In its last two Budgets the Federal Government proposed a number of measures directed at improving the sustainability of age pension provision. Central to its current solution is a redesign of the assets test which involves a return to the 7.8 per cent taper rate which existed before 2007.

While the harsher taper rate will, if enacted, reduce Government expenditure substantially over time, it poses a strategic dilemma for clients whose age pension entitlements are affected by it. Before 2007, we used to call this the assets test “black hole”.

This article briefly outlines developments in the Government’s approach to age pension eligibility over the last 12 months or so, and explores the options for clients caught in the black hole.

2015 reverses out 2014

In the 2014 Budget, the Government proposed an effective reduction in the indexation of the age pension, a reduction in the income test deeming rate thresholds, a freeze on the indexation of the income test free area and a staged increase in the pension eligibility age to 70. There were no pensioner winners from these measures. In the 2015 Budget, the Government has announced it will not pursue the first three of these measures. The fourth, the eligibility age increase, is still in the House of Representatives. Instead, the Government proposes two key measures:

1. an increase of the ‘asset free area’ for homeowners, with the relevant asset free area for non-homeowners pegged at $200,000 more than homeowners

2. an increase in the asset test taper rate from $1.50 to $3.00 per fortnight for every $1000 of assets above the minimum threshold for a full pension. This is the 7.8 per cent taper rate referred to as the black hole.

The first measure is expected to increase the age pension for around 170,000 retirees. The second is expected to reduce the pensions of 235,000 retirees and disentitle a further 91,000 from the age pension. (The latter group would retain entitlement to the Commonwealth Seniors Health Card – although it’s not clear whether that would be a permanent right – but could lose entitlement to state-based pensioner concessions.) So the 2015 proposals would, if implemented, generate winners and losers. Overall, the Government expenditure savings from the measure are expected to be $2.4 billion over five years. At this stage, the 2015 approach appears to have been more favourably received than the 2014 approach.

The black hole gobbles the Mersinis

Let’s explore a case study of two retiree couples, extremely simplified for the purposes of demonstrating the black hole effect. Mr and Mrs Hawking are age 66 and 68, own their own home and are not liable to pay income tax. They have $20,000 worth of home contents, a $20,000 car and a $360,000 investment. Mr and Mr Mersini are in the same position except that they have $760,000 invested, so their investment is worth $400,000 more.

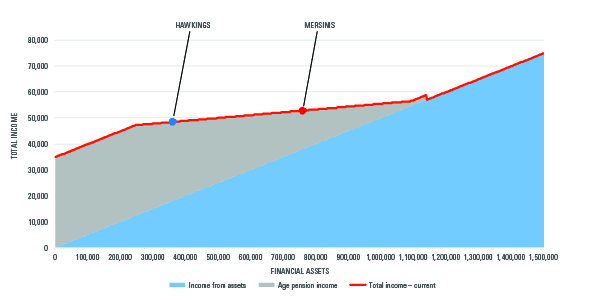

As the graph, left (click to enlarge), shows, if the investments of both couples earn 5 per cent per annum (pa) then, under current rules, the Hawkings will get $30,500 age pension bringing their total income to $48,500. The Mersinis will get a $14,900 pension and their total income would be $52,900. So long as the investments return more than 3.9 per cent pa (the current taper rate), the Mersinis will have more total income than the Hawkings.

As the graph, left (click to enlarge), shows, if the investments of both couples earn 5 per cent per annum (pa) then, under current rules, the Hawkings will get $30,500 age pension bringing their total income to $48,500. The Mersinis will get a $14,900 pension and their total income would be $52,900. So long as the investments return more than 3.9 per cent pa (the current taper rate), the Mersinis will have more total income than the Hawkings.

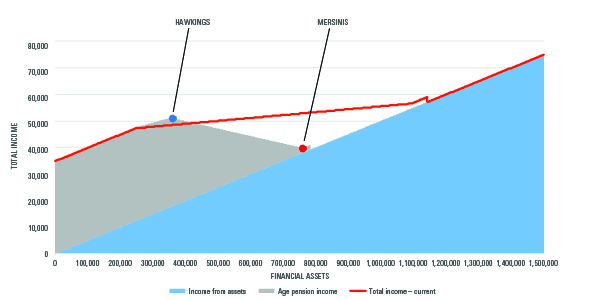

As the graph, left (click to enlarge), shows, if the 2015 Budget proposals are implemented, the Hawkings’ total income will be $51,000, slightly improved as the increase in the asset test free area would effectively increase their age pension. The Mersinis’ total income would be $39,900. While the Mersinis’ extra $400,000 investment is earning a respectable 5 per cent pa, they are losing the age pension at the rate of 7.8 per cent pa for every extra dollar they have invested. So, for every extra $100,000 invested, they are losing $2,800 in overall income.

As the graph, left (click to enlarge), shows, if the 2015 Budget proposals are implemented, the Hawkings’ total income will be $51,000, slightly improved as the increase in the asset test free area would effectively increase their age pension. The Mersinis’ total income would be $39,900. While the Mersinis’ extra $400,000 investment is earning a respectable 5 per cent pa, they are losing the age pension at the rate of 7.8 per cent pa for every extra dollar they have invested. So, for every extra $100,000 invested, they are losing $2,800 in overall income.

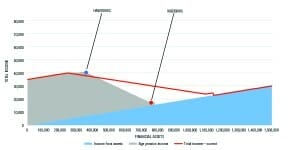

Under the proposed rules, the investments would need to earn more than 7.8 per cent pa for the Mersinis to have more total income than the Hawkings. But what if both couples’ investments are conservative and earn only 2 per cent pa – around the current cash rate? As the graph, left (click to enlarge), shows, the Mersinis’ total income would drop to $17,100, less than half of the Hawkings’ total income of $40,200.

Under the proposed rules, the investments would need to earn more than 7.8 per cent pa for the Mersinis to have more total income than the Hawkings. But what if both couples’ investments are conservative and earn only 2 per cent pa – around the current cash rate? As the graph, left (click to enlarge), shows, the Mersinis’ total income would drop to $17,100, less than half of the Hawkings’ total income of $40,200.

The Mersinis’ kitchen becomes the Tardis

In the face of the asset test proposals the Mersinis need to review their strategy and explore options as to how their investment capital could be applied. One option may be to use some of it to renovate their kitchen. Any resulting improvement in the value of their home would not be counted under the assets test so they would improve their age pension entitlement. Another option may be to gift capital to their children or others, bearing in mind that there are limits on the extent to which gifting capital actually reduces the amount counted under the assets test and the capital would – at least technically – not be theirs to control any more. Of course, they could resort to eroding their capital by living the ‘high life’, but let’s assume that, as typical Australian retirees, they will reject that as an imprudent course of action.The Mersinis’ kitchen becomes the Tardis

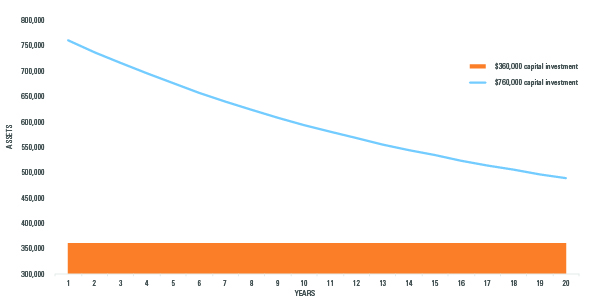

Another approach is for the Mersinis to draw from their investment capital to supplement any shortfall in income arising if the proposals are legislated, assuming the investment is flexible enough to allow this. The graph, left (click to enlarge), shows the impact of the Mersinis drawing capital to top-up cash flow to match the Hawkings’ total income in a 2 per cent pa earning environment, assuming that the Hawkings don’t deplete their $360,000 investment capital, using only investment income and age pension for lifestyle spending. After 10 years their investment capital has depleted to $567,379 and after 20 years it stands at $474,097.

Another approach is for the Mersinis to draw from their investment capital to supplement any shortfall in income arising if the proposals are legislated, assuming the investment is flexible enough to allow this. The graph, left (click to enlarge), shows the impact of the Mersinis drawing capital to top-up cash flow to match the Hawkings’ total income in a 2 per cent pa earning environment, assuming that the Hawkings don’t deplete their $360,000 investment capital, using only investment income and age pension for lifestyle spending. After 10 years their investment capital has depleted to $567,379 and after 20 years it stands at $474,097.

The retirement income policy universe: back to the future?

The conventional wisdom is that retirees manage their investments prudently and conserve capital responsibly. Clients affected by the return to the 7.8 per cent assets test taper rate will face quite a predicament in that regard.

Of course, the proposals don’t completely revisit the pre-2007 settings. Perhaps if the Government were to go a step further and re-introduce an assets test exemption for various types of income stream products, those products would be highly appealing to clients dealing with the black hole dilemma. Query whether this would be an efficient outcome from the Government’s perspective, however.

Taking a broader perspective, the sustainability and fairness of our retirement incomes policy is a product of, among other things, age pension and superannuation tax and benefit rules. While the age pension eligibility proposals have been adjusted from one Budget to the next, the super rules are the subject of structured consultation processes, including the Tax White Paper process. Integration of these components is essential to achieve optimal policy outcomes, but the process for integration is not clear at this stage.

This article is based on laws and regulator policy current at the time of publication.

Leave a Comment

You must be logged in to post a comment.