A report released in March by the Australian Securities and Investments Commission painted a picture of major financial planning licensees unable to monitor and regulate the actions of their advisers properly, and unable to appropriately address wrongdoing and remediation when bad practices are revealed.

Report 515 Financial advice: Review of how large institutions oversee their advisers, didn’t just portray major institutions in a poor light, it called into question the legitimacy of the financial planning licensing regime, right at a time when new educational, ethical and professional standards are squarely in the spotlight.

The Financial Adviser Standards and Ethics Authority (FASEA), created by legislation passed the month before the ASIC report, will set new standards for all individuals who provide personal financial advice. But if the ASIC report

is representative, then questions must be raised about the long-term role of licensees in granting authority to financial planners to practice.

The divergence of clients’ and licensees’ interests places financial planners in a dual-agency role, which is well recognised as a source of conflicts of interest.

Emerging academic research suggests that: a dual-agency role creates “conflict by association” for financial planners; such a conflict is inconsistent with the objectives of the Corporations Act, therefore delegitimising the current licensing regime; and arguments for individual licensing are now stronger.

As financial planning practitioners continue to drive towards attaining the status of professionals, responsibility for adhering

to professional standards must fall to individual practitioners, free from the influence of an entity whose own aims may be at odds with those standards.

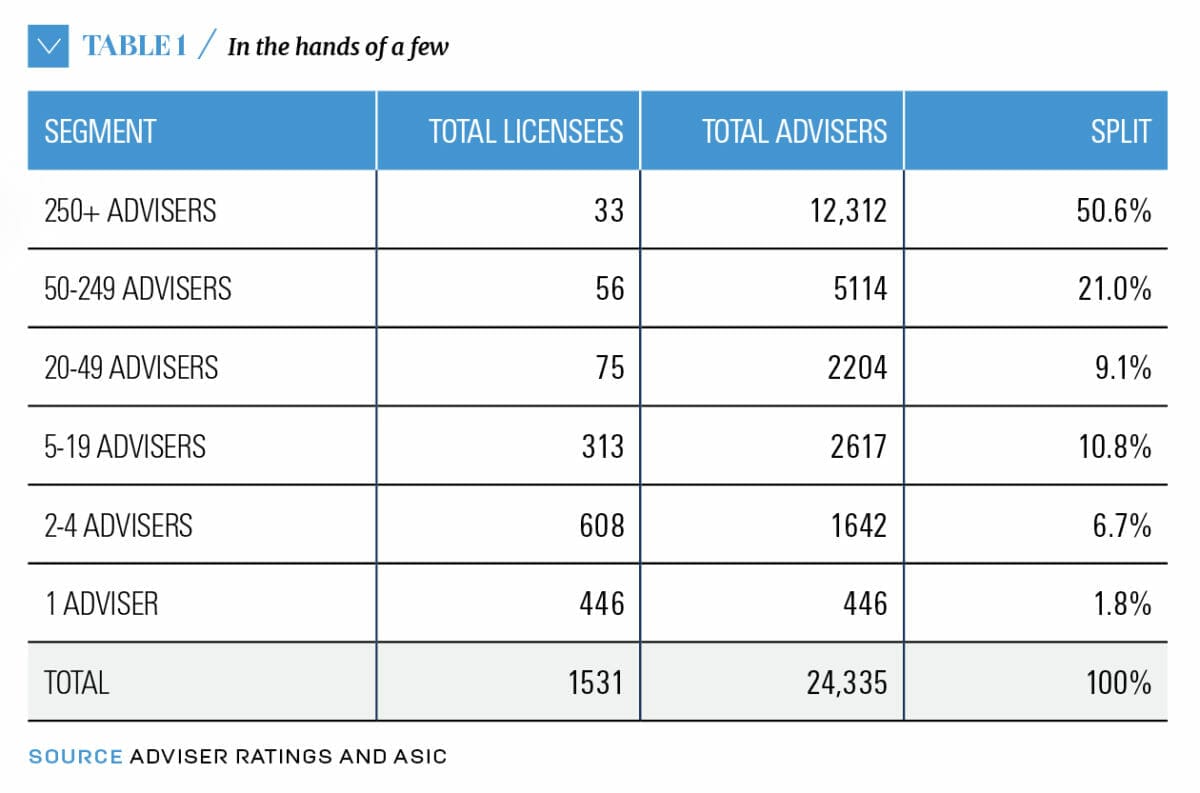

The financial planning industry remains heavily concentrated in relatively few hands, and if those hands fumble the ball, there is a disproportionate effect on the industry.

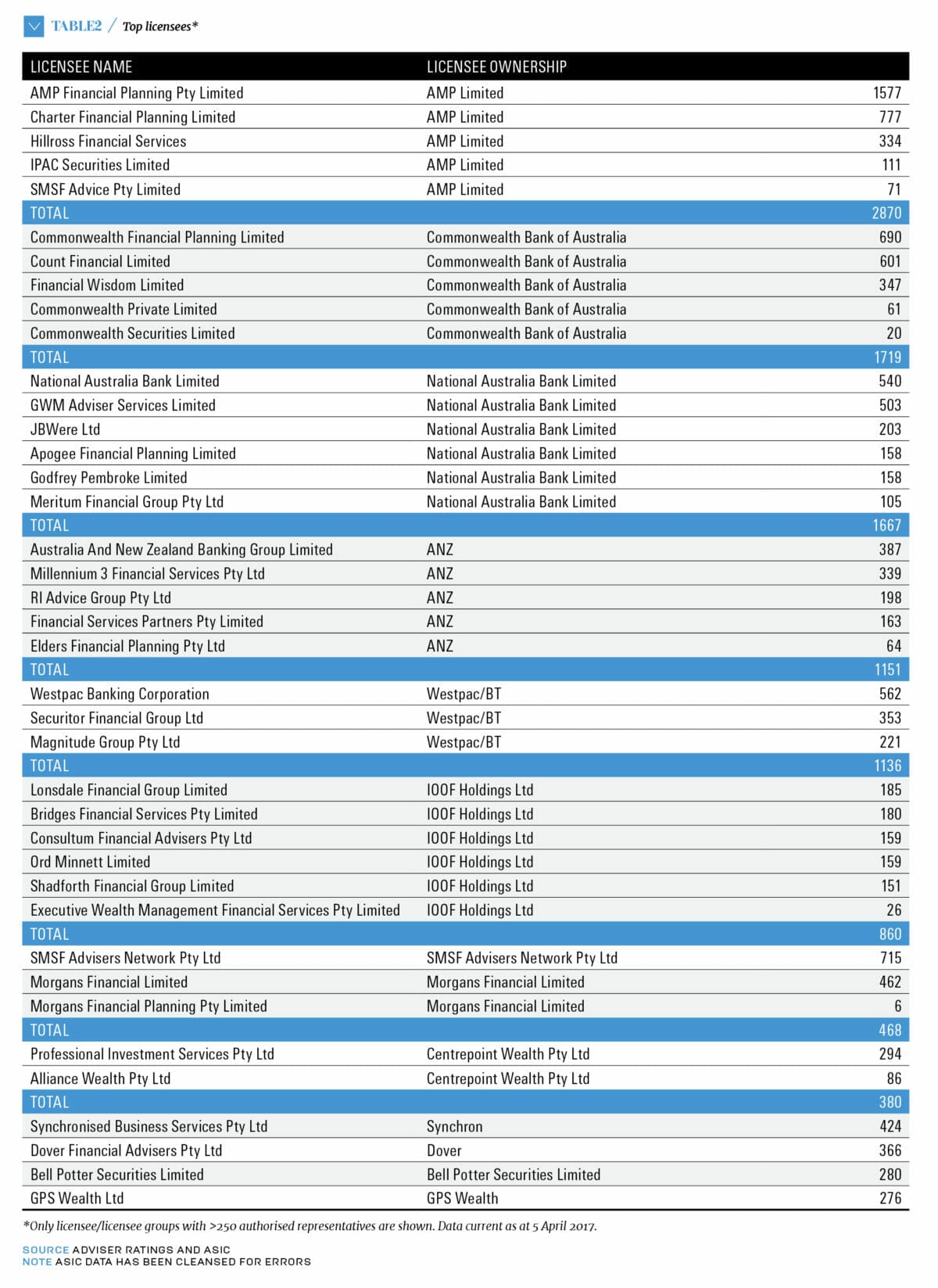

Data provided to Professional Planner by Adviser Ratings shows that as of April 5, 2017, more than half of all advisers on the ASIC financial advisers register were authorised by just 13 groups, controlling 33 licensee entities. Collectively, these groups had 12,312 representatives out of 24,335 on the ASIC register.

The largest single group, AMP, accounted for 2870 representatives across five licensee entities – more than 11 per cent of all financial planners in the country. The four major banks each had more than 1100 representatives, again split across multiple licensees, and collectively accounted for 5673 representatives – more than 20 per cent of all financial planners. IOOF sat just outside the top five, with 860 authorised representatives across six licensees.

For a full analysis of authorised representatives by licensee and ultimate licensee ownership, go here.

ASIC’s report states that the culture of licensee organisations is “very likely to have been a contributing factor” to compliance failures and breaches of the law.

“All of the institutions publicly state that their core values include being customer focused, ‘doing what is right’ for customers, and acting with integrity,” the report states. “Our concern is that, despite these stated values, many of the institutions we reviewed did not ensure that their internal processes consistently supported the value of ‘doing what is right’ for the customer.

Many of the failings we identified led, or had the potential to lead, to poor outcomes for customers.”

ASIC’s findings raise the issue of whether the current approach is a legitimate way to authorise individuals to give financial advice. There is a theoretical framework for testing the legitimacy of organisations, and whether their structures and activities are “desirable, proper, [and] appropriate within some socially constructed system of norms, values, beliefs and definitions”.

The framework was developed by US sociologist Mark Suchman and first applied to financial planning by Angelique McInnes and Abdullahi D. Ahmed, then both of RMIT University, in a paper published in the Financial Planning Research Journal.

The framework was developed by US sociologist Mark Suchman and first applied to financial planning by Angelique McInnes and Abdullahi D. Ahmed, then both of RMIT University, in a paper published in the Financial Planning Research Journal.

The conclusions of their pilot report aren’t encouraging. They found that the licensing of financial planners lacks legitimacy in several critical respects. However, they said further research was needed. McInnes, now a lecturer at Central Queensland University, is conducting that research as part of her PhD work. She says there are, broadly, three types of legitimacy: regulative, cultural-cognitive and normative (or moral).

In financial planning, regulative legitimacy is proven if the affiliation of planners with product providers does not lead to unintentional compliance breaches.

Cultural-cognitive legitimacy is proven if the Australian public can clearly distinguish between advisers defined as “independent” by the Corporations Act, and those who are not independent. Finally, normative or moral legitimacy is

proven if:

- Alignment to product issuers does not lead to commercial interests compromising advisers’ best interests duty.

- Affiliation to product issuers does not lead to sales procedures, standards and practices designed to reinforce product distribution while giving the appearance (window dressing) of satisfying regulatory requirements.

- Alignment to product issuers does not lead to conflicts of interest from association.

- Contributions by individual leaders of aligned licensees to the debate surrounding the licensing of advisers are not aimed at protecting their product distribution channels.

If those tests cannot be met, then the licensee structure arguably lacks legitimacy.

Within the context of financial planning, McInnes says, there has so far been little formalised study of licensee legitimacy, but her pilot study and the preliminary findings of her more detailed work suggest it is lacking.

Tom Reddacliff, a former managing director of NAB-owned licensee Godfrey Pembroke, says the current licensing structure means the public can never trust that the industry serves their interests rather than its own.

This masks the fact that “most financial planners I know have a passion and desire to make a difference to their clients’ lives, a truly noble cause of any profession”, Reddacliff says. “There are countless examples and case studies, which don’t get anything like the respect and recognition they deserve.”

The new standards will “clearly make a substantial impact on the journey to becoming a profession,” he says.

A paper Reddacliff has written suggests a new structure for financial planning regulation, in which the licensee – or a renamed version of that entity – continues to provide services to financial planners and their businesses, but the licensing aspect of

the relationship is removed.

Reddacliff argues this would put financial planning on a footing similar to other professions, where a licence to operate is granted by a body independent of the businesses in the profession.

“But financial planning has a structure like no other profession,” he says. “If you examine medicine, law, accounting, engineering and actuaries, you will observe none of them have a licensee structure or equivalent. Instead, the professional is either registered under the law, by entry standards, or by both. Other stakeholders in this approach are the professional associations and standards boards.”

McInnes supports this assertion.

“Doctors may prescribe certain pharmaceutical products they favour, but unlike financial advisers, they are not licensed to practise their craft through these pharmaceutical institutions,” she explains, in a discussion paper titled “Legitimacy of the current ‘authorised representative’ licensing model”.

“Indeed, lawyers, doctors and accountants work for corporate institutions, yet when they leave these institutions they retain their professional status – their ‘license’ to practise – and are able to work without being employed by other corporate institutions. This is not the case [with financial planners]. Instead, financial advisers are expected to recommend the financial products on their licensee’s approved product list.

“They are also licensed to practise through these licensees. Unlike other professionals, advisers lose their status and right to earn a living as a financial adviser when they leave their institutional licensee.”

FASEA emerges

FASEA emerges

A fundamental difference exists between financial planning today and during earlier calls for individual adviser licensing. That difference is FASEA. As an independent, standard-setting body, FASEA will play a central role in determining whether financial planners are fit – that is to say, appropriately qualified and trained – to practise. An individual’s right to practise would be contingent on adherence to the authority’s professional, ethical and educational standards, and it is easy to imagine

a scenario in which individuals could also be certified or authorised by FASEA to practise, irrespective and independently of their employer.

Reddacliff states that, under this approach, existing licensees would continue to play a vital role, but reconstituted as “registered advice groups”, or some other term, which “live or die on their value proposition to advisers, providing client-facing tools, support to run better businesses and supporting and fostering a strong professional culture”.

“Good quality groups will survive and thrive in this environment,” he states. “Their cost base and complexity to deliver services should fall and that benefits advisers and, in turn, consumers. Many readers might think this article will draw the ire

of the institutions. That’s not my mail; in fact, the groups with a strong proposition welcome these ideas. If your value proposition hinges on a licence, it’s sitting on a house of cards.”

Reddacliff says individual licensing raises issues that need to be addressed, including professional indemnity insurance and liability, the creation and use of approved product lists and product research, the ongoing role of ASIC in policing advisers’ compliance with the Corporations Act, and the need to ensure that advice businesses are not subsidised by advice support businesses linked to product issuers.

“Financial planning has some significant blockages in need of clearing,” he states. “Without repair, a professional model can’t exist.

Reddacliff adds that, “If the financial planning profession can’t get its act together and become a registered profession under the Professional Standards Councils, the model I’m proposing would be unworkable”.

The chief executive of the PSC, Deen Sanders, says he is hopeful that “the standards and ethical expectations set by FASEA will align to the national Professional Standards Legislation framework, so that at some point in the future the relevant occupations within financial services will be able to become genuine professions, recognised under our legislation”.

Reddacliff says individual licensing could also be an opportunity to introduce efficiencies for the regulator, financial planners themselves and the “registered advice groups” that support them.

“I consistently hear from large licensees they get more than a notice a week from ASIC for information,” Reddacliff says. “Everyone is losing. The regulator is expending considerable resources and time getting the data it needs to discharge its obligations; the licensee often has disparate and legacy operating systems, which means it’s drowning trying to meet the requests; and the adviser is copping it, constantly being asked to provide data in a manual and inefficient way.”

If ASIC requires data from a financial planning practice or practitioner, have them provide it to the regulator directly, Reddacliff says.

“This would introduce more data responsibility for advice businesses,” he argues. “However, you might start looking at the ‘registered advice groups’ for their value proposition in this area. It puts the advice group under value pressure, but advice businesses are in charge of the situation.”

Reddacliff says a move to individual adviser licensing, the formulation of licensees as “registered advice groups” and the use of technology to improve data flow and reporting would move “financial planning towards a true profession, earning the trust and respect it badly needs”.

“It is not good enough just to change the standards. The public needs to see an entire system they can understand and trust,” he says. “Exciting but important times are ahead. Let’s hope all the stakeholders have the courage to go the distance in making this into a true profession, as we all know the difference it can make to people’s lives.”

This is the beginning of a discussion about the future of financial planner licensing. To take part in the debate and have your say, go here.

Leave a Comment

You must be logged in to post a comment.