I have been investing professionally my entire career and I have to confess to being a little perplexed for the first time.

In 1999, when the tech sector first boomed, it was obvious that markets were on borrowed time. I was working at Merrill Lynch at the time and by selling my clients out of all the hot IPO’s on the first day of listing, I lost some of my clients to other advisers. Clients were unhappy with the paltry 40, 50 or 90 per cent returns they made on the first day because the shares they briefly owned in profitless companies continued to appreciate to many multiples of their IPO price.

That same year I gave a lecture for the Australian Stock Exchange, in their then new theatre under Bridge Street in Sydney. It was literally standing room only. The fire department turned up to clear people that were seated in the isles. I asked those gathered whether they’d be happy if their fund manager returned them 20 per cent in a year. Nobody raised their hand. Pointing to the crowded room, I told the audience conditions were abnormal and wouldn’t last.

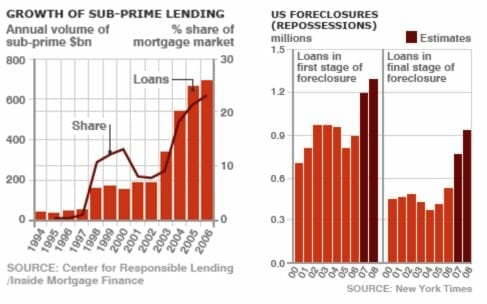

Then eight years later, in 2007, I gave a presentation to clients and invited Robert Gottliebsen to present alongside me. I revealed the collapse of the US real-estate boom and showed charts revealing the proliferation of risky subprime loans that would subsequently lead to a spike in mortgage resets and ultimately in defaults, beginning that year and worsening in 2008.

Figure 1. Way back in 2006; Estimated jump in subprime defaults.

Today I see parallels.

Like 2004 through to 2006, money has been cheap and finance abundant. And like 1999, that money has found its way into technology companies.

It all started with a Wall Street Journal article published in 2011 by venture capital icon and Netscape co-founder Marc Andreessen from Andreesen Horowitz entitled Why Software Is Eating the World and prompted by HP jettisoning its PC business and Google buying Motorola’s cell phone handset maker.

The article was written at a time when the market hated technology stocks. Apple, for example, was trading on the same PE of 15 times earnings as the broader market but Andreessen argued that we were “in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.”

He was absolutely correct and subsequently made billions investing in Skype, Facebook, Pinterest, Twitter, Lyft, Airbnb, Slack, Groupon and Zynga among others.

Part of his success however must also be attributed to the policy of central banks to reduce rates to zero, which disincentivised saving, and to engage in Quantitative Easing, which spurred speculation in everything from low digit licence plates, to art, collectable cars, wine and to corporate debt, venture capital and private equity funds.

As interest rates remained low and returns on cash remained poor, increasingly large allocations to venture capital from pension funds and endowment funds enabled VC Firms and Private Equity Funds to grow in size beyond anything ever seen before. Today, Softbank’s Vision Fund has raised US$100bn and its founder aims to raise another US$100bn fund every two years. Meanwhile Blackstone has closed its eighth private equity buyout fund at US$22bn – its largest ever.

And while traditional PE and VC funds have amplified their balances, so too has the number of new entrants driving capital availability for start-ups looking to change the world.

More money chasing a limited number of opportunities inevitably drives up prices. But it doesn’t change the underlying intrinsic value of a company.

But in his 2011 article, Andreessen also called on investors in 2011 to stop obsessing about valuations.

And if the sheer volume of money chasing VC and private-equity-backed start-ups isn’t enough to worry about, Andreessen’s 2011 clarion call to ignore valuation should cause us to pause and reflect.

Furthermore, investors should heed the lesson repeated throughout history, that world-changing technology does a lot more for consumers than it does for its investors. Think of the television, commercial flight and the motorcar; history records the billions that have been collectively lost, transferred from investors to consumers, through lower prices and bankruptcies.

But let’s suspend reality for a moment and reflect on the moment in history we are now in.

Since Andreessen’s opus was published, the best returns have most certainly come from ignoring valuations and investing in high growth companies with little or no earnings.

Pitchbook recently published the results of a study into the performance of ‘exits’ by private equity and venture capital firms in Unicorns (start-ups that surmount a billion-dollar valuation).

The paper, entitled; Searching for Validation, an analysis of valuation performance for $1 billion+ VC-backed exits, revealed that from the universe of companies examined, a high percentage (64.3%) were unprofitable on an EBITDA basis. This was diplomatically attributed to the “companies’ stage in the life cycle and common prioritisation of growth over profitability”.

The problem with such a euphemistic approach to explaining a lack of profit is that it ignores the impact abundant capital has had, and which has virtually defined the bull run since Andreessen’s article in 2011.

Cheap and abundant funding helps to patch over a high cash burn and defer the examination of whether the enterprise may ever be profitable.

While Pitchbook’s study also revealed that post-IPO performance favoured profitable companies, perhaps more worrying however was that the report attributed the more modest success of money-losing companies to “how public market investors have adapted to the current ecosystem” and allowed “businesses to scale” amid an increasing “willingness to accept negative to minimal cash flows for longer time periods”.

Indeed, for the record 2019 batch of Unicorn IPOs (Exits for VC and PE firms), including Pinterest, Lyft and Uber, investors may need to wait a very long time for a profit. In Uber’s S-1 Prospectus, on page 105, the company states; “We expect Adjusted EBITDA losses to increase in the future as we continue to invest in our platform offerings…”

The Pitchbook study also notes that more recent IPO’s aren’t experiencing the same ‘step-up’, in valuation from the last capital raising round, as they have in the past. This might be a function of the fact that “there’s simply less room for growth by the time the current generation of start-ups is going public” adding, that its “lending credence to the idea that, these days, it’s the private markets where most value creation occurs”.

That’s a very worrying conclusion; that ‘on-paper’ re-valuations, by investors willing to pay too much because they have too much money, is where all the value ‘creation’ occurs.

In late March ride-hailing promoter Lyft went public at an initial market cap of more than $20 billion. In so doing it launched a veritable tidal wave of Unicorn IPOs, some with mind boggling market valuations.

In the past, when a VC firm exited at a billion-dollar valuation, it was a rare event. In 2010 for example only four companies in the US made the grade with a combined valuation of US$5.1 billion. In 2018 however there were 33 with a combined valuation of US$76 billion.

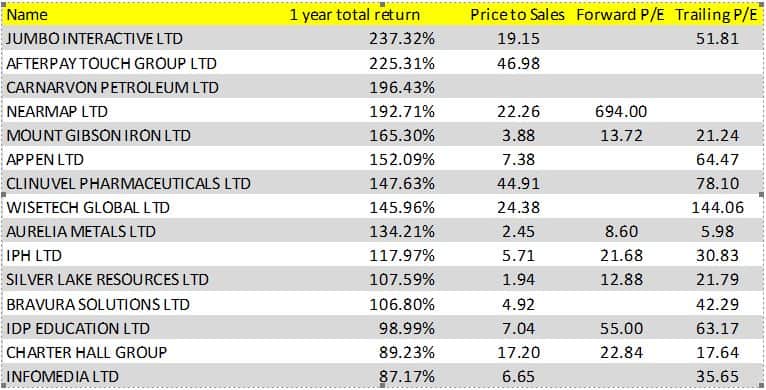

In Australia, the experience for Tech Stock investors has been equally rewarding if only in percentage, rather than absolute, terms.

Of the fifteen top-performing stocks over the past 12 months almost half can be categorised at technology-related. The top 15 currently have an average price-to-sales ratio of 15 times. Read that carefully, that’s not Price-to-earnings, we are talking price-to-sales! And of the companies that recorded a profit last year, the average PE is almost 50 times.

But if we only take the six tech stocks in the list, we find an average price-to-sales ratio of 19 times, and of those that made a profit last year, they’re trading on a trailing PE of 72 times.

Table 1. Top 15 performing ASX stocks. 12 months to April 15, 2019.

John Kenneth Galbraith in The Great Crash defined a bubble thus;

At some point in a boom all aspects of property ownership become irrelevant except the prospect for an early rise in price. Income from the property, or enjoyment of its use, or even its long run worth is now academic… what is important is that tomorrow or next week, market, market values will rise, as they did yesterday or last week, and a profit can be realised…”

I believe we have now reached that point. The boom has become a bubble and investors should be especially cautious this year.

Leave a Comment

You must be logged in to post a comment.