You probably all know that the “Life is short. Have an affair” website, Ashley Madison, was hacked recently, revealing to the world the names and email addresses of millions of people who had paid their money and registered their intention they wanted find someone other than their wife or husband to finagle with.

Like me, you were probably amused but not surprised by the sheer volume of people and the number of (mostly American) public figures who had decided that finding a sneaky significant other was something that they would trust to the internet.

What the hack proved was something that we all know: relationships, especially long-term relationships, are hard; they require work; and they require a kind of constant improvement that is hard to master.

The big relationship in Australian financial services – the marriage if you like – is between financial planners and their licensee, and the health of those relationships is a critical indicator of the health of the industry and the health of the businesses in it.

Here’s the thing with economists and relationships: As soon as we see a relationship which creates value, we try to measure it. We try to measure it for a few reasons. One of the reasons is that economics and research long to be real sciences, which are empirical and logical and mechanistic, and all the inputs can be measured in outputs. (They can’t by the way – and anyone who tells you different about economics or research is trying to sell you something.)

But it is a useful way of grouping things, people and businesses. In a bid to make this sound important, researchers and economists tend to call these groups “cohorts” – which is just a fancy way of saying “a group with shared characteristics”.

There can be only four

In any case, the behavioural research shows that when you are looking at relationships you end up with four broad groups: Those that hate you; those that have a transactional relationship with you; those that have a preference for you; and those that are loyal.

That’s it. Those are the only groups. If you are a licensee, then everyone who is part of your licence falls into one of those groups, and at CoreData we’ve been measuring those groups for the past 13 years.

Let me explain the groups briefly:

- Those that hate you are leaving you. They are now looking for the way out.

- Those that are transactional are only there for the transaction. If a better offer comes along, they will leave, because they only measure the relationship in what they can get out of it. And they think you are doing the same.

- Partners that have a preference for you are likely to think that you are pretty good at what you do and somewhat interested in their happiness.

- The loyal have bought into your vision, what you are trying to do and think that you are very interested in their happiness and success.

It’s that simple.

The big mistake that most licensees make is that they think that the advisers who are with them that have transactional relationships have at least a preference for them, or are loyal. They aren’t; they are simply with their licensee until a better offer comes along.

And the bad news for the licensee industry is that the number of businesses in the transactional relationship group is up year-on-year.

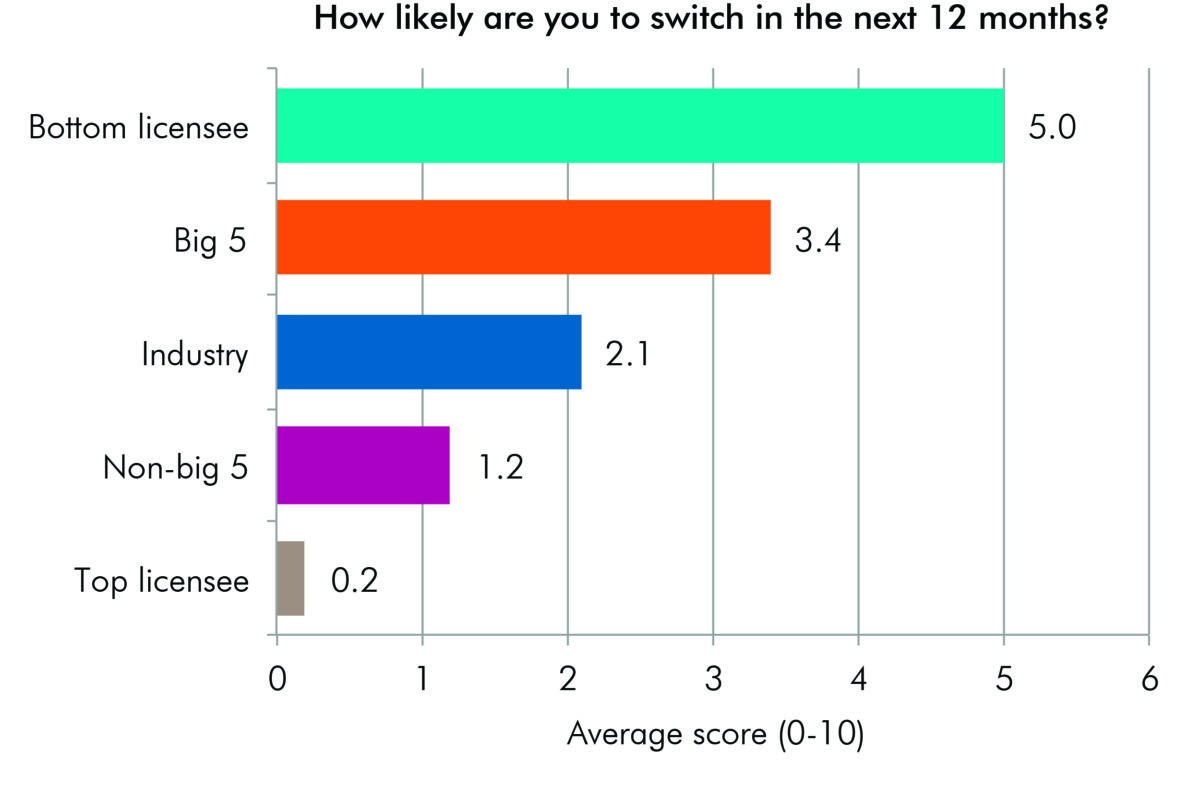

For the big licensees, particularly the bank-aligned ones, more than a quarter of the advisers state that they would like to leave them within the next 12 months. Those are the ones that hate their license.

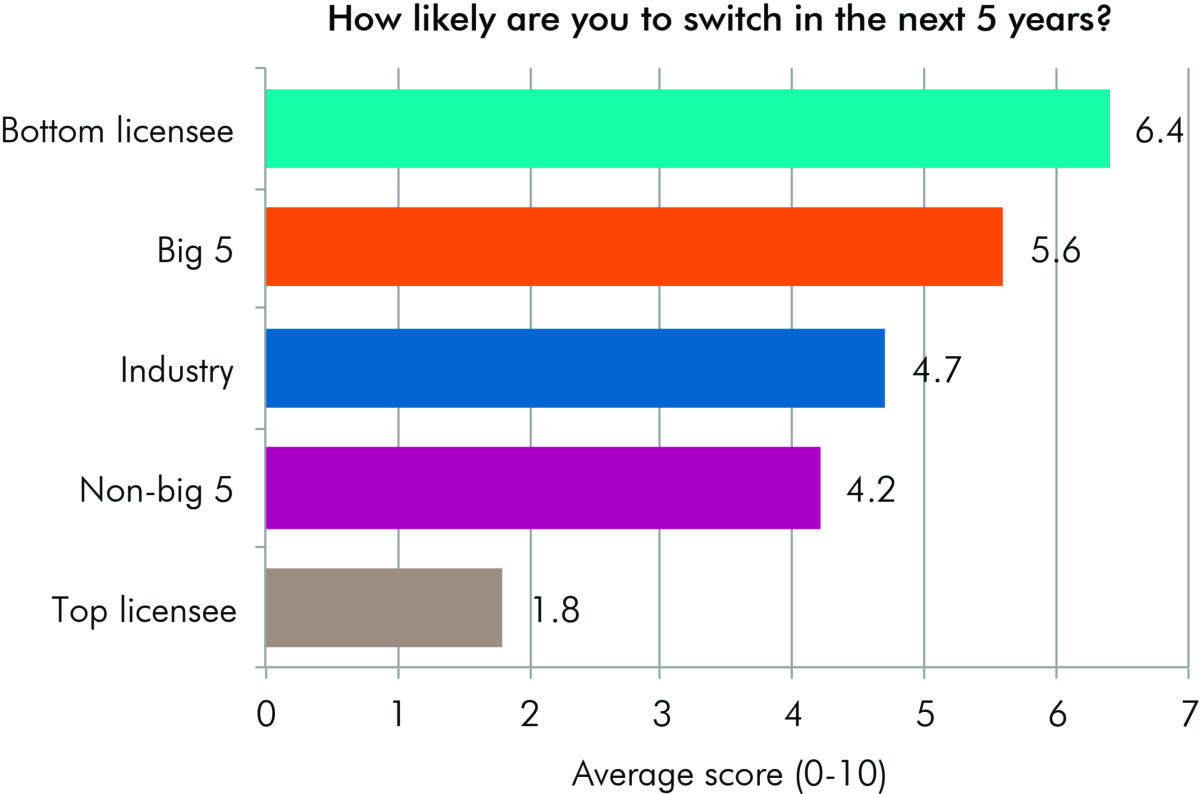

The news gets worse as you push the time frame out, with a further 40 per cent of the advisers stating that they would like to leave within the next five years, those are the ones that are in a transactional relationship. (Click on the charts to enlarge them.)

Obviously not all of the brands are equal. CBA has the most loyal and happiest advisers, frankly outperforming a decent number of the smaller, supposedly more intimate licensees.

Think about that for a second. CBA, the beleaguered giant, has a loyal and predisposed adviser base. Imagine what they could do once they start to unleash that machine. Imagine the power they have to transform the industry.

But for most of the big licensees and some of the small ones these findings reflect a broader picture among advisers in bank-aligned licensees in that they tend to be less satisfied, be less likely to recommend their licensee and be more likely to switch to a new licensee.

The hidden driver of change

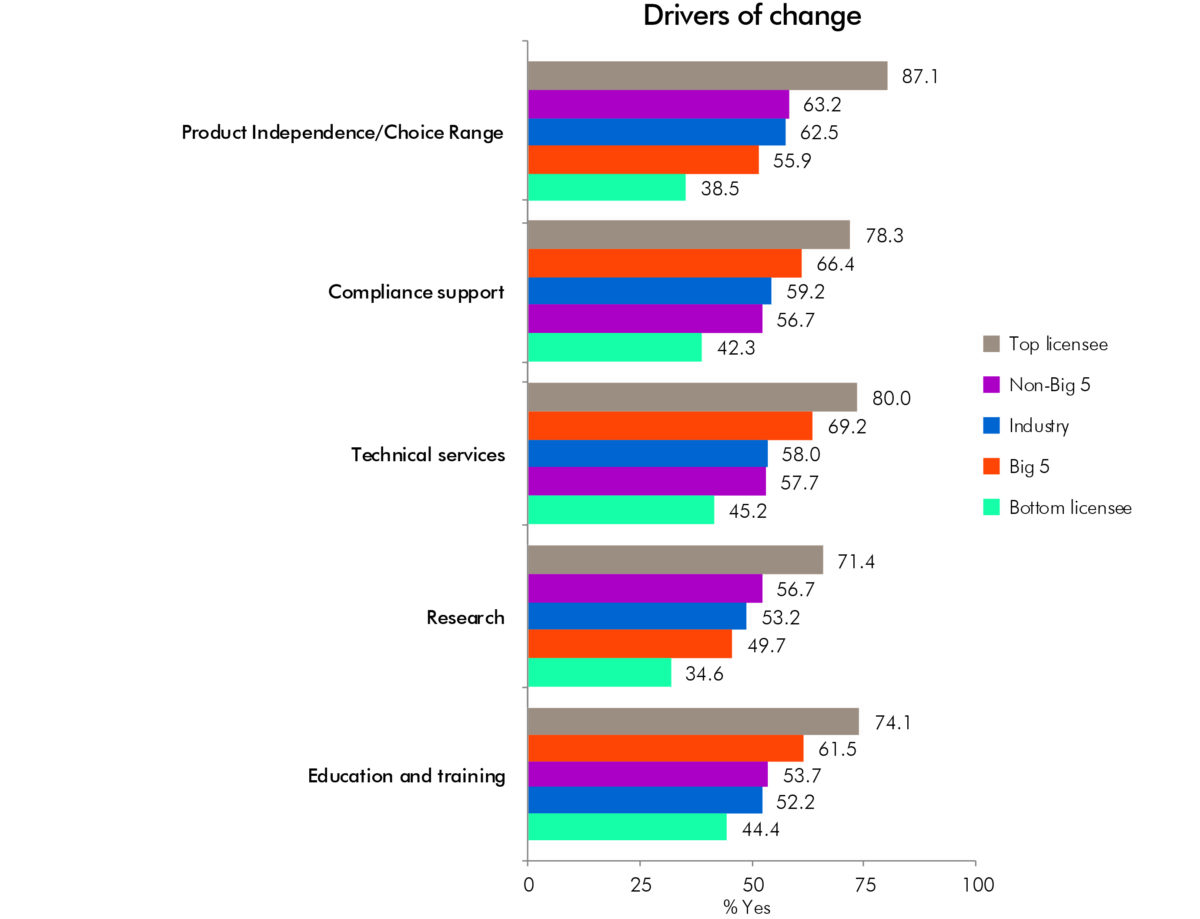

Every year when we do the research we pick up subtle shifts in the satisfaction drivers of the advisers – clues to what is really at work on their concerns for their business. This year the shift wasn’t subtle at all.

A technique almost every decent researcher employs is to design a survey to look beyond “stated preference” for real preference. For example a stated preference is something which is a politically correct or an acceptable preference – like saying you bought the top-of-the-class Mercedes Benz because it has high re-sale value or has great safety. Maybe you did. But maybe you bought it because it’s great deal of fun to drive and lets everyone know that you’ve got a lot of money.

So in this year’s survey we were looking at what would drive advisers to change practice and expected to yet again find that product independence and remuneration were fighting for number one and two slots. The surprise is that that they weren’t. Now, the biggest driver of change is technical expertise, then product independence, then remuneration.

In the past, getting an adviser to move was simple: pay more. Dangle a cheque and better income, and they would move.

In a change – which is frankly nothing short of admirable – that doesn’t really work any more. If you want to get an adviser to switch now, how much you pay them is only the third-most important thing. Turns out it’s now the advisers leading the licensees in terms of real change, which means the economic drivers in the industry have changed.

It seems a chequebook is no longer going to be enough to get the good advisers. You are going to have to be technically strong, have a flexible and open APL, and pay well.

Leave a Comment

You must be logged in to post a comment.