NAB chief executive Andrew Thorburn called the bank’s decision to unload its wealth arm a “strategic highlight” in the bank’s 2018 full-year results this morning and lamented the $360 million the bank was forced to pay in remediation costs.

Speaking on a media call shortly after the release, Thorburn said that while some remediation costs were part of “[business as usual] for the bank”, this year’s bill of $360 million – “required mainly in the wealth business” – was “a significant item”.

Thorburn made special mention of the administration and implementation costs included in the $360 million total, saying they accounted for “$100 million or so”.

“We’re comfortable with where we’re at, but there’s no question it’s a disappointing outcome,” Thorburn said.

Wealth exodus

On May 3, a week after the Hayne royal commission concluded its hearings into financial advice, NAB announced its intent to “reshape” its wealth management offering. Advice group JBWere and investment platform nabtrade will stay with the bank while advice, asset management and the other MLC brands would be unloaded. The retained elements will be folded into the private banking division, and the wealth arm of NAB will cease to exist.

On the day of NAB’s demerger announcement, then-head of consumer banking and wealth, Andrew Hagger, told Professional Planner “the timing felt right”.

NAB sits alongside Commonwealth Bank and ANZ Banking Group in deciding to demerge its wealth management business. Of the banks, only Westpac-owned BT will remain invested in wealth, anchored by a half billion-dollar investment in its Panorama platform. AMP’s position in the wealth market remains under a cloud after recently announcing its intention to divest its AMP lIfe and New Zealand wealth management businesses in 2019 – a move that precipitated a $2.4 billion drop in its market cap last week.

In the results document released today, Thorburn explained that NAB’s decision allows the MLC business “to determine its own strategy and investment priorities to better deliver for customers and enhance its competitive position”.

On a subsequent investor briefing call this morning Thorburn suggested that returns, along with scandals and the associated costs, were to blame for the decision to excise the wealth arm.

“We’ve divested major portions of the banks that weren’t going to be giving us the returns we needed,” he said.

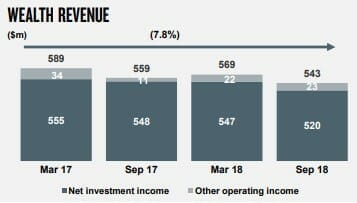

While the bank reported a headline underlying profit figure a tick under $9 billion for the year, wealth provided a small – and decreasing – part of that (see graph).

Hedging its bets

The way MLC will be sold remains unclear, as does the appetite for institutional wealth businesses in the wake of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. NAB used today’s announcement to reaffirm its intent to exit the market via demerger, initial public offering or trade sale options. The report stated that MLC investors will hear more from the bank on the matter at a briefing “prior to [the first-half 2019] announcement”.

On the investor briefing this morning, chief financial officer Gary Lennon commented on CBA’s recent sale of Colonial First State Global Asset Management to Japanese giant Mitsubishi UFJ Trust and Banking Corporation for $4.13 billion.

“It does send a signal that there are trade sale buyers out there,” Lennon said. “When you have one Japanese bank show interest in an asset sale, there are others.”

NAB continues to hedge its bets, though.

“We’re not pinning ourselves on any stream at the moment,” Lennon said. “We will zero in on the preferred options in the next six months.”

Leave a Comment

You must be logged in to post a comment.