There seems to be a strong trend these days against picking active managers over passive in Australian equities and elsewhere. The claim is, quite rightly, that one shouldn’t pay for underperformance – or even index-hugging.

In a world where there are, from time to time, major changes in which sectors or stocks are doing well, only by extreme luck could any manager excel in every short-time interval. So what is a reasonable expectation and how do you spot a potentially good manager?

With any manager that has a fixed style, such as growth or value, there must be extended periods when the fund does not outperform. Is it up to the investor to switch at the appropriate times? Of course, the investor can outsource such switching to a manager that offers this option – called active management. Unless one chooses one of these two options, it seems index-hugging funds or exchange-traded funds are the only ways to avoid material periods of underperformance.

The only way for a manager to guarantee tight index hugging is to hold, say, all 200 stocks in the ASX 200 (and charge no fees!). Once the manager chooses fewer stocks – say, 20 or 30 in a concentrated fund – it is game on. If we look at the Financials-x-REITS sector (financials for brevity) the enormity of the problem starts to emerge.

The only way for a manager to guarantee tight index hugging is to hold, say, all 200 stocks in the ASX 200 (and charge no fees!). Once the manager chooses fewer stocks – say, 20 or 30 in a concentrated fund – it is game on. If we look at the Financials-x-REITS sector (financials for brevity) the enormity of the problem starts to emerge.

This sector is about 40 per cent of the ASX 200 and the big four banks are about 75 per cent of that sector. In, say, an equally-weighted 20-stock portfolio, selecting a median-sized financials stock, such as Bendigo & Adelaide Bank, attaches a weight of 5 per cent in the portfolio, compared with only about half a per cent in the index. That’s a 10-times magnification of the impact on returns in the portfolio, compared with its impact on the ASX 200 benchmark.

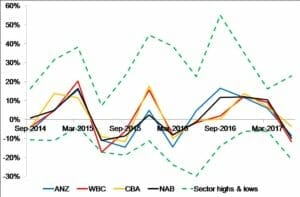

If we take a look the chart showing historical quarterly returns of the big four banks and the Financials-x-REITS sector over the last three years (left), we see that the big four moved in lock-step with the extremes of stock returns within the financials sector – and there seems to have been more upside than downside for the smaller stocks.

If 40 per cent of a 20-stock, equally weighted portfolio were to be allocated to this sector (making eight stocks) it would make plenty of sense to choose, say, just two big banks and six little ones to diversify away that small-cap risk. That way, if one little bank drastically underperforms, there is a chance the other five might carry some of the load. And if a little one that you don’t own charges ahead, you would hardly notice any underperformance because the ASX 200 would be largely unaffected.

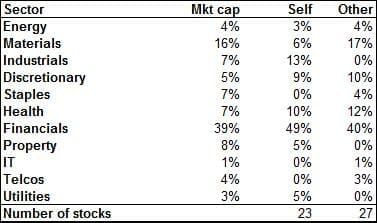

Now consider the market cap weights of all 11 ASX 200 sectors in Table 1 (below), together with the recent weights of a well-known concentrated fund, Other, and my personal portfolio, Self, as discussed in my Weekly on the website. It so happens that both Self and Other have had similar outperformance over the last three years – about 4 per cent annually, excluding fees (that’s why I chose that particular Other for comparison).

At this point in time, some of the sectoral allocations are strikingly different but there are many ways to get the same outperformance – but many more to fail! They key is in managing risks – particularly the one-side risk of a stock tanking. Given all of the talk of the potential disruption from Amazon and online retail in general, the amplification of index weights onto a small portfolio means, to me, that any stocks that might be challenged by disruption are not worth the risk of holding. The same goes for telecommunications stocks, with all of the potential technological developments in that sector.

At this point in time, some of the sectoral allocations are strikingly different but there are many ways to get the same outperformance – but many more to fail! They key is in managing risks – particularly the one-side risk of a stock tanking. Given all of the talk of the potential disruption from Amazon and online retail in general, the amplification of index weights onto a small portfolio means, to me, that any stocks that might be challenged by disruption are not worth the risk of holding. The same goes for telecommunications stocks, with all of the potential technological developments in that sector.

For Self, the only stocks in Discretionary at the moment are gambling stocks – no retailers! If I miss a winning retailer, it will have little impact on the index but it’s a major risk to my portfolio if it does not come off.

From my almost unbroken participation in investment committees over the last 15 years, I have noted widely differing attitudes towards cash among funds managers. All funds need a little cash, say 2 per cent to 3 per cent, to manage redemptions and administration costs. For funds with mandates that allow much larger cash allocations – some are 20 per cent to 30 per cent or even 100 per cent – there is no point in paying management fees for the cash portion unless it is actually used on occasion.

So the questions I would ask of a potential manager are:

- Does the fund switch themes or strategies over the cycle (or am I expected to do that for you)?

- Is the amplification of risks in the current small stocks warranted, given downside risk?

- Is the manager gambling on picking ‘beaten-up’ small stocks at the right time or is it trying for surer long-term bets?

- Is cash being reasonably managed or not charged for?

Leave a Comment

You must be logged in to post a comment.