Australia’s economy has had a remarkable run since the last recession in the early 1990s. But with the top 20 listed stocks offering poor growth prospects as our consumer debt levels set new records – not to mention some of the frightening statistics emanating out of Australia’s largest trading partner, China – many investors are considering diversifying their portfolios overseas in case the Aussie dollar sinks.

Having some overseas currency exposure makes sense for most Australians, as more and more people are travelling overseas as airfares fall. We’re also buying more overseas products as our local manufacturers are relocated or closed down, and online shopping is providing a much wider range of foreign products and brands with increasingly customer-friendly returns policies. In short, if you’re going to spend more money overseas, it makes sense to protect your purchasing power abroad with overseas investments.

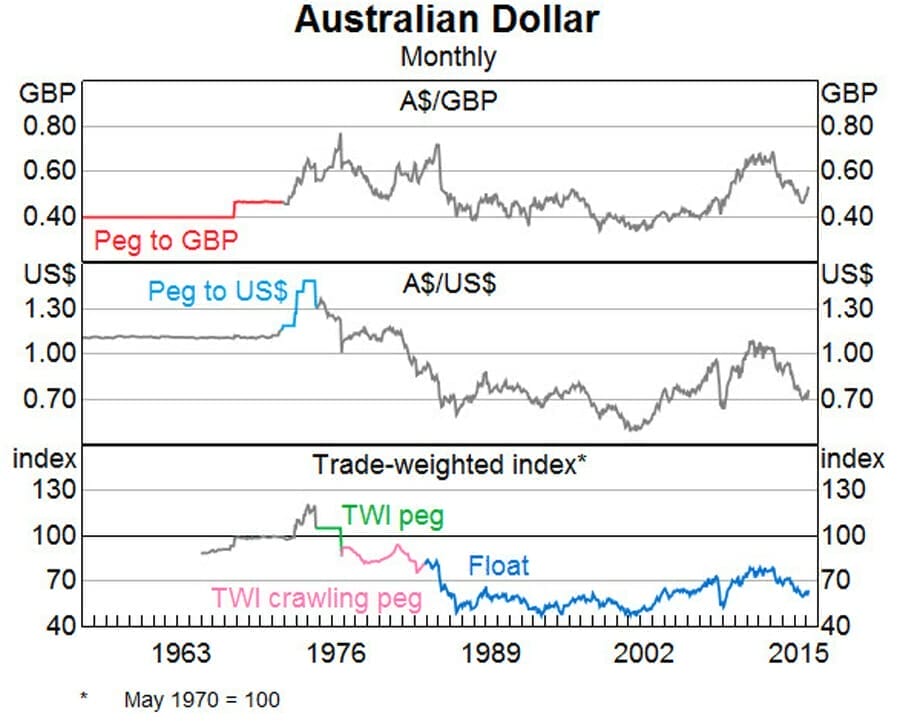

The problem is that while even the most stable currencies can swing around wildly in the short to medium term, over the long term the currency impact on your investments tends to wash out, as you can see from the chart below.

CHART 1

Click to enlarge

Click to enlarge

Currency impact on your investments tends to wash out

Source: Bloomberg, Global Financial Data, RBA, Thomson Reuters

If you’re a long-term investor that means the performance of your overseas stock portfolio will eventually reflect the performance of the individual stocks you buy. For those particularly worried about a housing crash in Australia, that might remove a major incentive for diversifying overseas. Fortunately, there are better reasons to revisit your overseas exposure as we round out another year. Let’s focus on two themes currently in our portfolio.

China

We recently made our first two investments in China, which most investors are avoiding due to reasons unrelated to the intrinsic value of what are some of the world’s fastest growing and most entrenched businesses. While we expect a major adjustment in the Chinese economy at some point (which is why we’ve hedged the currency), this pair of companies boasts large growth prospects regardless of any short-term macro fluctuations.

The first stock is Baidu, commonly referred to as the ‘Google of China’. The company has been under pressure since a student died after receiving experimental treatment that he discovered from an advertisement on one of Baidu’s websites. Earnings growth has stopped while Baidu increases its hurdles for advertisers due to more stringent regulation, but expects growth to resume next year. With founder and major shareholder Robin Li investing heavily in new services and plenty of cash on the balance sheet, paying 12x earnings for the online search business with an 80 per cent market share offers plenty of compensation for any short-term macro hiccups.

The second stock is JD.com, the ‘Amazon of China’, though there are some significant differences. JD’s founder and major shareholder Richard Liu is fanatical about timely delivery, offering same day delivery for most products if you order online before 11am. The delivery times of much larger rival Alibaba are measured in days, not hours, as JD has been willing to spend large sums on its delivery network, unlike Alibaba. Over time we expect more customers will gravitate to JD.com due to its unrivalled delivery times and increasing product range.

Broadband

A second theme in our portfolio is cable/broadband. Our largest investment is in Liberty Broadband, which is a holding company for a major shareholding in America’s second largest cable company Charter Communications (we own the Liberty entity as it offered a 12 per cent discount to buying Charter directly).

Last year you couldn’t open the Wall Street Journal without reading how traditional cable companies were dead in the water as more customers cut the cord in favour of cheaper online entertainment services, such as Netflix. Yet until more recently it went unmentioned that the cable companies also have monopolistic positions in the provision of broadband internet. It’s a superior business to cable, as the incremental cost of adding a broadband subscriber to the network is nominal and you’re not paying huge fees to content providers.

As the demand for online entertainment grows, so does the demand for fast internet services. By virtue of history, the wires laid to provide cable TV many years ago also happen to be the most efficient way to deliver high-speed internet services to the home, where the major competition is from mobile carriers that offer more expensive plans for an inferior service. Google has recently halted plans to deliver fibre services to many areas due to the massive cost of digging up sidewalks and unpredictable payback, showing how well the cable companies are positioned.

The beauty of being a contrarian global investor is that Brexit provided an opportunity to follow the same theme across Europe, via Liberty Global. The European market is quite different, with cable subscription prices and penetration rates much lower than in the US, for example, but the underlying investment idea is similar.

The key point behind these examples is that there are great businesses listed overseas that simply aren’t available in Australia and that, in contrast to our big banks and grocery retailers, have much greater growth prospects in the markets that they dominate regardless of any short-term macroeconomic headwinds.

Active vs passive

The father of value investing, Ben Graham, said, “in the short run, the market is a voting machine but in the long run, it is a weighing machine”. Right now, the ballot boxes are filled with votes for ETFs and other passive strategies that continue to buy more of the most popular and overpriced stocks. But eventually the market will reflect the intrinsic value of its constituents, and what’s been working well for investors for the past five or so years won’t be what works in the future.

Finding unloved or misunderstood businesses in the current environment is not easy, but there is always value somewhere in the world. Eventually the scales will tip back in favour of rationally valued assets, and those that have ignored the herds piling into passive strategies will be well placed to profit from the turmoil.

Disclosure: Peters MacGregor Capital Management holds a financial interest in Baidu, JD.com, Liberty Broadband and Liberty Global through various mandates where it acts as investment manager.

Leave a Comment

You must be logged in to post a comment.