoing see and non-ongoing fee consent forms, but knowledge that these forms exist is relatively low; just over half (52.3 per cent) of advisers are aware. Where they do know the forms exist it’s because their licensee has been on the ball and has brought the forms to their adviser’s attention.

This is another, albeit small, example of the divergence in the performance of licensees. Our 2021 Licensee Research shows that some licensees continue to support advisers well, keeping them up to date with regulatory and legislative changes across the industry and helping them through it; others are struggling either through resourcing or, to put it bluntly, competence issues.

Around six in 10 (60.1 per cent) advisers have received from their licensee a form of words they can use to obtain consent from clients.

It may be that this form of words is quite close to (or indeed lifted directly from) the examples provided by ASIC, but either way, if the licensee has done this work it’s one less thing advisers have to think about at a time when there’s plenty of other things going on to keep them occupied.

Leave a Comment

You must be logged in to post a comment.