While researchers and Professional Planner poll respondents predict adviser numbers will soon drop to 13,000 and below, many industry observers quietly predict the number will settle at a far more conservative 15,000 to 17,000.

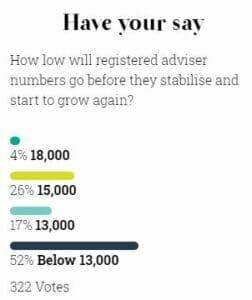

A recent Professional Planner poll asking advisers “How low will registered adviser numbers go before they stabilise and start to grow again?” received a grim response; 17 per cent believe the number will reach 13,000 and a further 52 per cent said the number would fall below 13,000, giving a total of 69 per cent that see adviser numbers falling to at least 13,000.

A further 26 per cent said adviser numbers would bottom out at 15,000 and only four per cent – out of 322 votes – said 18,000 would be the low point.

The numbers match predictions made by Adviser Ratings, which said in its latest Advice Landscape report that adviser numbers would fall from 20,764 at the beginning of 2021 to 13,154 by 2023 due to a confluence of pressures including the education mandate and a threats to insurance advice revenue.

The fall will be exacerbated by a slim funnel of new entrants; only 900 are currently studying FASEA-approved degrees, a fraction of which will complete the professional year and become authorised representatives.

Not everyone agrees on the nadir of the adviser exodus, however.

Not everyone agrees on the nadir of the adviser exodus, however.

Despite the research and the poll results, many in the industry believe adviser numbers will bottom out between 15,000 and 17,000 before gradually rebounding.

“The most likely number at January 2022 is about 17,000,” says Tom Reddacliff, chief executive at Encore Advisory Group. “After that you would think the vast majority will go through to 2026.”

“My response would be somewhere around the 16,000 number,” says ex-adviser Karen Eley, who now operates as a money coach under the Synchron banner.

“I think about 17,000 will pass the FASEA exam,” says Perth advice recruiter Simon Burke.

“Think of it from the demand perspective,” says Steven Fine, founder at advice brokerage firm Growth Focus. “Most practices we work with have grown over the course of the pandemic. If there’s growth then there is demand… and as long as there is demand for services there will be a planner to fill that demand. I think the number at the end of the year will be around 16,000.”

Exam numbers at a glance

While the spectre of 13,000 or less as a low point for adviser numbers remains a distinct possibility, the numbers coming out of FASEA tell a different story.

After January’s exam the education authority reported 12,000 advisers had already passed, with five sittings left on its schedule.

According to FASEA an average of 1,323 advisers have sat each exam, with a pass rate of 78 per cent across all exams. This success rate is declining, however – only 67 per cent passed in January. Regardless, if the attendance numbers hold up and the pass rate stays around 70 per cent another 4,600 advisers would join the qualified ranks, which would put the total well north of 16,000 in 2022.

An increase to 16,000 is far from a fait accompli. The number of sitters could decline as the ranks of advisers waiting to be tested thins out (indeed, only 1,079 sat in January, almost 20 per cent below the average). The pass rate could also drop well below 70 per cent as second sitters and first timers who have procrastinated due to a lack of confidence fill exam seats.

Yet the FASEA data indicates the tide-line on January 1, 2022 should be well north of 13,000 advisers.

A post exam world

There are a variety of views on exactly when adviser numbers will bottom out.

Some believe the exam cut-off date of January 1, 2022 will be a proxy ‘commitment’ date for advisers, and numbers will stabilise almost immediately. Anyone who does the exam, in other words, is here to stay.

Others think numbers will continue to drop after the exam cut-off date, and won’t stabilise until after the equivalent degree requirement kicks in at the start of 2026.

According to Encore’s Reddacliff the adviser run-off could be as high as 1,000 per year until then.

“That rate of natural attrition might continue as it will take a long time for new entrants to offset losses,” he says.

Another feasible scenario is that numbers stabilise after 2022 but then drop off significantly in the lead up to January 1, 2026. Some advisers might be willing and able to pass the exam and continue practising for another four years, yet reluctant to complete the equivalent degree requirement.

All scenarios – including a drop in numbers to below 13,000 – are in play. Industry participants may not agree on the low point, or the timing of it, but most agree on two things; attracting new talent will be key, and the industry will eventually come back in better shape than it is now.

“I am confident the financial services profession will emerge stronger and that the public, media and regulator’s trust will return,” says North Queensland adviser Peter Horsfield. “Only after these foundations have been laid can the rebuilding of the adviser numbers begin.”

Leave a Comment

You must be logged in to post a comment.