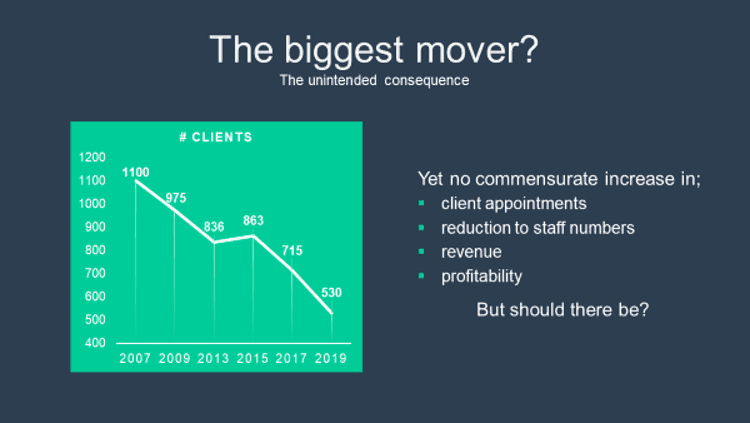

The headline takeout from our recently released industry analysis (Future Ready VIII) is undoubtedly the dramatic reduction in average client numbers per firm from 715 in 2016 to 530 this year. A far cry from the 975 per firm in 2009 and the 1,100 clients (or were they simply policy holders?) being served by the average Australian practice twelve years.

*Derived from HealthChecks completed by practices during the period 2007 to 2018

So, what’s been driving this reduction in client numbers per firm? A couple of factors spring to mind:

- Rising costs and increased compliance responsibilities are no doubt, two of the major reasons, leading some business owners to pull back on their ‘exposure’ and reduce the number of clients they serve.

- In a similar fashion to the previous point, the drive towards ‘fee for service’ has meant that advisers simply can’t manage higher numbers of clients within their existing business model.

- We’ve long encouraged practices to segment their client base, remove cross subsidisation between the various segments and ensure they’re only providing services to those who are actually paying for it. “Treat clients fairly and respectfully, but not equally” has been a Business Health mantra since we launched in 2000. Today, 80% of practices tell us they actively segment their clientele.

- Some practices have drilled down into a particular market niche (multiple niches maybe) and in delivering specific services to their niche, they’ve opted to let their other clients go?

- In an effort to control expenses and/or access some capital value, we’ve observed practices offer parcels of clients to other advisers, who are better placed to continue providing the services these clients need. A solid business strategy for sure, which we hope is further leveraged by the reinvestment of proceeds of any such sale back into the business itself.

- Finally, there’s no doubt that the ‘greying’ clientele has come well into play. From our client survey tool (CATScan), we learn that 49 per cent of clients are aged 60+ years, while 40 per cent are already retired. Their needs are certainly changing and we can’t help but wonder if their advisers haven’t yet picked up sufficiently on this subtle demographic shift?

Irrespective of the reasons driving this reduction in client numbers, our analysis indicates there are less Australians being serviced by a financial adviser today than previously. This is occurring during the greatest wealth transfer in our history, as ageing parents (the majority of today’s financial advice clients) look to navigate the vagaries of retirement and pass on their wealth in the most effective way, in what can only be described as an extremely complex financial services environment. If ever experienced, professional advice was needed, it’s surely now.

So how can practices profitably provide ‘non high-wealth’ Australians with the advice they need?

I believe the answer will centre around new business models which will embrace:

- A modular approach to providing advice – something akin to lifestyle, event or milestone advice. A specific need arises and help (advice) is needed.

- A much larger base of clients, with a substantial number not requiring a specific service from their adviser in every year (and therefore not paying an ongoing fee at the time of their ‘non need’).

- A clearly segmented clientele – supported with differentiated offers and pricing. Cross subsidisation will not be employed.

- Increased marketing capability – internal or outsourced to an external expert.

Lots to consider for every adviser and while different roads will be taken, I’m pretty sure that those who arrive in good shape will share a few common traits. These will include a flexible approach to business models, an openness to new ideas and a willingness to listen.

Perhaps the one thing that is imperative and underpins all of the above, is the need for business owners to regularly take some time to work on (and not ‘in’) their business, and identify the opportunities therein.

Leave a Comment

You must be logged in to post a comment.