If a financial planning profession had existed during the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, the recent public hearings might have been a different experience for advisers, associations and institutions.

It’s always fun to speculate about what might have been, but before we do that, let’s define “profession”.

A paper published in the British Actuarial Journal by Clare Bellis in 2000, titled “Professions in Society”, and presented to the Institute of Actuaries national conference in the UK, provides a succinct and useful definition as a starting point:

“A profession is a vocation founded on specialised education and training, the purpose of which is to supply disinterested counsel and service to others, for direct and definite compensation, wholly apart from the expectation of other business gain. This definition implies that for a profession to be recognised as a profession, it first must be organised within a professional body.”

There are many definitions of “profession”, and simply calling something a profession, or calling an individual a professional, does not make it so. For example, some define athletes and musicians as professionals, when all they mean is the musician or athlete does what they do full-time and gets paid for it. It’s fair to say the kind of profession financial planning aspires to be is more along the lines of law, medicine, actuarial, engineering, architecture, and so on. These professions are organised in a particular and well-recognised way and conform to a structure outlined in Bellis’s paper. It states that a profession is built on three pillars: cognitive, normative, and organisational or structural.

The cognitive pillar of a profession is the specialised knowledge, training and accreditation its practitioners must possess. The normative pillar is ethical standards, codes of conduct, and a commitment to serving the public interest. The organisational or structural pillar is all about practitioners creating and being part of a professional association that has disciplinary powers over its own members, and whose work and focus supports both the cognitive and normative pillars.

Public trust and confidence

Financial planning is not yet a profession in the way it would like to think of itself because it lacks all of the structural elements outlined above. But such structure is supported by the Financial Adviser Standards and Ethics Authority’s (FASEA) new educational, professional and ethical standards for all advisers. Along with facilitating the development of a new profession, the standards will also begin the necessary task of restoring trust and confidence in the industry and its practitioners, by making advice look more like other recognised professions and improving the standing of its practitioners.

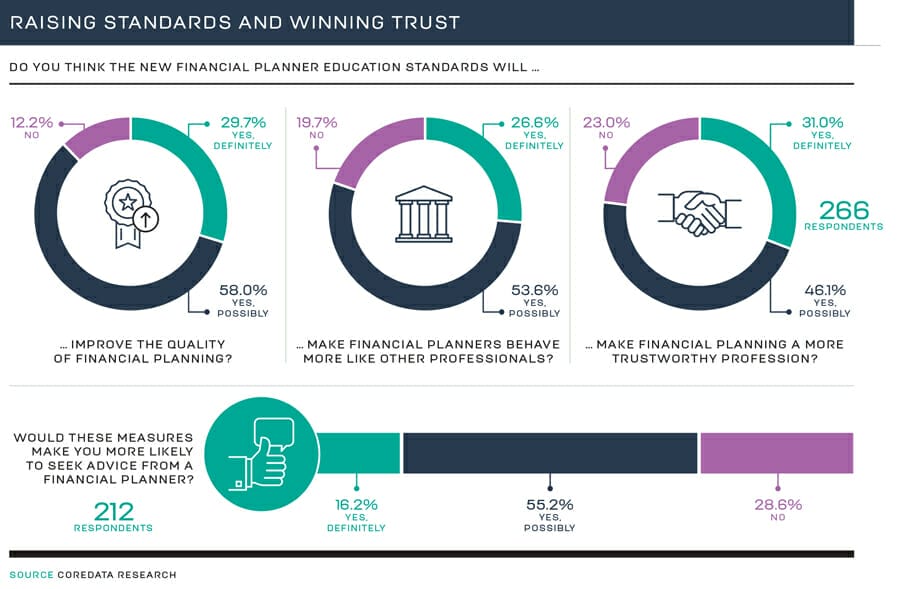

Even before professional standards have been finalised and implemented, there’s another ingredient that goes into defining a profession. It relates to a baseline level of public belief that the above measures can improve the quality of financial planning and make financial planners behave like other, more established, professions. While public belief might seem intangible, trustworthiness and willingness to seek financial advice can indeed be measured.

A survey of both advised and non-advised individuals by CoreData in the months before the royal commission shows the industry still has a way to go to be considered a profession in the hearts and minds of clients.

A number of issues that arose during the royal commission public hearings might have been treated differently had a profession, as defined above, existed.

Fee-for-no-service, ineffective disciplinary action by industry associations, and poor or non-existent background checking allowing substandard advisers to move freely about the industry – a profession should’ve addressed all of these before the royal commission got stuck in.

In fact, this might have removed the need for the inquiry to examine them at all. And many of the other issues that emerged might have been mitigated were the industry already demonstrating a deeper understanding of, and adherence to, professional and ethical standards.

Standards in practice

The Financial Planning Association Code of Professional Practice is not a massive document, at 38 pages, it’s shorter than the average Product Disclosure Statement and probably more concise than many statements of advice (SoAs). But it’s a roadmap for how professional standards and conduct in financial planning translate into practice, at least for FPA members, and even if not every member of the association has read the document, they have all signed up and agreed to comply with it as a condition of membership.

The document does not apply to advisers who are not members of the FPA, but one could assume that a financial planning profession would adopt broadly similar standards for all practitioners. It sets out plainly throughout that it’s a breach of the code to charge a client a fee if there is no service being provided. It’s a breach of the code if an FPA member does not set out in detail what the services will be, and when they will be delivered, along with how much they will cost.

Anyone who was a member of a profession, and who adhered to such practice standards, would have known fee-for-no-service arrangements were a prima facie breach of the code, and if they breached them they’d be subject to the profession’s disciplinary procedures. This leads to the issue of apparently ineffectual discipline of association members.

Within the structure of a true profession, membership in professional body would be compulsory, and not being a member would preclude an individual from practising.

In financial planning today, being a member of any association is optional and so, therefore, is compliance with an association-mandated code of ethics or professional standards. Treasury identifies this problem in its written submission to the royal commission. “Currently, not all individual financial advisers are required to be part of a professional association that regulates their conduct, in contrast to, say, lawyers and doctors, who are required to be individually licensed and members of a professional association,” Treasury states. So an individual who no longer wants to comply with an association’s code of practice or a code of ethics can simply resign their membership, with little practical impact on their ability to practise (apart, perhaps, from being forced to forfeit the Certified Financial Planner designation that the FPA administers). That’s a problem that needs to be addressed, and the FPA itself identifies it in its written submission to the royal commission: “At present, the licensee and regulatory systems do not place much value on the potential normative effect of professional disciplinary systems,” it states.

Discipline, advocacy clash

The FPA has proposed a separate, independent body, which could be called the Professional Conduct Commission (PCC) to mimic how professional misconduct issues are dealt with in established professions. Had that been in place already, practitioners might have taken the disciplinary process seriously, and the profession itself would have the teeth it needs to police its own members effectively.

Of course, this approach requires willingness on the part of a professional association to pursue disciplinary action as a priority, with the informed consent of practitioners to be subject to the disciplinary processes; and it requires the professional association to balance the twin objectives of attracting new members to the fold and potentially expelling members for misconduct.

The royal commission focused on this apparent conflict of interest, and a number of written submissions to the inquiry have suggested the membership and industry advocacy functions of an association should be independent of the disciplinary actions.

The FPA, for example, disciplines its own members through a notionally independent entity called the conduct review commission, which has an independent chair and deputy chair, and otherwise comprises financial planning practitioners who are FPA members but not FPA employees.

A helpful defense

A professional community that understands and lives up to its ethical and professional obligations and is properly organised as a professional body, with all that entails, can be a helpful, practitioners-led defence against shoddy practices and poor behaviour.

It is also helpful for identifying individuals with a track record of poor performance or inadequate expertise and stopping them from continuing to circulate. The collective commitment to identifying bad behaviour, poor practices and inadequate technical expertise, and to weeding out poor practitioners and expelling the worst of them, is a hallmark of any true profession.

Had financial planning exhibited these distinguishing professional characteristics, among others, then the royal commission hearings might have been quite a different kind of show.

Simon Hoyle is head of market insight at CoreData research and a former editor of Professional Planner.

Leave a Comment

You must be logged in to post a comment.