Bronwen Moncrieff examines why global emerging markets have underperformed relative to developed markets.

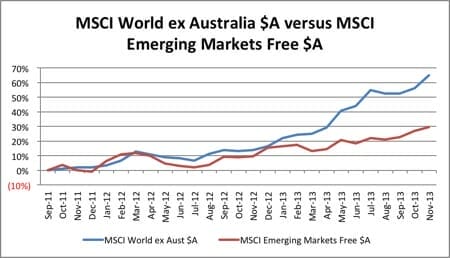

Over the 12-month period to November 30, 2013, investors in global equities (including emerging markets) enjoyed strong absolute returns. The MSCI World ex Australia ($A) Index and the MSCI Emerging Markets Free ($A) Index rose by 45.04 per cent and 18.34 per cent respectively.

Whilst the return from global emerging markets (as represented by the MSCI Emerging Markets ($A) Index) remained healthy at 18.34 per cent, it has materially lagged the return generated by the MSCI World ex Australia ($A) Index, which is predominantly comprised of the returns from developed market stocks.

The divergence in performance between developed and emerging markets from late 2012 onwards is quite apparent in Chart 1.

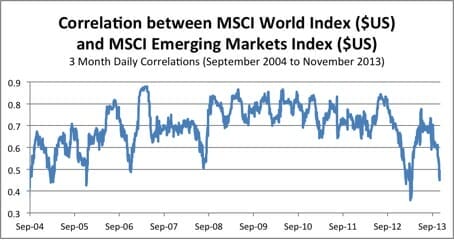

From an emerging markets perspective, correlations between global and emerging equity markets increased during the global financial crisis (GFC) and remained high during the subsequent period of increased global liquidity. However, more recently, as steps towards policy normalisation in the US have progressed – reflected by increases in treasury yields – and as emerging-market-specific developments have taken place, correlations between developed markets and emerging markets have fallen back towards pre-GFC lows. These observations can be seen quite clearly in Chart 2.

As can be seen from Chart 2, correlations between the two indices during the GFC period (September 2008 to September 2011) averaged approximately 0.85. More recently, the correlation between the two indices has fallen towards the 0.4 to 0.5 range.

CHART 1 – Source: Bloomberg

The obvious question is, why have global emerging markets underperformed relative to developed markets?

In general, the emerging markets managers that are part of Zenith’s coverage have cited the following factors as contributors to the underperformance of emerging markets relative to developed markets:

• The managed slowdown of economic growth in China. With the Chinese government targeting a long-term growth rate of 7.5 per cent per annum, and a transition from fixed-asset investment to domestic-based consumption, global markets (developed and emerging) have been affected by the slowdown in Chinese economic growth. However, global emerging markets have experienced a more direct impact relative to developed markets.

• High wage growth. In a number of emerging market economies, the rate of growth in wages has outpaced the level of economic growth. This has resulted in a direct rise in the input costs for companies operating within emerging market economies, reducing their overall level of profitability (assuming no corresponding price increase in their goods/services produced). However, a number of managers have noted that the pace of wage growth is beginning to slow.

CHART 2 – Source: Bloomberg

• High inflation. Similar to high wage growth, high inflation within some emerging market economies has the potential to restrict economic growth and reduce the capacity for government authorities to implement stimulatory policies. The ability of government authorities to reduce interest rates may be moderated in the event of high inflation as lower interest rates may result in further increases in inflation.

But what is the outlook for global emerging markets?

Managers that are part of Zenith’s coverage note that emerging markets, in general, have a number of attractive characteristics from an investment perspective, which remain intact despite recent underperformance. These are noted below:

• The growth rates in emerging markets have generally remained well in excess of those for developed markets. Overall, emerging markets are projected to grow approximately 2.5 times faster than developed markets in 2014, with the IMF forecasting (as at July 2013) average GDP growth of 5.4 per cent for emerging markets, compared to just 2.1 per cent for developed markets.

• Unlike developed markets, many emerging and frontier markets still appear to have ample room to implement fiscal and monetary stimulus should they be required. That is, these economies have the capacity to materially reduce interest rates or implement stimulatory fiscal measures. However, as mentioned in the previous section, where the economy is experiencing heightened levels of inflation, the capacity for such stimulatory measures may be somewhat tempered.

• Although weak growth in developed markets could flow through to emerging markets, notably through declines in world trade, this influence could be offset in emerging markets by higher investment spending and increased domestic demand.

• The debt level of many emerging markets in relation to their GDP is generally significantly lower than that of many developed markets.

• Valuations for emerging market stocks remain attractive. As a result of the depressed prices of emerging market equities arising from the recent capital outflows, the valuations of emerging market equities have become relatively attractive when compared with developed market equities.

How does this impact client portfolios?

While the impact of globalisation would appear to be a key driver for the increased correlations between global and emerging markets, Zenith believes emerging markets generally remain an attractive option within the international equities component of an overall portfolio.

Leave a Comment

You must be logged in to post a comment.