The risk profile of an asset – whether it is shares, bonds or property – is not static, but can vary dramatically from time-to-time depending on factors like the economy, underlying debt, and valuations.

An individual’s risk tolerance, on the other hand, is fairly stable for lengthy periods of time. While an investor’s ability to handle risk steadily declines as they near and enter retirement, it doesn’t swing widely.

That’s why traditional methods of portfolio construction that maintain a static strategic asset allocation are flawed, as they often leave investors exposed to variable degrees of risk, exacerbating client distress during market declines.

It’s critical for advisers to know and understand their clients’ maximum risk tolerance in order to dynamically and effectively manage portfolios within the acceptable parameters and deliver improved outcomes.

It also helps them to fulfil their fiduciary duty and protect against litigation.

According to the recently-released Financial Ombudsman Service (FOS) Annual Report, around two thirds of financial advice complaints received in the year to June 30, 2016, involved investment recommendations that failed to meet the client’s risk profile, objectives and goals.

Interestingly, the majority didn’t pertain to high-risk hedge funds and alternatives.

FOS found diversified funds that invested in multiple asset classes including cash, shares, bonds and property, accounted for 59 per cent of complaints about managed investment products. Inappropriate advice was the main issue with these products, followed by failure to follow instructions.

Monitoring portfolio risk

Risk profiling is a fundamental part of the advice process and advisers spend considerable time upfront determining a client’s tolerance to risk and then periodically reviewing it.

However, relatively little time is spent regularly reviewing the risk in a portfolio.

As a result, investors are commonly and unknowingly overexposed to risk, which is the antithesis of what risk profiling – and advice more broadly – aims to achieve. Risk profiling, as with advice in general, is trying to find the optimal level of investment risk a client can, and should, take to achieve their goals, and match them to an appropriate solution or portfolio.

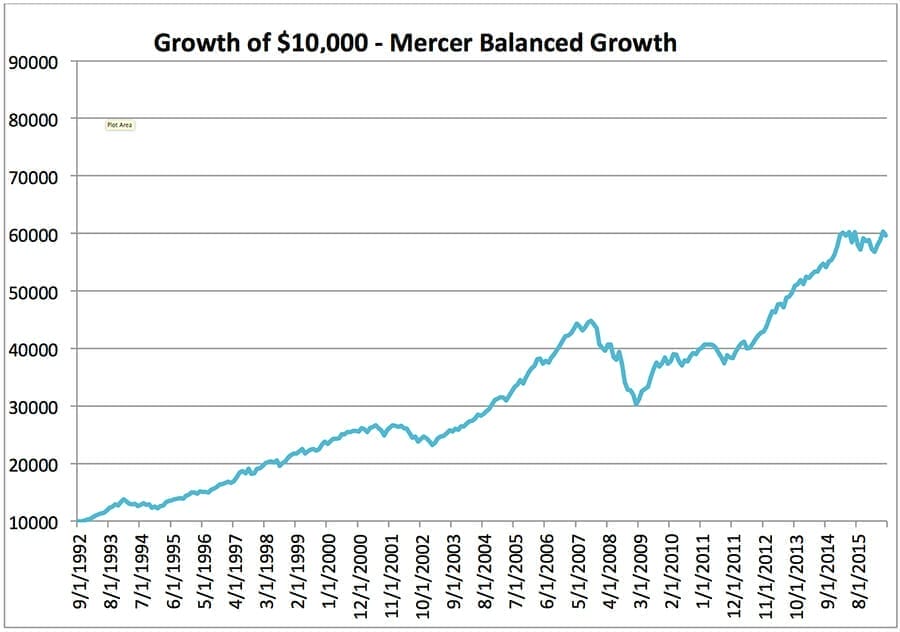

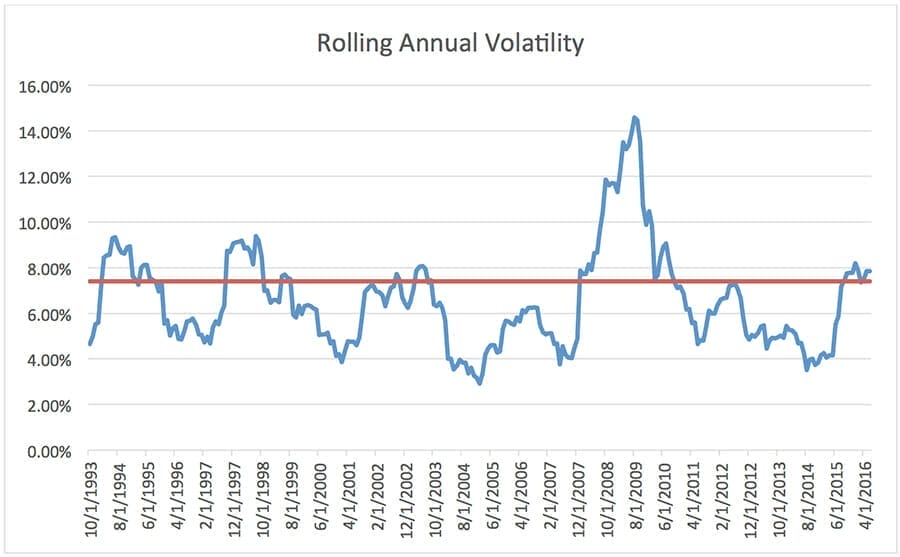

In the September edition of Portfolio Insights, we looked at the growth in value of a $10,000 investment in the S&P/ASX 200 Index. The following graphs show the growth in value of $10,000 in the Mercer Balanced Growth Index, and the Index’s rolling annual volatility, which is slightly under 7.5 per cent.

TABLE 1

Source: Mercer

Click to enlarge

TABLE 2

Source: Innova

Click to enlarge

Annualised volatility of 7.5 per cent is roughly the maximum risk a “balanced” client can tolerate, but as can be seen, volatility can vary drastically year-on-year even though it may smooth out over time.

As the graph above illustrates, the volatility of the Mercer Balanced Growth Index fell to around 3 per cent in 2005 and passed 14 per cent in 2008/09; almost double the maximum risk tolerance of the average “balanced” client.

This isn’t an isolated example. It’s common for volatility to fluctuate because most portfolio managers don’t have the mandate or flexibility (or skill) to actively adjust a portfolio’s asset allocation.

For investors, the problem with being overexposed to risk is that it’s uncomfortable, making them susceptible to behavioural biases. They can only handle a certain level of risk, so if markets wobble and risk blows out, they’ll almost certainly sell out at the wrong time.

Portfolio managers need to be agile and dynamic.

When the level of risk in a portfolio rises above an acceptable level, they should sell down risky assets in a timely manner. Conversely, if it falls below a certain level, they should lift their exposure to growth assets to maximise the probability of investors achieving their objectives.

It’s a proactive approach that requires diligence and skill to implement, but that’s what clients are paying for in the first place.

Leave a Comment

You must be logged in to post a comment.