Last month, I argued that the S&P 500 was so overbought it didn’t take much to take the steam out of an impressive rally. The trigger turned out to be the wage rate data printed on February 2nd. The figure was an increase of only 2.9 per cent but it was a little above expectations. So the market decided that might mean a faster pace for interest rate hikes by the Fed. That interpretation was clouded because the 2.9 per cent included a significant contribution from a one-off increase in the minimum wage. Was the 2.9 per cent increase a blip?

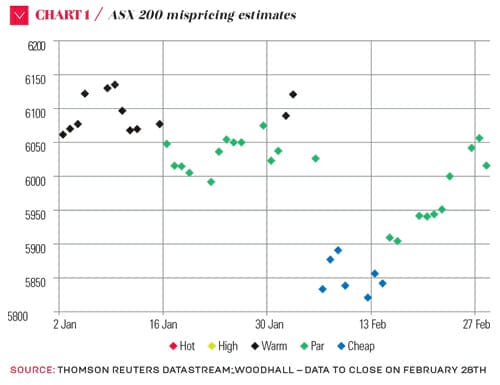

The S&P 500 fell by 10 per cent in a few days but it rallied hard to claw back most of that loss. Since the ASX 200 was not overpriced – at least by our measures – it fell by only 5 per cent. I show the ASX 200 for January and February in Chart 1. The colour coding relates to the mispricing (exuberance) discussed last month. Red (hot) would denote a correction of 6 per cent to 10 per cent or a prolonged sideways movement is expected. Yellow (high) would be just under that mispricing. However, black (warm) was the hottest it got in January.

Just when markets were starting to look like they’d wipe out the temporary losses in February in both those markets, new Federal Reserve chair Jerome Powell made his first appearance on Capitol Hill in the US to discuss matters financial. He was certainly impressive, and refreshingly expressed his personal opinions along with those of the broader Federal Reserve.

Powell was “upbeat” on the US economy and he stressed that, in his opinion, the economy has improved since the December meeting. Therefore, the three hikes in 2018 pencilled into the Fed’s “dot plots” suddenly looked like four hikes. The market immediately repriced the chance of four hikes at 34 per cent – a reasonable possibility but far from certain.

US 10-year Treasuries nearly got to 3 per cent – a four-year high – and equity markets slumped again. Yet, when we step back and see that inflation is below target and GDP growth is strong, there is no impending problem. The market always gets the jitters when new information jumps in front of it. The fundamentals are still strong, so these jitters create buying opportunities for investors holding too much cash – and times to sit it out for those fully invested.

US 10-year Treasuries nearly got to 3 per cent – a four-year high – and equity markets slumped again. Yet, when we step back and see that inflation is below target and GDP growth is strong, there is no impending problem. The market always gets the jitters when new information jumps in front of it. The fundamentals are still strong, so these jitters create buying opportunities for investors holding too much cash – and times to sit it out for those fully invested.

Returning to Chart 1, I note that there was a multi-day buying opportunity during January and February (blue dots). The important thing to note here is that the fundamentals in the S&P 500 and the ASX 200 have already strengthened this year (using our methods) so what was a bit pricey in January would be less so now.

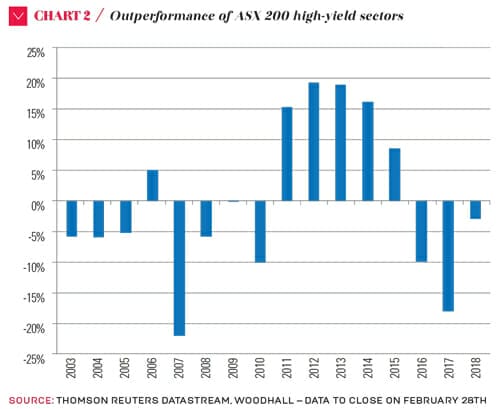

But where will the growth come from on the ASX 200 in 2018? I’ve updated some figures I used a few times a couple of years ago in Chart 2. There are four high-yield sectors (Financials, Property, Telcos and Utilities) and seven other sectors. The bars in Chart 2 show the differences between the total returns of the high-yield sectors and those from the other sectors.

The salad days of investing in anything with yield in 2011-14 started to wane in 2015. With rates so low in 2011-2014, investors turned to high-yielding stocks. Since 2015, the sectors of the ASX 200 have behaved more like those in pre-2011 days. With the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry ongoing and the threat of higher interest rates around the world, we do not see any big future for the high-yield sectors. Co-ordinated global growth will aid our other sectors.

Our forecast for capital gains for the next 12 months on the ASX 200 is just under 7 per cent, plus about 6 per cent in “grossed up” dividends (including franking credits). Not stellar but nice work if you can get it.

I think it will take at least all of 2018 to sort out where inflation and the Fed are heading. As a result, we expect more market volatility than in 2017 – but the dips present buying opportunities.

Leave a Comment

You must be logged in to post a comment.