Bond markets reacted quickly in May and June when the US Federal Reserve (the Fed) indicated it would begin winding back its bond-buying economic stimulus program earlier than expected.

Bond prices plunged and yields in all the major bond markets rose sharply (the two move in opposite directions). Investors interpreted the Fed’s hints as a sign that interest rates would start moving upwards, driving down bond prices.

Bond markets have continued to be volatile over the last three months. On balance, the magnitude of the recent sell-off looks overdone: global growth and inflation remain below trend and don’t support rapid interest rate increases. The Fed’s recent announcement that it would not yet wind back the bond purchase program supports this view.

Investors holding bonds lose money when bond prices fall (due to interest rates and yields going up). They make money when prices rise (due to yields falling). The recent fall in prices, and rise in yields, has meant short-term negative returns from bonds. As investors tend to see bonds as the stable, reliable part of their portfolio, some have begun to question whether they remain a worthwhile investment.

Despite short-term market gyrations, bonds play a very important role in a diversified portfolio. Understanding this can help investors take a more long-term view and reassure them that bonds remain a valuable investment.

What role do bonds play in a diversified portfolio?

Diversification

Bonds aren’t generally included in an investment portfolio for the purpose of generating high returns (though they have in fact done this over the last 30 years). Rather, the role of bonds is to increase diversification, as bonds tend to perform well when shares are doing badly and vice versa. So bonds help insulate against the worst kind of market risk − the risk that share markets plunge suddenly and unexpectedly.

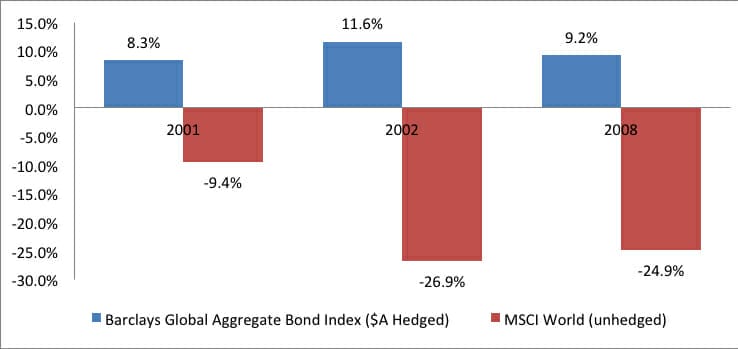

For example, in 2008, global share markets seemed to be sailing toward another year of gains, while bond prices were experiencing 30-year lows. Why own bonds in an environment like that? Well, because by the end of calendar year 2008, a mixed portfolio of bonds had achieved a 9 per cent positive return, while stocks were losing 25 per cent − meaning bonds outperformed stocks by 34 percentage points. A similar drop in share prices and surge in bond returns happened in 2001 and 2002 (see chart, below).

The stabilising effect of bonds means that over time, investors holding bonds and shares enjoy a smoother ride and experience lower losses in share market downturns than those just holding shares.

Although returns on some types of bonds are currently low, especially compared with the strong returns of recent decades, bonds are still likely to help cushion a diversified portfolio against the volatility of share market returns. This alone makes bonds worth holding.

Income

Another important reason to invest in bonds is the regular income they provide. The interest payments an investor receives on a bond, called coupons, are a fixed amount, rather than being paid at a company’s discretion like dividends on shares.

In recent years, low interest rates and yields have made it necessary to look beyond government and even corporate bonds to other bond markets to find higher yields.

These markets include US high yield bonds (corporate bonds with a lower credit rating and therefore higher risk) and bank loans (debt of companies rated “high yield”). Both held up quite well during the recent bond market sell-off.

What’s the outlook for interest rates?

We think markets have overreacted to the Fed’s recent comments about winding back the bond purchase program. While the US economic recovery is gaining momentum, it doesn’t appear strong enough to accommodate higher borrowing costs, so it’s unlikely interest rates there will rise sharply. A gradual rise is more probable.

And all Fed governors have emphasised that interest rates will remain low beyond any changes to quantitative easing. Both UK and eurozone economies remain weak and we expect rates to remain low there too.

Meanwhile, economic indicators in Australia remain soft because of concerns about the sustainability of commodity demand from China, a rise in unemployment and the change in the Federal government. To top it all, Japan has recently begun its own bond purchase program, which may end up being even larger than the Fed’s. All of this points towards interest rates, and bond yields, remaining low for a while.

Kajanga Kulatunga is a portfolio specialist with MLC Investment Management