The term “financial adviser” probably has less baggage and is more aligned to professionalism than “financial planner”, experts believe.

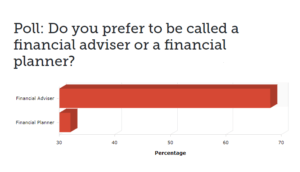

Further, in a recent poll conducted by PP Online and participated in by more than 600 respondents who are practitioners in the wealth-management industry, the majority (close to 70 per cent) now prefer to be referred to as a financial adviser rather than a financial planner.

“Adviser is closer to the profession,” says Dr Simon Longstaff, director of the St James Ethics Centre and a member of the Financial Adviser Standards and Ethics Authority (FASEA) board of directors.

As part of the same legislation that’s responsible for bringing FASEA into existence, both “financial adviser” and “financial planner” are legally restricted terms for use by registered and recognised purveyors of the service.

While both financial adviser and financial planner are reserved side by side under the legislation, they’re not perceived to be on the same footing by the general public and their future use will probably take different paths, Longstaff tells Professional Planner.

“If you’re a financial planner, then you’re someone who specialises in the provision of a technical service – like if you contract a plumber they’re going to come in and fix your pipes. If you’re an adviser, you provide a much broader range of higher-order services,” Longstaff explains.

Longstaff, who also holds board positions with the Banking and Finance Oath, BT’s professional standards council, Westpac’s stakeholder council and the IAG ethics committee, had input into the ethics component of the new FASEA standards, which are now part of an industry consultation process.

The connotations attached to financial planner and financial adviser in the eyes of experts and the public may be a surprise to a few practitioners, the PP Online survey reveals.

The connotations attached to financial planner and financial adviser in the eyes of experts and the public may be a surprise to a few practitioners, the PP Online survey reveals.

“Why would anyone want to call themselves a financial adviser? Any junior work experience bank employee can call themselves an adviser, yet [the term] financial planner shows that the person has studied and has many years of experience,” one adviser commented after responding to the poll.

“Financial adviser might be more consistent with the direction to professionalise the industry,” says Lujer Santacruz, who is a lecturer in finance at the University of Southern Queensland’s School of Commerce.

In 2011, Santacruz penned a paper for the Australasian Accounting, Business and Finance Journal arguing the term ‘dealer group’ added to the general perception that financial advisers were not objective when making financial product recommendations.

Santacruz made reference to investigations and inquiries at the time – including the Parliamentary Inquiry headed by then Labor MP Bernie Ripoll in 2009 – noting that the continual use of the term dealer group was a serious impediment to the industry’s desire to professionalise.

The term, Santacruz argued, weakened the credibility of financial advisers by painting them as product distribution for institutions.

In light of the revelations from subsequent inquiries, including the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Santacruz notes his personal view is that the term financial planner “seems to be tainted”.

At a time when the need to professionalise is at the front of the minds of everyone involved with setting and meeting new education and ethical standards, Longstaff believes destiny is on the side of the adviser rather than the planner.

“If you say ‘I’m your adviser’, then you do more than just make a plan. If you are talking about succession in a family, family issues and life issues generally, then you’re providing advice about issues that impinge on the lives of your clients,” he says. “If you think of yourself as a planner, and only a planner, then you are limiting the horizon of the service you provide to your clients and to the community.”

Leave a Comment

You must be logged in to post a comment.