My SMSF equity portfolio is coming up for an annual rebalance. I would have done a mid-year rebalance in May 2016 had the horizon for high-yield stocks been clearer. On November 2, 2015 I chose to allocate half of my equity exposure to a high-conviction portfolio and half to what I call a “hybrid-yield” portfolio – which is a dynamic mix of conviction stocks across the spectrum, but with a very strong tilt towards yield. In November I was already leaning away from yield but not quite ready to abandon it.

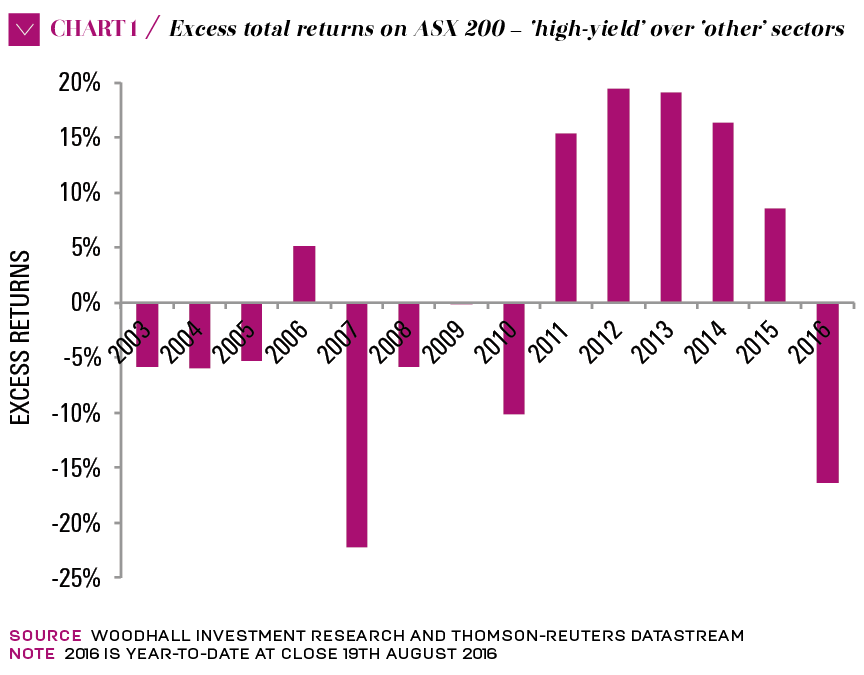

In Chart 1 (below), I show an update of a chart I published here last year. After four stellar years (2011 – 2014) of the composite “high-yield sectors” (financials, property, telcos and utilities) over the “other” seven sectors, the pure high-yield play started to wane in 2015.

The year 2016 to date has been a disaster for the pure high-yield play as can be seen from the last bar in Chart 1. High-yield sectors collectively returned 0 per cent while “other” returned plus 16.4 per cent (both including dividends) making a minus 16.4 per cent excess total return.

Over the same period, the ASX 200 returned plus 7.2 per cent while my composite portfolio returned plus 11.5 per cent.

Going backwards

These performance results show that the capital losses in the high-yield sectors erased the entire yield component in 2016. After tax and inflation, such a play went backwards.

My portfolio did not suffer as badly from the high-yield results because my hybrid-yield version of yield includes stocks from ‘other’ sectors, providing the relative risk-return forecasts warrant it, and the yields are reasonable.

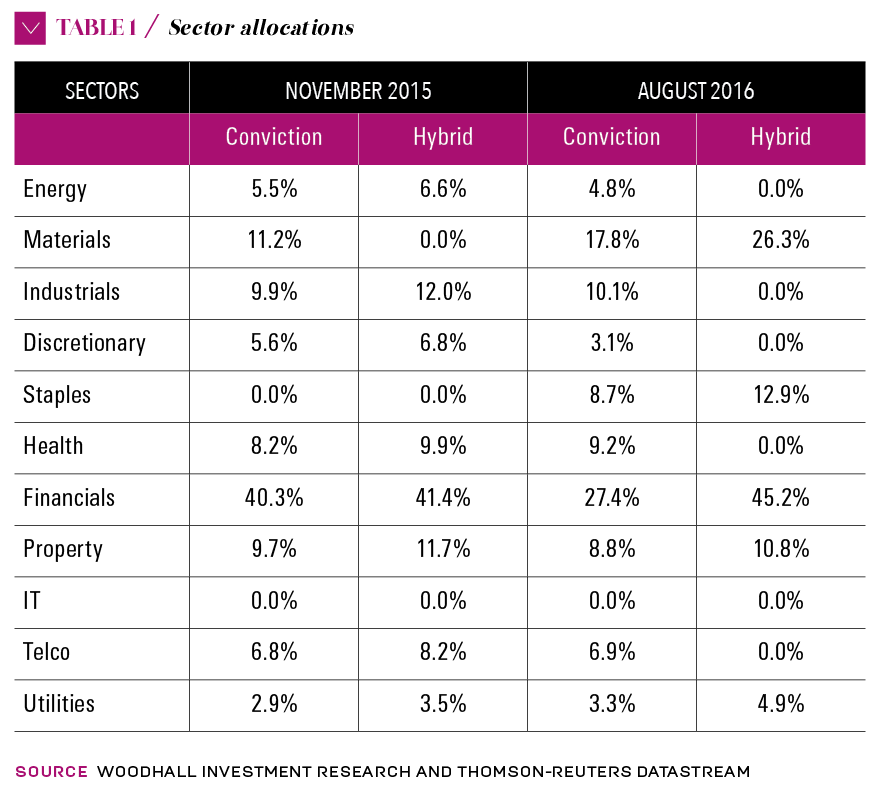

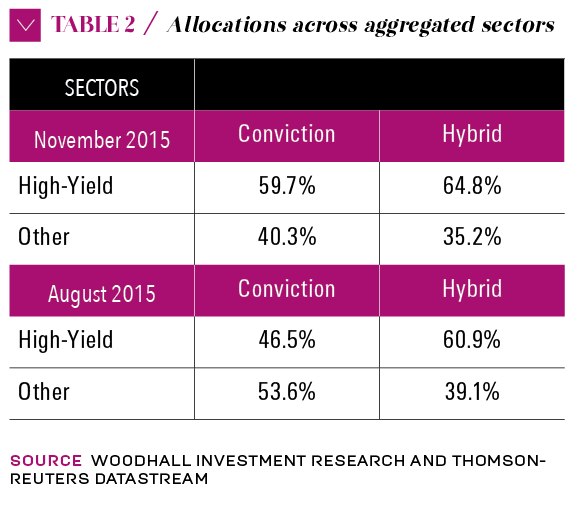

I show the allocations at the start of the period in the left panel in Table 1 (below) which are aggregated into high-yield sectors and ‘other’ in Table 2 (below).

As it turned out, there was not a great difference between the conviction and hybrid portfolio allocations in late last year. It so happened that the allocations to financials (that contain the big four banks) were remarkably similar.

Indeed, from Table 2, there is only about a five percentage point additional allocation to the High-Yield sectors in the Hybrid portfolio (5.1 per cent = 64.8 per cent – 59.7 per cent). Of course, the stocks within each sector may be different and were.

I am not convinced about a possible bounce back in the performance of the high-yield sectors. My calculations based on broker forecasts show an expected plus 6.4 per cent capital gain for high-yield over 13.5 per cent for ‘other’ over the next 12 months – and that includes a compensation for a current plus 3.3 per cent over-pricing in ‘other’.

The expected yield on high-yield is 5.8 per cent compared to 2.8 per cent on other.

Out of hybrid portfolio

When I compare the November 2015 allocations to the latest from August 1, 2016 in Tables 1 and 2, there has been a distinct shift away from financials and high-yield in aggregate for the conviction portfolio – the hybrid portfolio is constrained to at least be market weight in each of the four high-yield sectors, providing sufficient quality stocks can be found.

Telcos didn’t get any allocation in the latest hybrid portfolio because the consensus recommendations didn’t pass muster! The expected yield for the hybrid portfolio is 5.6 per cent while it is 3.6 per cent for the conviction.

On this basis, I am now going to sell out of my hybrid portfolio and into a rebalanced conviction portfolio as soon as the impact of reporting season seems to have settled down. But whichever way you slice and dice it there is no point in sticking with a pure yield play if capital losses are likely to swamp that yield – as they have in seven of the last 14 years (Chart 1).

CHART 1

TABLE 1

TABLE 2

Leave a Comment

You must be logged in to post a comment.