Produced in partnership with Allianz Retire+.

In the complex world of retirement planning, it is often challenging to align clients’ portfolios with income needs that are as varied as they are critical. Understanding the hierarchy of retirement spending and the strategic structuring of income sources can make the difference between a comfortable retirement and a financially strained one.

There are generally a limited range of actions that retirees can consider when projected income falls short, but with new, flexible solutions coming to market, lifetime income streams can be an effective part of the solution.

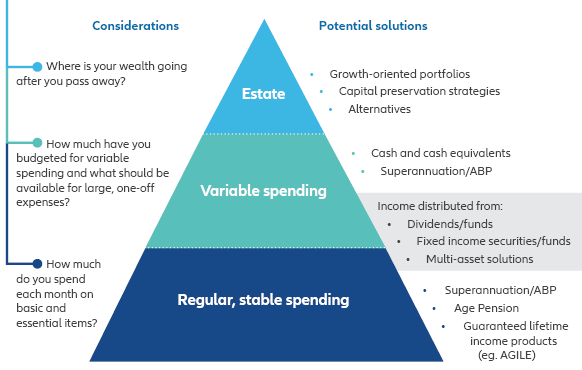

The hierarchy of retirement spending

Retirement spending typically falls into a hierarchy, beginning with:

- Essential expenses such as housing, food, and healthcare,

- Discretionary spending including travel and leisure activities; and

- Estate planning and legacy goals completing the hierarchy.

This hierarchy underscores the importance of matching dependable income sources, such as guaranteed lifetime income streams, with regular, predictable expenses.

More variable expenses might be met with other more variable income and/or growth-oriented solutions and a cash reserve, providing flexibility and potentially funding one-off retirement expenses or legacy goals.

Chart 1: Hierarchy of investment spending

Dependable income sources are particularly suited to covering essential expenses. These are the non-negotiable costs that require a stable, salary-like income stream that remains unaffected by market fluctuations, offering retirees the security they need to manage regular expenses.

Structuring a portfolio to align with income needs

When structuring a portfolio for retirement, diversification is key.

In a September 2024 research paper titled An update on superannuation account balances, the Association of Superannuation Funds of Australia highlighted the gap between median superannuation balances, being $397,566 for a couple combined, and the $690,000 savings the December 2024 ASFA Retirement Standard says is required for a “comfortable retirement”.

This gap emphasises the need for retirees to diversify their income sources beyond the traditional term deposits, shares/dividends, interest, rent, and so on. Growth-oriented portfolios can provide the potential for increased returns, but they come with inherent risks.

Options when income falls short

Retirees facing projected income shortfalls have limited strategies at their disposal:

- Taking on greater risk: by shifting to growth-oriented investments, retirees can potentially increase their returns. However, this approach requires careful consideration of risk tolerance and market conditions, noting client capacity for loss changes in retirement. It also requires careful portfolio management to mitigate sequencing risk – does the adviser or the client want to retain all of that that risk?

- Delaying retirement: postponing retirement can allow for additional savings accumulation and potentially higher or longer retirement income – but this option may not be attractive or even available to many retirees.

- Cutting back spending: adjusting retirement lifestyle expectations and reducing discretionary spending can help manage limited resources however this is often the least favoured option by clients and where tailored advice is crucial.

- Incorporating guaranteed lifetime income streams: solutions that offer a dependable income source can bridge the gap between funding essential expenses for the long term and available funds. A design incorporating a guaranteed future lifetime income rate and investment options with downside protection manages longevity and sequencing risk, helping to ensure financial security and client confidence throughout retirement.

The role of guaranteed lifetime income streams

Lifetime income streams operate as a form of insurance for longevity, protecting against the financial risks of outliving savings. By allocating a portion of a client’s portfolio to the right retirement income product, advisers can provide clients with peace of mind, knowing their budgeted essential expenses will be covered regardless of market conditions.

For those seeking stability, or even permission to spend, guaranteed lifetime income products offer a compelling solution, offering downside protection to ensure that lifetime income payments do not decrease even when markets fluctuate, with options for income to rise over time to support the increasing cost of living.

When determining the allocation for lifetime income streams, it makes sense to start with the client’s monthly retirement budget, assessing how much income is needed for daily living expenses and identifying portions of spending that may fluctuate. This tailored approach ensures that clients can maintain their desired lifestyle without financial stress.

Achieving a reliable income, that is not correlated to income being generated from other assets in the portfolio, is key to providing security and confidence in retirement. For variable spending needs, there may be room to move the timing of income drawdowns, but when markets dip and/or fixed interest returns drop, the retirement income that covers essential or fixed cost spending shouldn’t also drop – if income sources have been correctly matched with a client’s spending hierarchy.

It’s worth noting too, the flexibility of some retirement income products also allow for partial or full withdrawals if there is an otherwise unplanned and unfunded expense or a change in circumstances, and often their inclusion in a portfolio even improves legacy outcomes. Of course, they can be utilised to improved age pension outcomes too – but that is not the limit nor the end goal for retirement planning.

As retirement strategies evolve, so too must our approach to income planning. Not all income is created equal. By combining a clear understanding of spending priorities with a diversified mix of income sources—including guaranteed lifetime income—advisers can help clients retire with greater certainty, clarity and peace of mind.

Justine Marquet is head of technical services at Allianz Retire+.