In just a few weeks from now, the boom gates come down on the financial planning industry, in effect ringfencing existing advisers and requiring all new entrants to the industry to hold a university degree approved by the Financial Adviser Standards and Ethics Authority (FASEA).

The new-entrants requirement from January 1, 2019, is the first of a series of standards for education, professionalism and ethics that will come into effect over the next five years, culminating with the provision that all existing advisers must have a bachelor’s degree or equivalent qualification, or higher, by January 1, 2024.

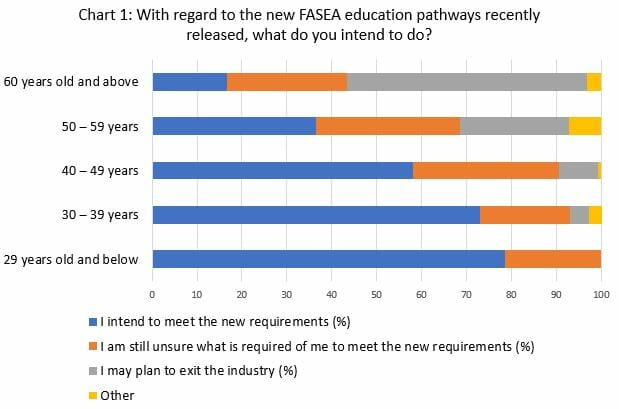

It is now becoming clearer just what impact the new standards will have on the advice industry over the next five years. CoreData’s analysis of adviser intentions reveals that just over 20 per cent of all advisers “may plan to exit the industry”, depending on exactly what recognition is ultimately given to experience, prior learning and existing industry-based designations.

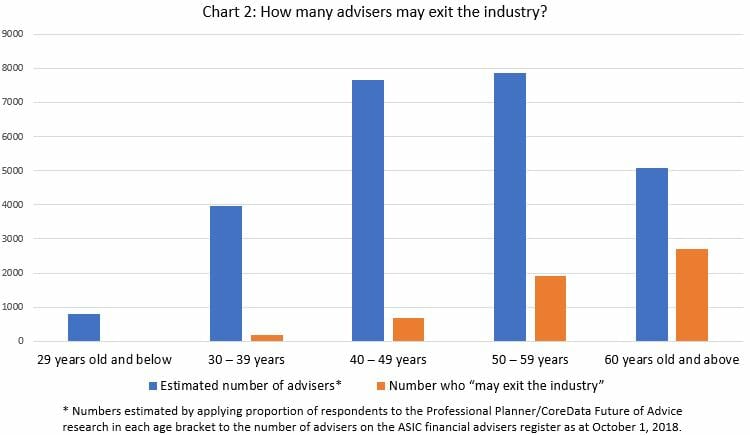

That equates to about 5450 advisers out of a total of more than 25,000 on the ASIC financial adviser register who say they may leave the industry over the next five years. Older advisers are understandably more likely to be thinking about leaving than younger ones, with more than half of all advisers aged over 60 saying they may exit, along with just under a quarter of advisers aged between 50 and 59.

Conversely, younger advisers seem unfazed by the education requirements. Less than 5 per cent of advisers aged under 40 – and no advisers aged under 30 – say they plan to exit the industry in response to the new standards. More than three-quarters of advisers aged under 30 say they intend to meet the standards, while just under three-quarters of advisers aged 30 to 39 plan to do the same thing. Well over half of advisers aged 40 to 49 also plan to meet the new requirements, along with more than a third of advisers aged 50 to 59.

Conversely, younger advisers seem unfazed by the education requirements. Less than 5 per cent of advisers aged under 40 – and no advisers aged under 30 – say they plan to exit the industry in response to the new standards. More than three-quarters of advisers aged under 30 say they intend to meet the standards, while just under three-quarters of advisers aged 30 to 39 plan to do the same thing. Well over half of advisers aged 40 to 49 also plan to meet the new requirements, along with more than a third of advisers aged 50 to 59.

While FASEA has issued broad guidance on the options advisers have to meet the 2024 deadline, there is still considerable uncertainty about the details of the path ahead.

The research has found that another 7300 or so advisers, or about 30 per cent of the industry, say they still do not know what is required of them to meet the new standards.

As the exact requirements become clearer in the weeks and months ahead, this group of “undecideds” will make a decision on whether to go or stay, and could skew the numbers either way.

The figures in this analysis are based on the Professional Planner/CoreData Future of Advice surveys conducted in September and October this year. To calculate the number of advisers who may choose to leave the industry between now and 2024 (or who say they still don’t know what to do) the proportions of survey respondents in each age group were applied to the 25,347 authorised representatives on the ASIC financial advisers register as at October 1, 2018.

These education reforms have been a long time coming and trace their genesis back more than four years, to mid-2014, when a Parliamentary Joint Committee on Corporations and Financial Services inquiry, chaired by Senator David Fawcett, examined the professional, ethical and education standards of the financial services industry.

That inquiry’s report, published in December 2014, made a series of recommendations to raise standards in financial planning and formed the basis for some of the reforms that are coming. Its original timetable suggested the reforms could be in place by January 1, 2019, but financial planning being financial planning, the process has taken much longer than anyone initially expected, as the nuances of reform have been thrashed out and stakeholders have agreed upon transitional timetables.

It was not until early 2017 that the Corporations Amendment (Professional Standards of Financial Advisers) Act received assent and formally introduced the new standards, and it was not until July 1 the same year that FASEA came into being. With the delays, what was initially going to be the deadline for meeting new standards will end up being just the start date for the transition.

An important factor in how effectively advisers will be able to upskill to meet the new standards where necessary is how much support licensees can provide to help them get there.

The Professional Planner/CoreData surveys show that a majority of planners say their licensee has yet to indicate how they will help advisers cover the time and the cost – including to study for and sit the exam, which all existing advisers must do by January 1, 2021.

More than a third of advisers say obtaining any new qualifications will be their personal responsibility. Less than 8 per cent of advisers will have the costs of upskilling fully met by their licensee; 4.2 per cent say their licensee will partly cover the expense.

There will be a reasonable amount of work required across the industry to reach the new standards. Only 1.6 per cent of survey respondents say their highest level of education achieved is a bachelor’s degree in financial planning. A further 23 per cent say they have a degree in a related field. Another 11 per cent hold a graduate diploma in financial planning and 6 per cent have a master’s degree in financial planning.

While education and professional standards for planners have had a long and sometimes difficult gestation, and have been surrounded by a miasma of misinformation, the overall effect of the reforms will probably be positive and will lift financial planners onto a footing more equal to that of other recognised professions.

That is a particularly important outcome in the wake of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which has substantially eroded trust not just in financial services generally but in financial planning specifically this year.

CoreData has tracked the level of trust in financial planning and seen it decline from a score of more than 60 at the beginning of the year to just 35 in the third quarter, before rebounding modestly to about 40 in the fourth quarter. The score is calculated by asking people how much they trust the industry, on a scale from zero to 10, where zero is complete mistrust and 10 is total trust.

A starting score of 60 denotes only mild trust overall anyway, and a score that falls to 35 or 40 indicates a growing level of mistrust. Any steps that can be taken to restore public trust and confidence in financial planners and the services they provide should be welcomed.

Leave a Comment

You must be logged in to post a comment.