A lot of the debate about property in self-managed super funds has missed a bigger issue: is there a reasonable investment case for it being there in the first place? Dug Higgins explains.

As we look back on 2013, if one thing will stick in my memory it’s the seemingly endless debate around geared property and self-managed super funds (SMSFs). It seems that not a week went by without either dire warnings from regulators on the one hand or heated rebuttals from facilitators on the other. But with neither camp seemingly willing to commit to an armistice, perhaps one key question seems to keep going relatively unasked: If we consider directly-held property as an investment (notwithstanding the regulator’s definition), does it have merit in a long-term investment portfolio?

The ability to hold real estate in an SMSF comes with a host of structural advantages. But just because a client can do it, does it mean that they should? After all, investment decisions should not be obscured by structural advantages.

Much of the current debate is centred on residential property. However, based on information to date (although a lagging indicator), relatively small amounts of residential property appear to have ended up in portfolios, compared to commercial property. So in this instance, I’m going to concentrate on the traditional avenue, which typically utilises the trustee’s own business premises.

For many years now, it has been permissible for an SMSF to invest in commercial property from which a fund member runs a business – but only since 2007 has it been permissible to borrow. How then does geared property benefit an investment portfolio?

Significant advantage

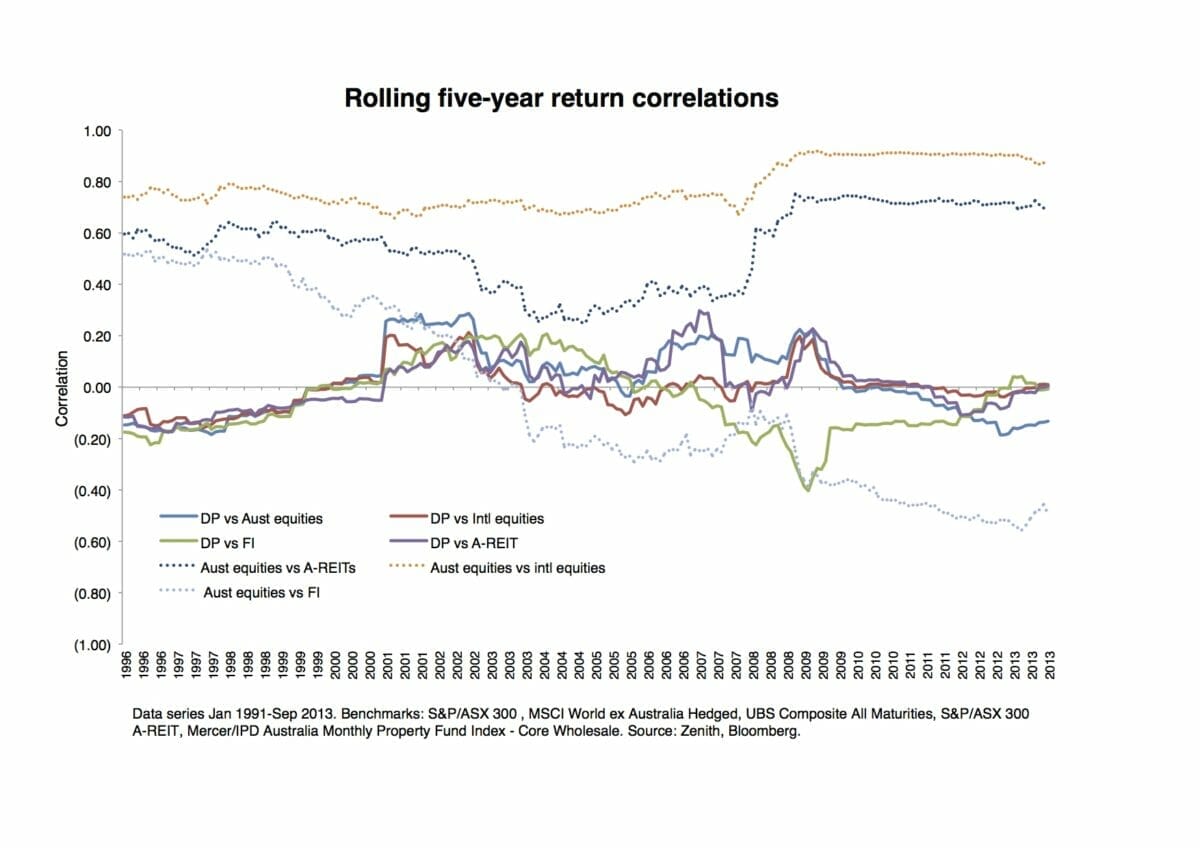

In Zenith’s view, the addition of commercial real estate to the portfolio construction process brings a significant advantage in terms of lowering volatility. During the global financial crisis (GFC), investment portfolios otherwise thought to be relatively diversified saw correlations across many assets converge. While correlation analysis is an important part of the portfolio construction process, it can obviously be misleading to take spot figures or averages into account. So here we focus on the longer-term rolling data.

Direct property as an asset class presents a significantly low correlation to domestic and global equities – two of the traditional building blocks of investment portfolios. Chart 1 illustrates the historical rolling correlation of direct property (DP) against the other major asset classes, using broad industry benchmarks. We have included paired correlations of some of the other major assets, such as domestic versus global equities (shown by dotted lines), as a comparison.

What is apparent is that over the longer term, direct property has generally retained its low correlation and remained resistant to incidences of correlation convergence during times of turmoil. While obviously the timing of the correlation analysis is important, we assume superannuation is long-term and so have used five-year rolling periods in our analysis. When examined over a shorter timeframe, such as three years, the correlations are only slightly higher and do not meaningfully detract from the diversification picture.

The predominant driver of property’s low correlation is the comparatively low liquidity and tradability of direct real estate, coupled with a slower valuation cycle than more liquid securities. While direct property is often accused of having “false” indicators around its low volatility, it is important to realise that regardless of whether this accusation is true or false, it is also market reality. It can just as easily be recognised that liquid asset classes suffer from trading sentiment, which results in increased market volatility. Ultimately, the cash flows generated by an asset do not alter depending on the nature of the investment vehicle in which it is held. But the level of tradability of that vehicle is crucial in driving volatility.

Risk and return

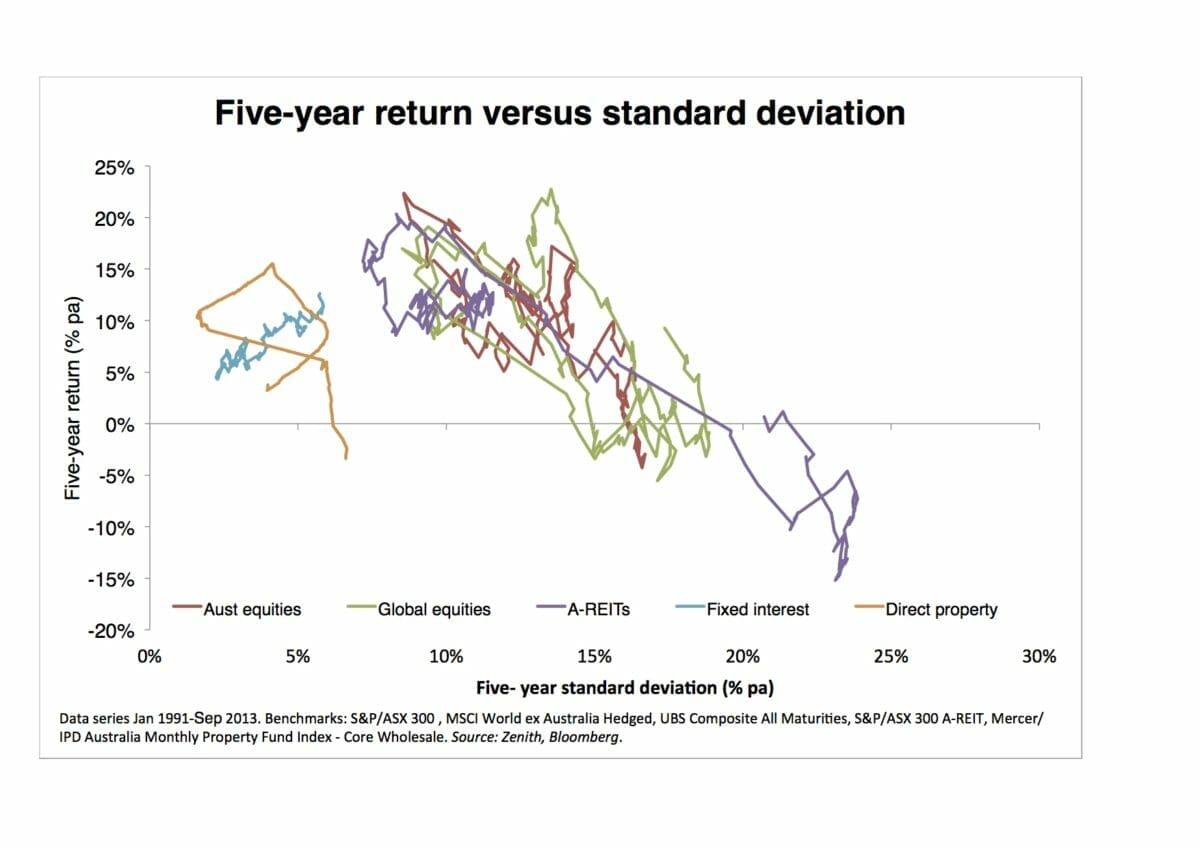

Correlation should not be considered in isolation, so it is also appropriate to consider the risk/return proposition. Chart 2 details the moving five-year return versus standard deviation of each major asset class over the same period.

The use of a “snail trail” chart is useful as it encapsulates the movement of returns and volatility over time. Predictably, the liquid asset classes have been more volatile while the less liquid direct property category shows stronger levels of stability. Total returns over the data series have been solid given the strong income-generating capacity of the underlying assets to stabilise overall outcomes.

Downsides

So, if these outcomes show that direct property has obvious benefits in a portfolio, what are the downsides? Firstly, it should be recognised that most SMSFs will only hold a single asset. This means the level of risk in the portfolio would be significantly higher than otherwise indicated by the data, which takes into account hundreds of properties. Also, given the comparatively large value of most commercial properties, care must be taken that overall portfolio diversification if not excessively skewed to a single asset.

Gearing should also be taken into account, as this obviously magnifies positive and negative outcomes. Zenith would suggest that from a property strategy perspective, gearing at levels in excess of 50 per cent should be approached with caution. The direct property returns shown here are geared, but to a relatively low level.

Trustees should also give significant consideration to whether or not a property will be divested before or after pension phase. If they wait until entering the pension phase, the sale of the asset will be capital-gains-tax-free and the income stream may prove attractive. However, the risks may be considerable if the property – most likely a single asset – falls vacant.

Ultimately, Zenith believes that from an asset allocation perspective, direct commercial real estate has solid merit inside (and outside) super. However, careful consideration must be given to the strategy employed; and it is imperative to ensure trustees are not blinded by structural considerations.

Leave a Comment

You must be logged in to post a comment.