Produced in partnership with iShares by BlackRock.

Geopolitical tensions and concerns over stretched AI valuations have contributed to a summer of lacklustre performance for global equities, which generated a return of -3.4 per cent in the three months to January 2026, according to the MSCI World ex Australia Index as of 31 January 2026.

At the same time the MSCI World ex Australia Minimum Volatility Index – a portfolio of developed market stocks with a low volatility ‘tilt’ – returned essentially flat (-0.19 per cent as of 31 January 2026), demonstrating the advantage of leaning into this type of strategy at times of market nerves.

As sentiment turns away from growth-oriented US tech stocks – around 42 per cent of respondents to a recent BlackRock client survey are looking to reduce US equity exposure in the next three months – investors are becoming increasingly interested in ways to steady their portfolio in the event of a sell-off.

In fact, these portfolio diversifiers are increasingly hard to find, with bonds not providing the reliable protection against share market sell-offs that they once did. BlackRock believes investors need a new approach to diversification, layering different strategies to build resilience when shocks occur.

With their grounding in decades of economic theory, and broad exposure across a range of markets and sectors, minimum volatility investing strategies may be a handy piece of the diversification toolkit in months to come.

Why minimum volatility investing?

To understand the potential benefit of investing in lower-volatility stocks over time, it’s helpful to use the analogy of a hiker who has two potential paths to climb a mountain – one is rocky with several sharp descents, and one is more gradual and stable.

A minimum volatility strategy would look more like the second trail — not as exciting, but designed to help investors navigate the risks of big fluctuations in the market with less anxiety.

Minimum volatility investing is backed by decades of economic data showing that less volatile stocks have outperformed more volatile ones over time.

There are a few theories as to why – for example, institutional investors may be overweight to more volatile companies to capture more equity premium and reach their return targets.

In practice, a global equity portfolio constructed with a tilt towards low volatility stocks – that is, stocks with both lower volatility versus the market, and lower volatility versus the other stocks in the portfolio – can even out the swings of equity markets for investors while still capturing much of the upside.

To illustrate this point, if we look at the performance of the MSCI World Minimum Volatility Index since its inception on 31 May 1988, we can see it has exhibited 20 per cent less volatility than broad global equities (via the MSCI World Index), while also generating broadly the same 9 per cent average annualised return, as of 31 January 2026.

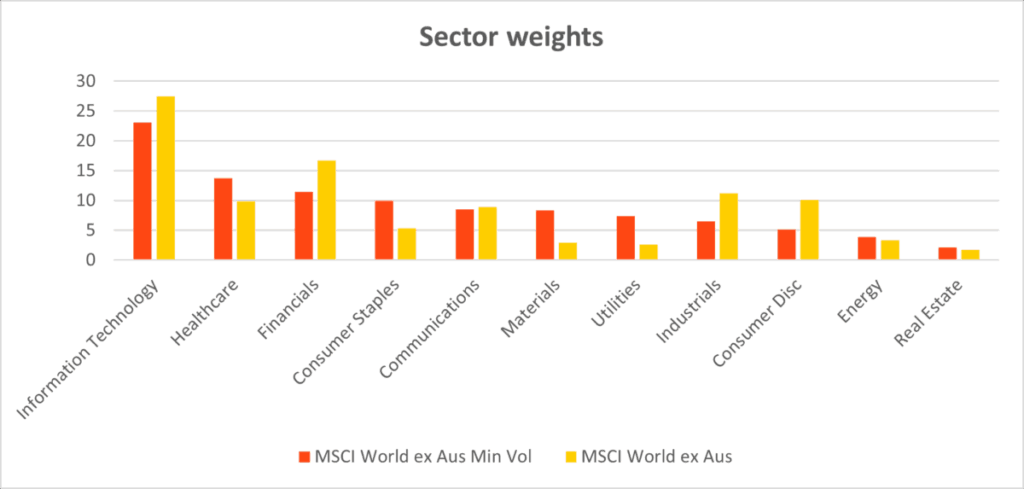

A key feature of the Minimum Volatility Index is that it’s constructed to have broadly similar sector weights to a traditional global equity passive exposure. As seen in the chart below, this prevents overweights into traditional safe haven sectors, allowing the index to achieve similar returns to broad global equities over time while smoothing out volatility.

Source: MSCI data as of 31 December 2025. Indexes are unmanaged and one cannot invest directly in an index.

Of course, a lower volatility approach does have its downside – namely short-term underperformance during economic expansion periods.

For instance, if we look at the past three-year period that’s been characterized by exceedingly strong returns in equity markets, the MSCI World ex Australia Minimum Volatility Index has trailed the broader MSCI World ex Australia Index by 8 per cent, as of 31 January 2026 and based on average annual returns from 31 January 2023 to 31 January 2026.

However, with concerns in today’s market environment ranging from growth to earnings breadth to valuations, we believe pockets of the volatility we’ve seen so far this year are likely to persist, making it worthwhile for investors to consider leaning into a minimum volatility approach.

What’s more, valuations for minimum volatility stocks are looking attractive versus their historic average, and versus the broader market, based on historical data from the period 31 July 1994 to 30 November 2025.

Examples of some of the names you may find in the MSCI World ex Australia Minimum Volatility Index include Johnson & Johnson, ExxonMobil and Berkshire Hathaway. Investors can gain access to the index through the iShares MSCI World ex Australia Minimum Volatility ETF (WVOL).

Batten down the hatches

Market conditions look increasingly volatile as we close out the first quarter of the year – as seen in the latest Australian reporting season, where over a third of companies saw extreme price swings after reporting, which is significantly above average, according to JP Morgan data.

As such, turning to a strategy with more resilient historical performance during market downturns may make sense.

This is another potential advantage of the minimum volatility portfolio – in each of the largest four corrections in the stock market from 2006 to 2026, WVOL has outperformed the broad global equity benchmark, according to MSCI data.

Offering both sector diversification and a focus on lower individual stock volatility over time, minimum volatility investing may be a compelling option for investors looking to stay in equity markets, but ride out any potential storms with less downside than a classic index approach.

To explore how different strategies can work together to build more resilient portfolios, visit BlackRock’s Diversification Toolkit, which brings together product solutions to help navigate uncertain markets.

Tamara Haban-Beer Stats is the lead ETF and index investments specialist in Australasia for BlackRock.