Investors with a portfolio of top-20 Australian stocks have recently been asking where the growth has gone. Looking at global gross domestic product (GDP) figures you’d be forgiven for thinking that there isn’t any growth anywhere. At least not that’s available at an attractive price, given the current high valuations for stocks offering seemingly predictable earnings growth or yield.

The value of investing outside Australia is that you’re more likely to find industries with plenty of growth ahead. Even better, occasionally you can play the same trend several times in different countries to make the most of your insights. If an industry has matured in the US, perhaps it’s still in its infancy elsewhere.

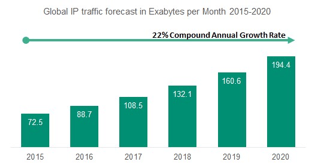

A current theme running through our portfolio is the rapid growth in broadband usage (see chart 1). Our first investment came via Liberty Broadband in February, which fortuitously coincided with the low in the general market.

CHART 1

Global broadband usage forecast

Source: Cisco

Liberty Broadband is one of many Liberty stocks listed on the US market, where the common denominator is cable industry legend John Malone, who is a major shareholder and chairman. Liberty Broadband is a holding company whose primary asset is a shareholding in Charter Communications.

The case for Liberty Broadband was that you got a 12 per cent discount to buying Charter Communications directly. The case for Charter was that it was about to become the second largest cable company in the US, once regulators agreed to the acquisition of Time Warner Cable, which Charter chief executive Tom Rutledge had led in the past.

Once Rutledge was in charge of the combined entity, he would strip nearly a billion dollars in costs and potentially increase subscription prices as Time Warner Cable subscribers upgraded to Charter’s superior service.

Despite fears that online competition such as Netflix would destroy the economics of the traditional cable bundle, we believed Charter’s triple bundle (home phone, cable and broadband) would be less impacted than the single offerings of other providers, such as satellite TV providers, for example.

Most importantly, we believed as online entertainment grew more popular, broadband subscriptions would increase along with Charter’s profit margins, due to the nominal cost of adding a broadband customer to the network.

Brexit brings opportunity

So far the stock has performed better than we could have hoped in such a short period, but there were more ways to play the same theme. The Brexit vote and some company-specific news caused the share price of Liberty Global (essentially the European version of Liberty Broadband) to fall, creating an opportunity.

Some differences in the European cable industry include stronger competition from telecommunications companies. Over time we expect consolidation between the two industries, with a mooted tie up between Liberty Global and Vodafone potentially making sense. Profit margins are also often higher, as European cable companies don’t spend as much on content as US cable companies.

Liberty Global also has first class assets in Latin America. Broadband and cable penetration rates are much lower than in the West, providing plenty of room for growth. This was also a safe way to get exposure to potentially faster growing markets, as Liberty Global comes with Western management that believes in investing for the long term and returning capital to shareholders when it’s appropriate.

Need to be opportunistic

While this article has focused on a particular investment theme, the broader implications are just as important for any investor searching for safe ways to grow their wealth, while asset prices across the board are inflated by low interest rates.

First, there are plenty of industries and geographies that will grow for a very long time to come. The biggest step that most Australian investors need to make is to look beyond our beautiful shores.

Second, you need to be opportunistic. To make these investments we took advantage of the market’s scepticism that Charter and Time Warner Cable would be allowed to merge, and the fact that the media was obsessed with calling the downfall of cable companies without acknowledging that their broadband businesses would pick up the slack.

Without these negative views, we would never have been able to buy cheaply, and we note the media reporting has since turned 180 degrees. Brexit also helped provide the chance in Liberty Global, showing that one man’s crisis is another’s opportunity.

Third, having entrepreneurial management is worth its weight in gold, particularly in a slow growth environment. Tom Rutledge is widely acknowledged as the best in the business, and Charter’s (and Liberty Broadband’s) share price reflects the market’s confidence in him.

Unpredictable acquisitions

Although we no longer own it, the surge in Liberty Media’s share price after recently buying the Formula 1 franchise is further proof. You couldn’t predict the acquisition, and therefore couldn’t forecast it in a discounted cash flow model. But if you invest in great managers, they can create more value than you can predict, proving that investment, like business, is as much art as science.

It’s never been easier to invest overseas, but you have to know where to look. Particularly when valuations are so high across the board. The other benefit of investing in predictable businesses with top-notch management is that they can use downturns to improve their market position.

If you own these types of situations, that should provide you with plenty of comfort, as no matter what the macro environment, your management teams and businesses will be busy creating value.

Disclosure: Peters MacGregor Capital Management Limited holds a financial interest in Liberty Broadband and Liberty Global through various mandates where it acts as investment manager.

Leave a Comment

You must be logged in to post a comment.