While the quantitative easing (QE) measures recently announced are better than hoped for, more needs to be done to address the eurozone’s structural problems. What action has the European Central Bank (ECB) taken?

On 22 January, the ECB announced a massive program of QE. They’ve decided to purchase €60 billion of financial assets – mostly eurozone government bonds ─ each month for at least the next 18 months, expanding the ECB’s balance sheet and injecting liquidity of more than €1.1 trillion into financial markets.

The ECB indicated that they were prepared to extend the QE program if inflation remains unacceptably low. The size and composition of the package, and the commitment to an extension if necessary, are better than financial market participants had hoped for. How does it compare with other countries’ QE efforts?

Given the pressure from financial markets for action, the history of eurozone policymakers doing too little too late, and the scope for disappointment, the package is impressive. QE aims to stimulate economic growth by getting more money circulating in a country’s financial system. QE involves the central bank buying financial assets on the open market and paying for them by increasing the liability side of its balance sheet, or ‘money base’.

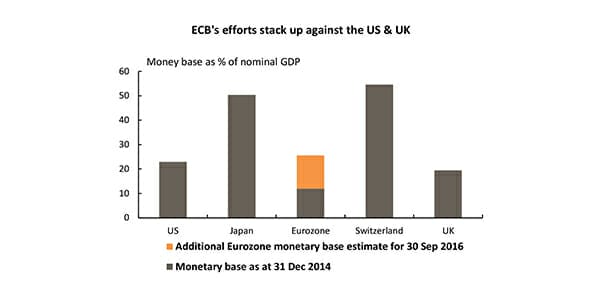

The accompanying chart (source: Datastream and MLC) compares the magnitude of the ECB’s proposed QE efforts against other countries’ programs. It shows the current size of the money base for several countries that have engaged in QE compared to the countries’ GDP, and our estimate of the likely increase in that ratio for the eurozone from the new measures.

The chart suggests that while the eurozone is not planning to be anywhere near as aggressive as the Bank of Japan or the Swiss National Bank, they will end up doing somewhat more to increase the relative size of the money base than either the US Federal Reserve or the Bank of England. Given the magnitude of the eurozone’s problems, they certainly need to.

Will the new QE program succeed? It depends on how we define success. Will it help weaken the euro and strengthen European financial markets? On balance, we think the answer is yes. Will it help boost economic growth in the eurozone? It probably will, but there are good reasons why the impact on growth might be more limited than many hope.

Massive bond purchases should, in theory, drive yields on government bonds lower and help bring down borrowing costs for households and business.

However, bond yields across the eurozone are already extraordinarily low, and borrowing costs for households and business are by no means excessive.

Further, the effects of QE may not be as powerful in the eurozone as in the US. Consumers in the US invest a substantial proportion of their wealth (around 20%) in share markets. US QE has boosted markets, which in turn has boosted US household wealth, allowing Americans to save less and spend more.

That potential transmission mechanism may be less powerful in the eurozone, where listed shares only account for around 4% of household financial assets. Is the ECB’s action the solution to Europe’s underlying structural problems? Sadly, no. The reality is too many countries in the eurozone are carrying too much euro-denominated debt, a currency they don’t control.

Austerity measures designed to bring down budget deficits and stabilise debt levels have largely failed. Austerity leads to weaker growth and even higher unemployment and weaker revenues, further undermining government finances. The recent parliamentary elections in Greece showed that voters there understand this better than most officials and politicians in Brussels or Frankfurt.

Professional Planner blog for February 2015 Conclusion The eurozone desperately needs growth. To restore growth, genuine structural reform and a true economic union are essential. This means the ECB alone can’t provide the solution. While the ECB’s efforts will help, only fiscal policy – spending money– can have a more powerful and immediate impact on growth.

However, there is little evidence that eurozone policymakers – especially the Germans – are willing to allow this, preferring to fret over deficits and debt at a time when nearly a quarter of the continent’s young people are unemployed.

Leave a Comment

You must be logged in to post a comment.