Listed investment companies (LICs) have long been a popular way for investors to access a managed portfolio in a format that is simple, familiar, transparent and often relatively cheap, compared to accessing managed funds via investment platforms.

The added lure of high franking levels for retirees – in an environment where the yield trade dominates and cash and term deposits (TDs) cannot support their income requirements – is driving income-seekers to bid up prices across a wide range of yield-oriented assets.

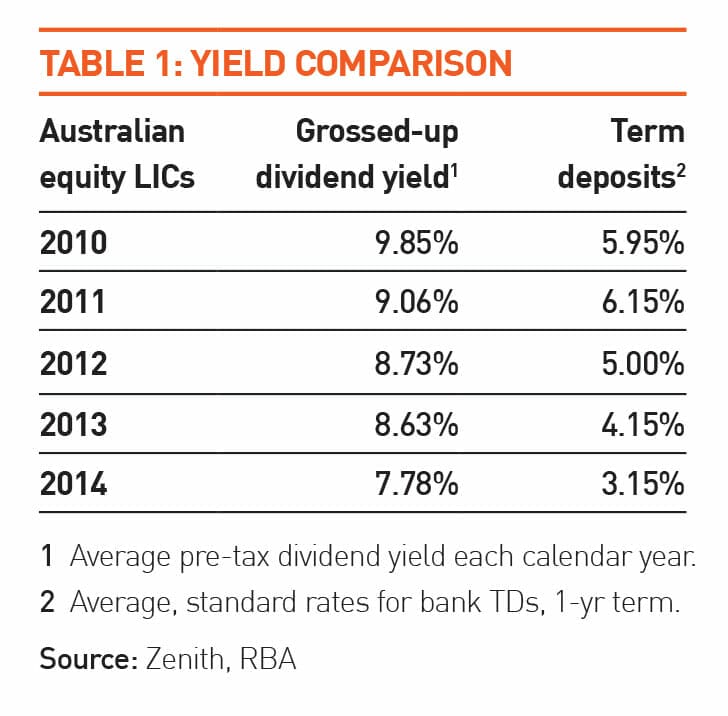

Yield compression continues apace, with LICs being no exception – although we note that the margin they offer over TDs has widened rapidly over the past three years (see Table 1).

Bull market for LICs continues

LICs have been a natural beneficiary of the yield trade, and with good reason. With an increasing range of choice of asset classes and strategies, as well as several high-profile, quality fund managers broadening their distribution strategies to more easily accommodate direct investors, LIC investors have more choice than ever. Benefits from a structural and taxation perspective mean that the lure of relatively stable dividends (in comparison to managed fund structures), reinforces their usefulness for income-seekers.

In response to demand, and as something of a self-fulfilling prophecy, capital flows into the sector have followed the increased level of interest evidenced in previous years, with the number of new vehicles launched reaching a decade-long high in terms of both entrants and capital raised.

In response to demand, and as something of a self-fulfilling prophecy, capital flows into the sector have followed the increased level of interest evidenced in previous years, with the number of new vehicles launched reaching a decade-long high in terms of both entrants and capital raised.

Calendar 2014 has seen a significant uplift on the previous year, with $1.1 billion raised across 12 new LICs versus $297 million across four initial public offerings (IPOs) for 2013. In addition to new vehicles, existing LICs continued to take advantage of buoyant market conditions to raise additional capital, with $530 million raised during 2014 via various placements and share purchase plans. Investors have also joined the party, with $130 million in options being exercised.

Storm clouds gathering?

However, investors need to remember that the outcomes for LICs are driven not only by the skill of the portfolio managers, but the behaviour of investors themselves and the broader market.

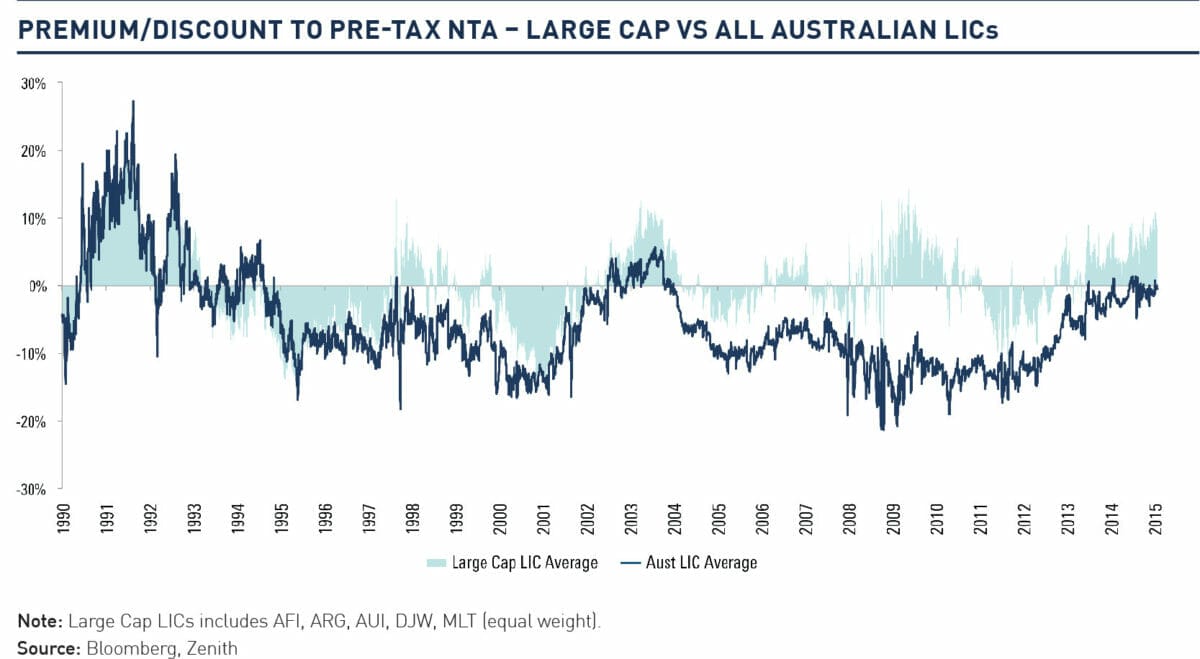

Combined with strong equity market returns, the yield-seeking behaviour from investors has continued to drive rising premiums and narrowing discounts in LIC share prices versus their net tangible assets (NTA). As shown in the accompanying chart (click to enlarge), Zenith measures the Australian market’s most significant LICs (based on the greatest market cap and longest operating history) as a proxy for sector sentiment, using share price versus pre-tax NTA.

As a secondary comparison, we have shown the average across all Australian equity LICs.

As a secondary comparison, we have shown the average across all Australian equity LICs.

This long-term data series clearly highlights the cyclicality of investor behaviour in LICs, as well as providing evidence that the sector as a whole (that is, not just the largest, most liquid participants), has a prevailing tendency to trade at a discount. Notwithstanding individual drivers of results, which can be impacted by a range of factors (sentiment, performance, management/fees, size/liquidity et cetera), this should highlight the potential risks of purchasing LICs at a premium.

Overwhelmingly, LIC investors appear to be overly sanguine to value signals at present (a symptom also being exhibited with A-REIT investors, where similar behaviour is being exhibited). Despite frequent debate as to whether the cause is structural (the classic “new normal”) or more a function of behavioural finance and momentum, this is a dangerous time for LIC investors.

While there are several arguments to suggest that a “re-rating” of LICs is justified, Zenith believes that such enthusiasm is usually always dampened by the appearance of the next crisis. Therefore, while the current buoyant conditions provide an opportunity, significant caution is warranted.

Although signals have been generally bullish, year-on-year positive movements in the premium/discount numbers across the sector appear to be losing momentum. In the periods 2012-2013 and 2013-2014, 77 per cent and 75 per cent of all equities LICs respectively (by number) experienced either a narrowing of discounts, or increases in their premium to pre-tax NTA. Calendar 2014-2015, however, saw this figure fall to 51 per cent of LICs experiencing positive movements.

Exhibit caution

Whether this represents investor fatigue, arising from a surge in new vehicles entering the market, or is a rational response to an over-valuation signal is difficult to determine. However, it reinforces our view that investors should exhibit caution if purchasing LICs at a premium. While some LICs sometimes break the mould and may sustain premiums for prolonged periods, history both here and overseas would suggest that this is unlikely to be permanent.

Ultimately, whilst Zenith remains supportive of the investment talents that stand behind those considered to be quality offerings in the LIC sector, we remain circumspect of entering a market where premiums are becoming endemic. While we have always advocated a “through-the-cycle” approach to investment decisions and portfolio construction, this only makes sense if investors are paying a reasonable price. As with other sectors of the market, the pursuit of yield at any cost is unlikely to be a journey that has a happy ending.