Stockspot, a leading automated investment adviser, has today released its annual Fat Cat Funds report. It is Australia’s largest and most comprehensive analysis of 3,820 super and managed funds which names the best and worst performers.

This year the report found 638 Fat Cat Funds and 574 Fit Cat Funds. A fund is a Fit Cat when it performs better than its peers over 1, 3 and 5 years and by more than 10% over the 5 years. While to be named a Fat Cat a fund must perform poorly compared to peers over 1, 3 and 5 years and by more than 10% over the 5 years.

The research found that $59 billion is trapped in Fat Cat Funds that consistently underperform and $777 million per year is paid to these Fat Cat Funds in fees.

The research shows Fit Cat Funds charge on average 0.94% in fees whereas Fat Cats Funds charge an average of 2.04%. A consumer in a Fit Cat Fund pays 12% of their returns in fees as opposed to 28% of returns which are paid in fees to Fat Cat Funds.

The top Fit Cat Funds are: Investor’s Mutual, SG Hiscock & Company, REST Industry Super, Vanguard Investors, Lazard Asset Management & Legg Mason Global Asset Management.

Table 1. Top three Fit Cat Award winners

| Fit Cat Fund | % of Fit Cat Funds |

| Investor’s Mutual | 75% |

| SG Hiscock and Company | 70% |

| REST Industry Super | 43% |

Commenting on the research, Chris Brycki, Stockspot CEO & founder said:

“It’s disappointing there are still so many Fat Cat Funds, however we should not forget to celebrate the Fit Cat Funds. The Fit Cat Funds have done well for their customers by consistently delivering higher returns. They set an example of best practice that the rest of the industry should attempt to follow.

“We’ve set a high bar for both poor and high performance. To be classified a Fat Cat the fund has to be seriously underperforming. Almost three quarters (74%) of the Fat Cat Funds charge over 1.5% in fees. On the other hand 78% of Fit Cat Funds charge much lower fees ranging between 0.2% – 1.5%. The research shows a clear relationship between high fees and poor investment returns.

Industry v retail super funds

Stockspot’s Fat Cat Funds report also shows Industry Super funds continue to outshine their retail rivals. Of the Retail Super funds, 39% were a Fat or a Flabby Cat, as a opposed to Industry Super funds with only 13% being deemed as a Fat or Flabby Cat Fund. 72% of Industry Super funds achieved a Fine Cat Fund or Fit Cat Fund status.

“It’s not a matter of Industry funds being superior, most Retail super funds actually do better pre-fees, however after fees they deliver a significantly poorer result. What is the point of good returns when they’re eroded by high fees?” questioned Brycki.

Government intervention required

Stockspot believes government should intervene with two measures to improve fairness for consumers. It wants government to:

• require all superannuation and managed fund products to provide fee and performance data to a comparison website.

• implement a public tender for the right to manage default super funds.

“Superannuation is the single most important savings pot we will have in our life, so surely this is an issue that needs Government intervention.

“A public tender for the right to manage default super funds has the potential to halve fees. Chile’s established public tenders for the right to manage default super funds has reduced average annual super fees to 0.30% versus average fees of well over 1.0% in Australia”.

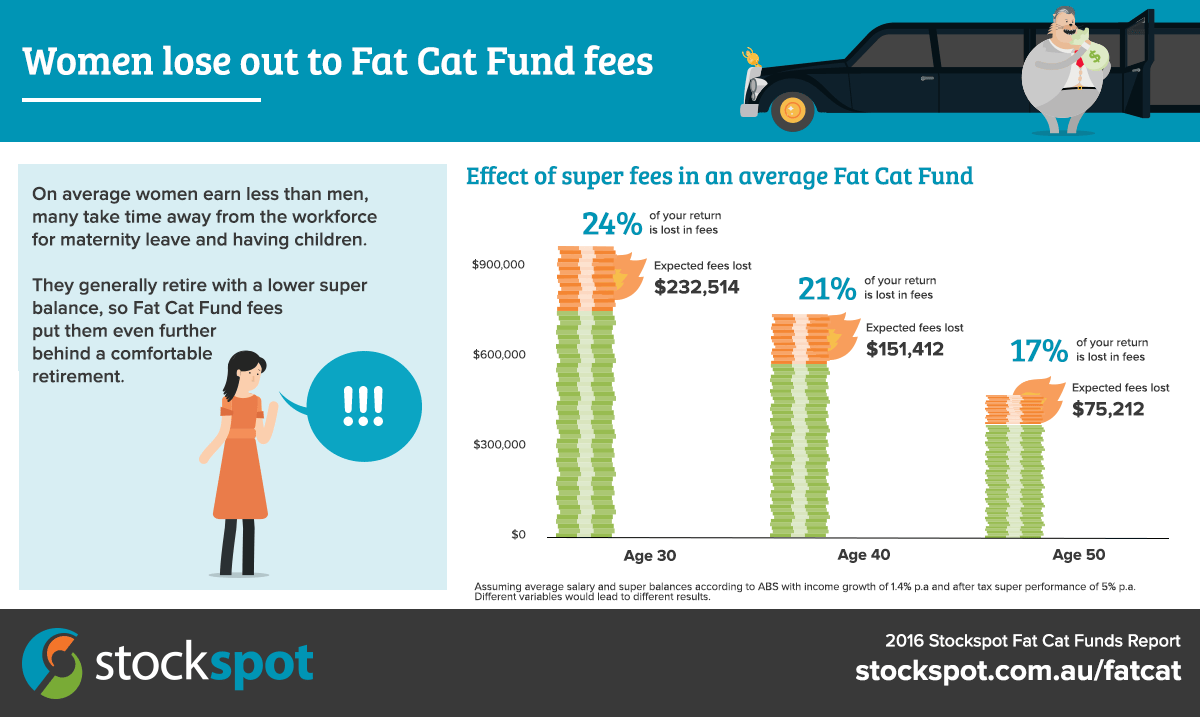

Adult Australians of all ages impacted

An important report finding is the impact a fund’s compounding fees has on savings.

The 30 year olds of today could lose nearly a quarter (24%) of their lifetime super savings in fees if their money is trapped in an average Fat Cat Fund. Men could lose $285,208 and women could lose $232,514. Furthermore, people in their fifties could lose over $100,000 in the years leading up to retirement.

Table 2: Demonstrates superannuation balances before and after the effect of Fat Cat Fund fees.

| Age | Women super balance – pre fee | Women – balance after fee | Men super balance – pre fee | Men super balance post fee | % loss |

| 30 | $980,111 | $747,597 | $1,197,840 | $912,632 | 24% |

| 40 | $729,366 | $577,954 | $900,931 | $709,498 | 21% |

| 50 | $433,560 | $358,348 | $628,538 | $515,093 | 18% |

Brycki continued:

“Regardless of your age if you’re in a Fat Cat Fund high fees could be a total disaster for your ability to pay for a comfortable retirement. The problem is compounding fees. 2% in fees doesn’t sound like a huge sum, but the compound effect over 30 or 40 can mean a quarter of a million dollars”.