Cheaper administration and better pricing on cash holdings is on the way according to an analysis by investment bank and global research firm, UBS.

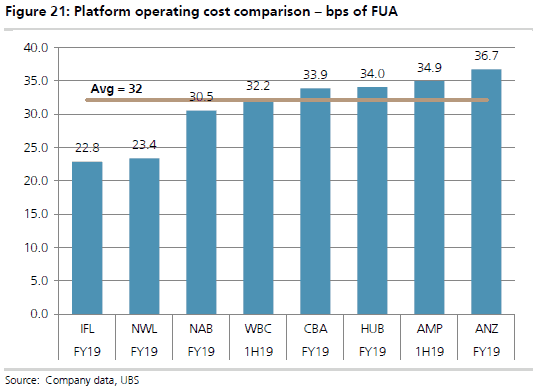

While the cost of operating platforms by large institutions might not appear to allow much headroom for pricing reductions, these adjustments are expected to be made on the back of outsourced deals with cheaper third party administration providers or through possible mergers designed to build scale, this analysis shows.

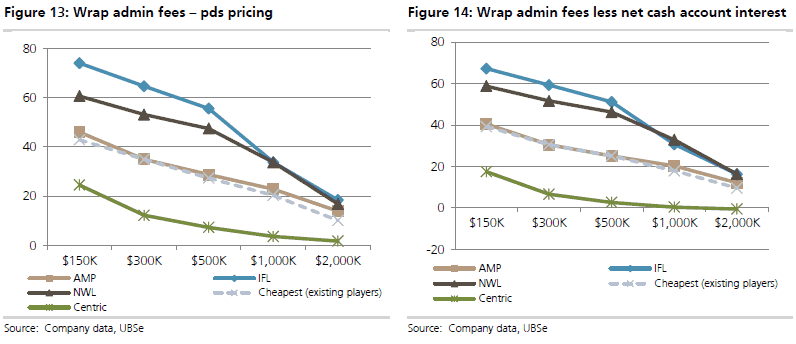

The approximate 30 to 40 basis point price reduction for wrap account balances between $300,000 and 500,000 institutions have made since mid-last year could be the tip of the iceberg, Kevin Chidgey noted in his latest Australian wealth management, the next wave of disruption report.

Chidgey pointed to a new wave of wrap providers with admin fees as low as 7 to 12 basis points offering above RBA rates for cash holdings as the likely catalyst for further cost reductions; Findex’s Centric, Spitfire and FinClear were three of the “next wave” of admin providers Chidgey mentioned.

Admin fee structures across these new entrants are relatively simple, with either flat fixed annual admin fees and/or low single tier FUA-based fees, Chidgey summarised. In addition, the report noted, FinClear removes the need for a linked cash account while Centric and Spitfire offer RBA+ returns on linked cash accounts.

The continued downward pressure on admin pricing is also evident in the discounting undertaken by the specialty platform providers like Netwealth and HUB24. Chidgey pointed to Netwealth’s Strategic Partnership Pricing – below its advertised “rate card” pricing – as evidence of continued pricing pressure in the platform space.

“Accelerating adviser fragmentation has seen once dominant vertically integrated wealth platforms shed FUA at an increasing rate to more contemporary specialty platform providers such as Netwealth and HUB24. However, with specialty platform providers disruption driven more by technology and independence than fees, we believe the door has been left ajar for a new wave of entrants,” Chidgey stated.

While base admin fees from this new wave of platform entrants are consistently below major wealth managers and specialty platform providers, the gap widens further after taking into account net interest earned on clients’ linked cash accounts, the analysis noted (see below).

Since mid-last year AMP, Commonwealth Bank, Westpac’s BT, National Australia Bank’s MLC and Macquarie have all repriced key wrap platform offerings, with admin fees now tightly grouped around 30bps at a $500,000 account balance.

BT was the first to make a splash with new pricing via an advertising campaign in mainstream newspapers with comparative research from Chant West; MLC announced its repricing at the start of this year.

While Chidgey’s analysis showed the cost base of the respective wealth managers meant their ability to continue to cut pricing would be limited (see below), he added that these institutions might need to find other ways to compete as pricing for administration would continue to come down.

The UBS analysis predicted mergers and acquisitions between existing large platform providers as a way to enhance scale and bring cost bases down. It also predicted that existing local providers could look outsource to giant global third party providers.

Leave a Comment

You must be logged in to post a comment.