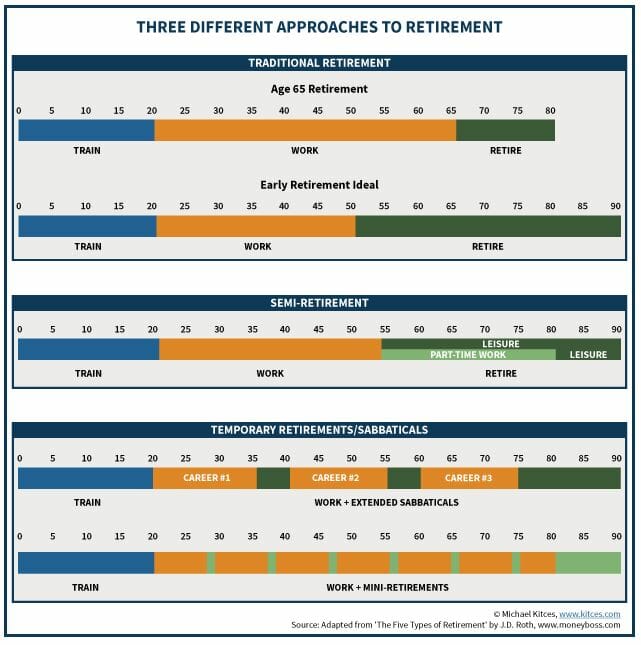

The traditional approach to retirement is relatively straightforward: save and invest as much as you can, for as long as you can, starting as early as you can, to accumulate enough savings that you’ll no longer need to work and instead can enjoy a life of leisure.

For those who struggle to save in the US, Social Security provides some retirement safety net; for everyone else, the more and faster you save, the earlier you can retire and the more leisure time there may be.

The problem is that a growing base of research finds fewer and fewer people want a retirement of all leisure and no work. Thanks in large part to our hedonic adaptation abilities – we quickly adjust to our new circumstances – retirement is boring for many.

Barely half of today’s retirees state that they never intend to work again and barely one-third of pre-retirees intend to spend retirement not working indefinitely. Instead, whether it’s part-time work, entrepreneurialism, an encore career or some other path, retirement is less and less about not working at all and more and more about finding a different kind of engagement, which may still involve a non-trivial amount of employment income.

As a result, semi-retirement and ‘mini-careers’ interspersed with sabbaticals are emerging as two alternatives to the traditional retirement model.

The significance of these changes is that if traditional retirement doesn’t work for most people anymore, then the traditional retirement savings approach might not make sense either.

Because if retirement is really more about doing different and perhaps more fulfilling (but not necessarily zero-income) work, then it might not take nearly as much to retire as commonly assumed. Retirement portfolios might look very different if their primary purpose is to be a buffer for retirement transitions and perhaps scaled-back work, rather than to fund a period of earning nothing at all. Some people necessitate more savings but have a smaller average balance (as it’s built up and spent more than once), while other types of retirement would allow for less ongoing savings and smaller retirement account balances, supplemented by partial work in “semi-retirement” that could last for years or decades.

A future with different types of retirement could also increase demand for disability insurance – as a greater reliance on the ability to work and earn income puts us at a greater risk if that goes away – and increase the need for emergency savings, for more extended mid-career transitions.

From the financial adviser’s perspective, perhaps the greatest potential disruption from different types of retirement is that, for most of the alternatives to the traditional approach, retirees will never accumulate as large a retirement portfolio in the first place, which could substantially impair the feasibility of the assets under management-based retirement planning approach.

This is a summarised version of an article printed on the Kitces.com website, reprinted with permission. The full article can be found here.

Leave a Comment

You must be logged in to post a comment.