Year-on-year underlying global dividend growth slowed to 1.2% at the end of the second quarter of 2016, down from the 3.1% underlying growth in the first quarter, putting further pressure on Australian investors searching for steady income to boost portfolio returns.

The latest Henderson Global Dividend Index out today reinforced the need for Australian investors to seek income in offshore markets as Australian equities continued to produce flat dividends.

Dividends in Australia fell just -0.2% on an underlying basis. The largest payer, Commonwealth Bank, held its payout steady, while retailer Woolworths made a steep cut.

Each year Henderson analyses dividends paid by the 1,200 largest firms by market capitalisation. Key highlights from the latest quarterly survey include:

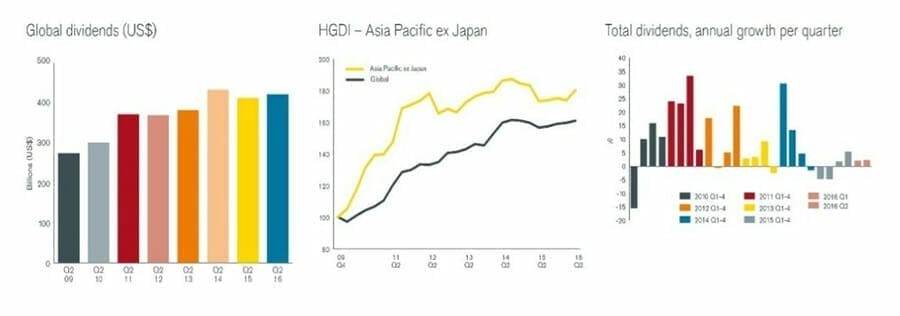

• Global dividends rose in underlying terms by 1.2% year on year to $421.6bn

• US engine of global dividends decelerated to slowest growth since 2013, partly thanks to the stronger dollar

• Europe saw broad-based, encouraging growth year on year – Q2 saw two thirds of Europe’s dividends

• Dividends in Australia are flat, while South Korea tops the global growth tables

• The strong yen has impacted corporate profits and Japanese dividend growth, though in dollars, Japanese dividends rose strongly

• H2 set to be slightly weaker than H1, as slower growing regions make up a larger share of the total

Overall, global dividends rose 2.3% on a headline basis, reaching $421.6bn, an increase of $9.7bn year on year.

The slowed growth for the quarter partly reflected Q2 seasonal patterns that give greater weight to slower growing parts of the world, and partly owing to a more muted performance from the United States.

US dividend growth of 4.6% on an underlying basis was the slowest since 2013, reflecting subdued profit expansion, partly due to the impact of a strong dollar. This US slowdown began late last year but should be considered a normalisation to more sustainable levels of dividend growth after several quarters of double digit increases.

Source: Henderson Global Investors as at 30 June 2016

The second quarter is seasonally important in Asia Pacific ex Japan, particularly in Hong Kong and South Korea. Total dividends of $36.9bn were 12.2% higher year on year, and were boosted by some large timing effects in Hong Kong. In underlying terms, growth was 3.7%.

On an underlying basis, Hong Kong’s dividends fell 2.4%, with cuts at China Mobile making the biggest impact. Meanwhile in Singapore, United Overseas Bank sharply reduced its Q2 payout. South Korea stood out, with dividends up by a third, the fastest growth rate in the world during the quarter. This reflected a huge fivefold increase from Korea Electric. Most other Korean companies modestly increased their payouts.

Elsewhere in the world, Japanese dividend growth was 28.8% in headline terms, but most of this increase was due to the strength of the Japanese currency. In underlying terms, Japanese dividends fell 0.8% as company earnings were depressed by this same factor. Toyota Motor was a case in point, reducing its final dividend by 12% in yen terms. Dividends in emerging markets fell sharply year on year, and were down in the UK too.

The second half of the year is likely to be weaker than the first, partly because seasonal patterns mean the emphasis shifts slightly towards those parts of the world where dividends are growing more slowly, like Australia, the UK and emerging markets.

Two thirds of European dividends are paid during second quarter, making the region’s payouts much more seasonal than those elsewhere in the world. In fact, European dividends of $140.2bn made up two-fifths of the global Q2 total. They were 1.1% higher than Q2 2015 on a headline basis. Underlying growth was an impressive 4.1%, however, once lower special dividends, as well as other more minor factors were taken into account. The Netherlands and France had the second and third fastest dividend growth in the world on an underlying basis, while Germany and Spain lagged behind owing to very large dividend cuts from Deutsche Bank, Volkswagen and Santander. Over four fifths of European companies held or raised their dividends year on year.

As a result of the Q2 trends, Henderson has reduced its forecast for the full year to $1.16 trillion, down from $1.18 trillion. This is equivalent to a headline expansion of 1.1%, or 1.4% on an underlying basis.

Alex Crooke, Head of Global Equity Income at Henderson Global Investors said:

“Encouraging growth in Europe is helping to balance the global picture for dividends. Any weak spots in the region have been company-driven, or owing to specific sector trends like the impact of lower commodity prices, rather than related to wider economic difficulties. The slowdown in US dividend growth is not a cause for concern. It began late last year but should be considered a normalisation to more sustainable levels of dividend growth after several quarters of double digit increases.

“In Asia, China’s slowdown is certainly having an impact on Australia, Hong Kong and Singapore, but China is performing better than many emerging markets so the impact is relatively muted.

“The Brexit vote in the UK has brought a devaluation in the pound. That will reduce the UK’s share of the global dividend total, but the impact will be less severe than the pound’s fall might suggest, as the UK’s largest companies are very international, and many pay in dollars.

“Thinking globally for income really helps investors reduce their reliance on any one part of the world, providing more stable dividend growth over time than any one country could normally muster.”

Source: Henderson Global Investors as at 30 June 2016

Leave a Comment

You must be logged in to post a comment.